Your jobs wrapped on time, your crews got paid, or your practice stayed booked solid. Then tax season hits, and you find out you may have left a large deduction sitting on the table.

That is how the 20 qbi deduction shows up for a lot of owners in Jacksonville and Northeast Florida.

If you are a Jacksonville contractor running more than one LLC across active job sites, or a healthcare practice owner in Ponte Vedra deciding how to split profit between owner pay and business income, this deduction is not a technical side issue. It affects how much cash you keep after a strong year. It also affects how much trouble you invite if your books, payroll, and entity setup do not match the tax position you claim.

Here is the plain-English version. If your business income passes through to your personal return, the Qualified Business Income deduction may let you deduct up to 20% of that income, subject to rules tied to your taxable income, your business type, W-2 wages, and certain business property. It was created by the 2017 Tax Cuts and Jobs Act and later made permanent, as explained in Thomson Reuters' QBI overview.

This rule saves real money. It also creates real risk.

Construction owners run into problems when job-costing is sloppy, owner draws are confused with payroll, or multiple entities are set up without a clear tax strategy. Healthcare owners hit a different wall. Compensation structure, partner allocations, and whether the practice falls into a service category can change the result fast. Get it right and you lower your tax bill. Get it wrong and you hand the IRS an easy place to start asking questions.

That is why serious owners do not treat QBI like a box to check in March. They treat it like year-round planning with a CPA who knows how Florida contractors and medical practices operate.

Your Biggest Tax Break Might Be Hiding in Plain Sight

A Jacksonville contractor wraps up a profitable year, sees solid cash in the bank, and assumes the tax bill is just the price of doing well. A medical practice owner in Ponte Vedra does the same after adding a new provider and growing collections. Then tax season hits, and both learn the same lesson. Profit alone does not decide the final tax bill. Structure does.

The 20 qbi deduction can be one of the biggest tax breaks available to pass-through business owners. If your income flows from the business to your personal return, you may be able to deduct up to 20% of qualified business income. Done right, that can preserve a meaningful amount of cash. Done carelessly, it can shrink fast or disappear.

For Northeast Florida owners, this is a planning issue, not a form-prep issue.

Why Florida business owners should care now

The rules around QBI are too valuable to ignore and too technical to wing. Starting in 2026, the deduction remains in place, the married filing jointly phaseout range expands to $150,000, the upper threshold moves to $544,600, and single filers face a $197,300 to $272,300 phaseout range. There is also a new minimum $400 deduction for taxpayers with QBI over $1,000, adjusted for inflation after that year, as noted earlier.

That matters in real life.

A construction company can swing from a thin-margin quarter to a strong one based on job timing, retainage, equipment purchases, and labor costs. A healthcare practice can look wildly different after provider compensation, partner allocations, and staffing changes hit the books. Those shifts can push you into a range where QBI planning gets more complicated, and where bad bookkeeping turns into expensive tax results.

If you wait until March, you have already limited your options.

Where owners get this wrong

The problem is not the headline. The problem is everything underneath it.

QBI planning depends on several moving parts working together:

| Issue | Why it matters |

|---|---|

| Entity type | Your setup controls how income, compensation, and planning options show up on the return |

| Taxable income | Higher income can trigger limits that change the size of the deduction |

| Business type | Healthcare and other service businesses can run into tighter rules |

| Payroll | W-2 wages can affect how much deduction survives at higher income levels |

| Assets | Certain business property can matter in the limitation calculation |

This is why I push business owners to stop treating QBI like a coupon. It is closer to a construction estimate. If the inputs are wrong, the final number is wrong.

In Jacksonville construction, I see owners mix draws, reimbursements, and payroll like they are interchangeable. They are not. In healthcare, I see practice owners assume all profit qualifies the same way regardless of how doctors are paid or how the entity is structured. That is how money gets left on the table, or worse, how a return ends up claiming a deduction the records cannot support.

A CPA should be involved before year-end, while there is still time to adjust payroll, review entity treatment, clean up bookkeeping, and test different scenarios. That is how you protect the deduction and avoid handing the IRS an easy issue to question.

What Exactly is Qualified Business Income

The first mistake owners make is assuming all income is treated equally. It is not.

Qualified Business Income is the net income from your actual business operations that passes through to your personal return and is eligible for the deduction. If you own a Jacksonville framing company, a specialty contractor, a medical practice, or a local retail business, QBI usually starts with the ordinary profit from doing the work, billing the customer, paying the expenses, and ending up with real operating income.

Which businesses can use it

The deduction applies to income from sole proprietorships, partnerships, S corporations, and certain trusts and estates, according to TurboTax's explanation of the qualified business income deduction.

That puts a large share of Northeast Florida businesses in play. If your income passes through to you instead of being taxed inside a C corporation, QBI belongs on your annual tax planning checklist.

What owners include by mistake

Owners get into trouble when they lump everything together. The tax return may show business profit, investment activity, gains, and other income on the same pages, but QBI does not pull from every line item.

Capital gains, dividends, and similar investment-type items generally do not count the same way as operating profit. The deduction is also capped by taxable income, and that cap is calculated after subtracting net capital gains. That detail matters more than people expect.

A construction owner might sell equipment at a gain and assume that extra income helps the deduction. It may not. A physician with a healthy brokerage account may have strong total income and still see the QBI result limited because investment income does not feed the calculation the way practice income does. Those are the kinds of details that separate a decent return from an expensive mistake.

The practical definition

Use this working definition:

- Included: Ordinary profit from an eligible pass-through business

- Excluded or treated differently: Capital gains, dividends, and other non-operating items

- Still limited: The final deduction cannot exceed the taxable-income-based cap

That is why clean books matter so much. If your bookkeeping mixes shareholder distributions, personal investment activity, owner draws, reimbursements, and true operating profit, your QBI number can go sideways fast. In construction, that often shows up when equipment, job reimbursements, and owner pay are coded inconsistently. In healthcare, it shows up when practice income, ancillary services, and doctor compensation are not separated correctly.

A CPA's job here is simple. Draw a hard line between what counts and what does not, then document it well enough to survive scrutiny. That is how you keep the deduction you deserve and avoid claiming one your records cannot support.

Are You Eligible The Income and Business Type Rules

A Jacksonville contractor and a multi-partner dental practice can both show strong profit on paper and get two very different QBI results. That surprises owners every year. Profit matters, but it does not settle eligibility by itself.

Two filters control this section of the deduction. Your taxable income comes first. Your business type comes second. Get either one wrong and the deduction shrinks or disappears.

Gate one is income

Once taxable income moves above the IRS threshold, the calculation gets tighter. For 2025, the threshold is $197,300 for single filers and $394,600 for joint filers, and the wage and property limitation can reduce the deduction above those levels, as explained in the IRS newsroom guidance on the qualified business income deduction.

Below the threshold, many owners can claim the deduction with fewer moving parts. Above it, the return has to be built, not guessed at. W-2 wages matter. Qualified property matters. The way you run payroll matters.

That hits construction businesses in a very practical way. A contractor in Northeast Florida who owns equipment and pays a real field and office staff often has more room to preserve the deduction because wages and depreciable property can support it. But that only works if job costs, payroll, and asset records are clean. If materials, subcontractors, and equipment purchases are sloppily coded, you create your own tax problem. That is one reason accurate inventory and job-cost treatment matters, especially if you need to sort direct costs correctly for tax reporting and calculate cost of goods sold properly.

For 2026, as noted earlier, the threshold structure changes for some filers. Owners should review QBI every year, not once and assume the answer stays the same.

Gate two is business type

Business type can change the answer fast. The big dividing line is whether your company is a Specified Service Trade or Business, or SSTB.

Construction companies usually have the better setup here because they are generally not SSTBs. Many healthcare practices are. That means a successful construction firm and a successful medical or dental practice can sit at the same profit level and still land in very different places on the deduction.

Here is what "tougher analysis" means in real life for healthcare. Take a multi-partner dental practice in Jacksonville. The practice may throw off healthy profit, but we still have to review each partner's total taxable income, not just the practice's bottom line, to see whether that partner's deduction is limited or phased out. One partner may qualify for a meaningful deduction. Another partner in the same practice may lose much of it because of spouse income, investment income, or other pass-through earnings on the return.

That is why healthcare owners get in trouble when they rely on a quick estimate from bookkeeping software. The software sees practice profit. A CPA looks at the full return, the SSTB rules, owner compensation, and whether the deduction survives once all the pieces are on the table.

Here's the straight read for Jacksonville owners:

- Construction companies: Often have stronger QBI planning opportunities because they are usually outside the SSTB category and may have wages and equipment that help support the deduction.

- Healthcare practices: Face stricter limits once owner income rises, especially for physicians, dentists, and other licensed professionals whose work falls squarely inside SSTB rules.

- Professional firms: Accounting, consulting, and similar service businesses need a line-by-line review. Close enough is how deductions get lost.

If you run a service business and your income is climbing, stop comparing your tax result to a builder, roofer, or site contractor. The rules are not playing the same game.

A quick self-check

Use this grid as a first pass:

| Question | Why it matters |

|---|---|

| Are you a pass-through entity? | If not, QBI may not apply the way you expect |

| Is your taxable income below the threshold? | Lower income usually means fewer limitations |

| Are you an SSTB? | Service businesses can face stricter treatment |

| Do you pay W-2 wages? | Above-threshold returns may rely heavily on this |

| Do you own qualified business property? | UBIA can affect the limitation calculation |

A lot of owners answer the first question, see pass-through income, and assume they are set.

They are not.

You need all five answers right, backed by records that hold up if the return is questioned. That is why professional help is not optional here. QBI is one of those deductions that looks simple from across the room and gets expensive the minute you cut corners.

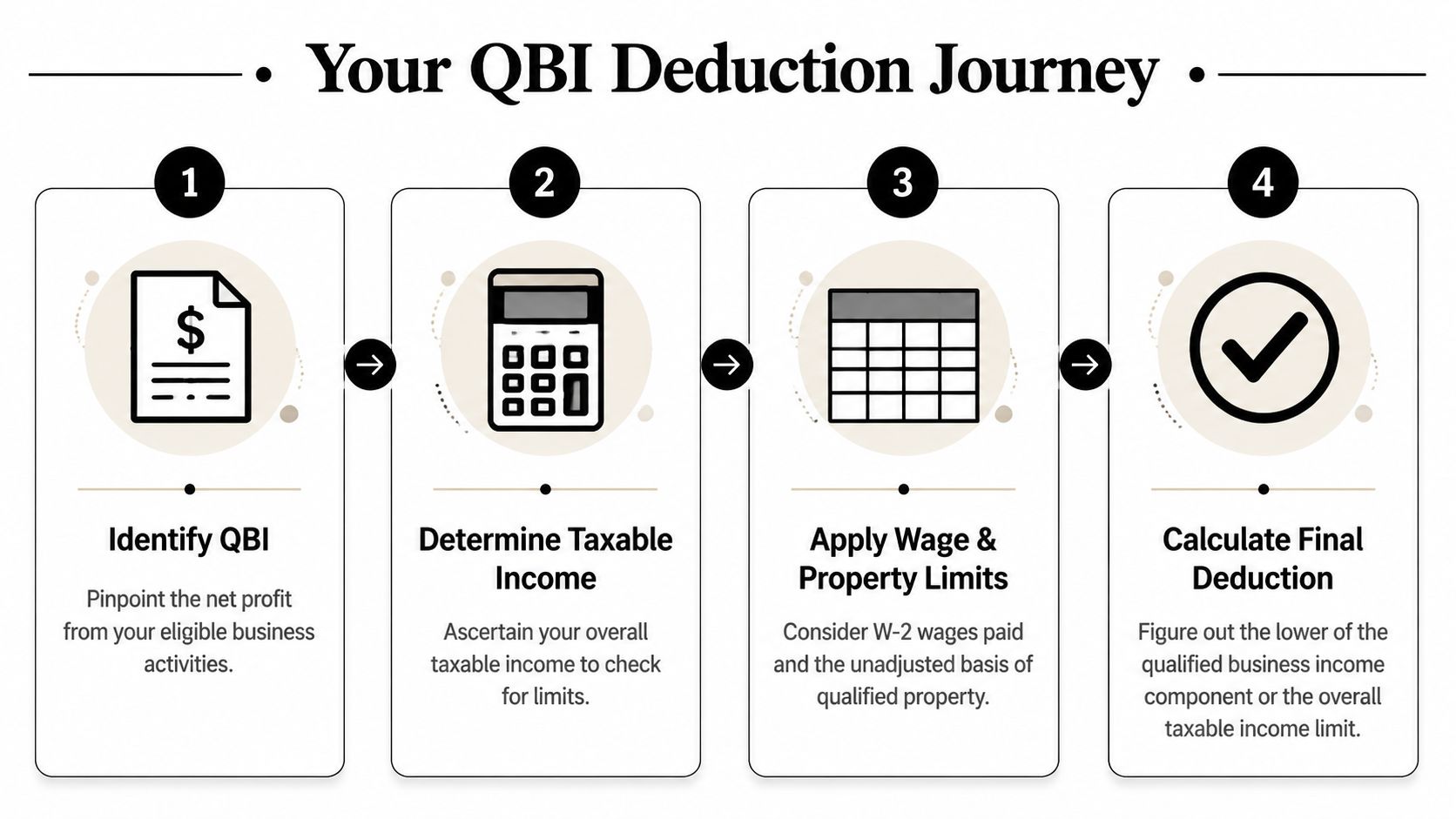

How to Calculate Your QBI Deduction with Examples

A Jacksonville business owner sits down in March, sees solid profit on the books, and assumes the 20 qbi deduction is just 20 percent of that number.

That assumption is how money gets left on the table.

The calculation starts with qualified business income, then runs through limits tied to taxable income, business type, W-2 wages, and sometimes depreciable property. If your books are messy or your entity structure is off, the deduction shrinks fast. For Northeast Florida owners in construction and healthcare, the difference can be material.

Start with the process flow below. It gives you the basic path, but the actual work is in the details.

A short video can also help if you want a quick visual overview before getting into the examples.

Example one with a straightforward sole proprietor

Say a Jacksonville freelance designer reports $80,000 of net profit on Schedule C and her taxable income stays below the threshold discussed earlier. In that situation, the starting point is usually simple. Her tentative QBI deduction is 20 percent of qualified business income, or $16,000, subject to the overall taxable income limit.

Simple is not the same as safe.

If she buried personal expenses in the business, missed deductible expenses, or misclassified inventory and direct job costs, the profit number is wrong. Once that number is wrong, the deduction is wrong. Owners in construction run into this constantly because direct materials, subcontractor costs, and job-related purchases often get lumped together carelessly. If you need to clean up margins before they hit the tax return, this guide on how to calculate cost of goods sold is a good starting point.

Example two with a construction S corporation

Now take a Northeast Florida contractor operating as an S corporation. The business shows $300,000 of qualified business income, pays the owner $90,000 in W-2 wages, and has taxable income high enough that wage limits matter.

Here is the quick math. Twenty percent of QBI is $60,000. But above the threshold, the deduction can be limited by W-2 wages or by a wage-and-property formula. If 50 percent of W-2 wages is $45,000, the deduction may be capped there unless the property calculation produces a better result.

That is why owner salary planning matters so much in construction. Too many S corp owners pick a payroll number for cash flow reasons and never test the tax impact. Then they find out after year-end that they cut their own deduction. A contractor with trucks, equipment, and depreciable assets may get some support from the property side of the formula, but you do not guess at this. You model it before December.

My advice is simple. If you own a construction company in Jacksonville, do not set shareholder salary by habit. Set it with a tax projection.

Example three with a healthcare partnership

Now look at a two-owner medical practice. The partnership earns $400,000, and each doctor is allocated $200,000. On paper, the 20 percent deduction looks like $40,000 per owner.

Healthcare is where owners get tripped up.

A medical practice is usually a specified service trade or business, so once taxable income moves into the phaseout range, the deduction can be reduced or wiped out. The answer is not sitting in one screen inside tax software. You have to test the owners' taxable income, confirm the SSTB treatment, review any related entities, and make sure the K-1 reporting matches the actual economics of the practice.

This is the point where professional help stops being a nice extra and becomes a money decision. A physician group, dental practice, therapy clinic, or specialty provider in Northeast Florida can lose a valid deduction by treating QBI like a basic worksheet. They can also create problems by claiming too much. Both outcomes are expensive.

A good CPA does more than fill in boxes. A good CPA checks whether the books support the deduction, whether compensation and allocations were handled correctly, and whether the return can survive questions later. That is how you keep more of the deduction you deserve without creating a bigger tax problem next year.

Advanced QBI Strategies Your Competitors Miss

A Jacksonville contractor closes the year with decent profit, three related LLCs, and no clear plan for how those entities affect the deduction. A medical practice in Northeast Florida has solid earnings, but the owners never tested whether the structure is helping or hurting QBI. That is how businesses leave money on the table.

Real QBI strategy starts before year-end. In some cases, it starts before you form the entity.

For construction companies, healthcare groups, and management entities tied to professional practices, the biggest missed opportunities usually come from two areas. Low-income year planning and multi-entity design.

Low-income years still deserve planning

Small-profit years get ignored too often. That is a mistake.

Beginning in 2026, the law provides a minimum deduction for certain taxpayers with modest qualified business income. If your income is uneven, that rule can matter more than owners expect. A seasonal subcontractor, a newer therapy practice, or a side business with stop-and-start revenue can still benefit if the books are clean and the timing is handled correctly.

That does not mean forcing income into a return or playing games with expenses. It means knowing where you stand before December 31, making sure cutoff is correct, and keeping records that support the position. If receipts, deposits, and vendor charges are scattered across email, glove compartments, and personal cards, start by fixing that with a better system for organizing tax receipts and backup documents.

Owners who wait until tax season usually lose this kind of opportunity.

Multi-entity businesses need intentional design

A lot of successful businesses in Jacksonville do not run through one tidy entity. The owner may have an operating company, a building LLC, an equipment entity, or a management company. That structure can be smart for liability and operations. It can also create confusion fast if nobody is looking at QBI across the full picture.

As Ramp's guide on the QBI deduction highlights, QBI is calculated at the entity level and then applied on the owner's return, so structure matters. Separating an SSTB from a non-SSTB real estate holding can affect how phaseout rules hit the overall plan, as discussed in Ramp's article on the qualified business income deduction.

That point matters in actual practice, not just in tax theory.

Here are three situations I see often in Northeast Florida:

- Construction company with multiple LLCs: Separate entities may help with jobs, equipment, or liability, but they often create messy books, unclear intercompany charges, and weak reporting. If you cannot explain which entity earned what, your deduction is exposed.

- Physician or dentist who owns the practice and the building: The practice may be an SSTB. The building entity may not be. How rent is set, documented, and reported can affect the tax result.

- Management company tied to a nonprofit-adjacent or healthcare operation: The lines between service income, support functions, and shared costs need to be clear. If they are not, the structure becomes a tax problem instead of a tax plan.

Good structure works like a job site blueprint. If the framing is crooked, everything built on top of it costs more to fix.

Strategy beats after-the-fact preparation

A return preparer records history. A CPA doing real planning shapes decisions while there is still time to act.

That means asking better questions before year-end, not after the return is already boxed in. The same discipline behind Numeric insights on big money decisions applies here. You should test multiple outcomes before you commit to compensation, distributions, rent arrangements, or entity changes.

| Decision area | Question that saves money |

|---|---|

| Entity design | Does this setup support the deduction, or is it creating avoidable phaseout and reporting problems? |

| Owner compensation | Is pay set with a tax projection, or did you just repeat last year's number? |

| Intercompany activity | Are rent, management fees, and shared expenses documented clearly enough to hold up under scrutiny? |

| Related businesses | Do the entities work together in a way that helps the owner, or are they just making the return harder to defend? |

This is why professional guidance is not optional for serious owners. QBI planning crosses bookkeeping, entity structure, compensation, and compliance. Miss one piece and the deduction can shrink, disappear, or create questions you do not want to answer later.

The Bookkeeping You Need for an Audit-Proof Deduction

A Jacksonville contractor lands a strong quarter, buys equipment, pays a crew, takes owner draws, then hands a shoebox of receipts to the tax preparer in March. A medical practice does the same thing with payroll reports, loan statements, and a few personal charges mixed into the business card. Both owners think they are buying a tax return. What they are really buying is risk.

The QBI deduction lives or dies on the quality of your books. If your records are sloppy, your deduction is shaky. If the IRS asks questions, you need clean support for how income, wages, and assets were recorded. Good intentions do not count.

What has to be documented correctly

This section is not about theory. It is about whether your records can support the deduction you plan to claim.

Your bookkeeping needs to show these items clearly:

- Accurate profit and loss reporting: QBI starts with real business profit. That means income posted to the right period, expenses coded correctly, and no personal spending buried in business accounts.

- Clean payroll records: If W-2 wages affect your deduction, payroll has to match the return, the payroll filings, and the books. Construction companies with field crews and healthcare practices with doctors, nurses, and admin staff get this wrong all the time.

- Asset detail: Equipment, vehicles, furniture, and improvements need purchase dates, cost, and proper classification. If qualified property matters to the calculation, vague fixed-asset accounts will not save you.

- Owner transactions: Draws, distributions, guaranteed payments, and reimbursements need to be separated and labeled correctly. Mixing them together distorts QBI fast.

- Entity-by-entity separation: If you run a practice entity, a real estate entity, or a management company, each one needs its own books and clear intercompany entries.

Where DIY books break down

The trouble usually starts in the gray areas.

A truck payment gets split wrong between principal, interest, and personal use. An owner health insurance payment lands in the wrong expense account. Payroll is posted from bank activity instead of payroll reports. A reimbursement gets treated like income. None of those mistakes look dramatic on their own. Together, they can change the deduction and make the return hard to defend.

Jacksonville construction companies feel this in job costing, subcontractor payments, and equipment purchases. Healthcare practices run into it with owner compensation, staff payroll, and shared expenses across entities. Those are not small details. They are the points where QBI calculations drift off course.

If you want a better framework before making year-end decisions, I like Numeric insights on big money decisions. The lesson is simple. Run multiple scenarios before you commit. That approach works for salary changes, major purchases, and entity-level decisions tied to QBI.

Clean books give your CPA something to work with. Messy books force your CPA to guess, and guessing is expensive.

The records small businesses should organize now

Start with the documents that support the entries on the books. Keep receipts, payroll reports, fixed asset invoices, loan statements, owner distribution logs, and year-end adjustment support in one place. If your records are spread across glove boxes, email threads, and phone photos, fix that now with this guide on how to organize receipts for taxes.

Then go one step further. Reconcile bank and credit card accounts every month. Review payroll against the general ledger. Track fixed assets as they are purchased, not months later. Separate business and personal spending without exceptions.

That is how you make the deduction defensible. It is also why a real CPA matters. Software can sort transactions. A professional accountant makes sure the books support the tax position, the tax position matches the return, and the return can stand up if anyone asks questions later.

Stop Guessing and Start Strategizing with a CPA

The 20 qbi deduction rewards owners who plan early and document everything. It punishes owners who guess.

By now, the pattern should be obvious. Your result depends on more than “did I make a profit?” It depends on your entity type, your taxable income, whether your business falls into SSTB treatment, how payroll is handled, how assets are tracked, and whether multiple entities are structured intelligently. That is not a side task for a busy owner.

Jacksonville businesses especially need practical tax guidance, not abstract theory. Construction companies need job-costing discipline and payroll structure. Healthcare practices need someone who understands service-business limitations and owner compensation. Nonprofits and affiliated management entities need compliant reporting that doesn't collapse under scrutiny. Growing companies need someone who can act like a fractional CFO, not just a once-a-year tax filer.

If you're still trying to piece this together after the year ends, you're already behind. QBI planning belongs in your monthly financial review, your payroll setup, your bookkeeping process, and your entity strategy. That's why working with a real tax advisor matters. Not because the rule is impossible to understand, but because the cost of getting it wrong is too high.

If you need a starting point for professional support, review what a dedicated small business tax professional handles. Then ask yourself a blunt question. Do you want to hope your deduction is right, or do you want to know?

If you want clear answers on the 20 qbi deduction, clean books, stronger compliance, and ongoing financial guidance, talk to Bookkeeping and Accounting of Florida Inc.. Their Jacksonville team helps small and midsize businesses with bookkeeping, payroll, tax preparation, audits, and fractional CFO support, so you can stop guessing, stay compliant, and make better business decisions with confidence.