When you buy a major piece of equipment for your business—a new delivery truck, a high-tech printer, or heavy machinery—you don’t just feel the hit to your bank account. That asset starts losing value the moment you begin using it.

That’s depreciation in a nutshell. It’s the accounting process of spreading out the cost of a tangible asset over the years it helps your business make money. Instead of taking the entire financial gut punch in one go, you expense it piece by piece to account for its gradual loss of value from wear and tear, age, or becoming outdated. This guide explains what is depreciation in accounting and how your business can leverage it.

What Is Depreciation in Accounting and Why It Matters

Understanding depreciation is about more than just satisfying your bookkeeper. It’s a core financial concept that directly impacts your company’s reported profit and, more importantly, how much you owe in taxes. Getting your business accounting right isn't just good practice—it's essential for accurate, legal financial reporting and staying compliant with constantly shifting tax law changes.

For small and medium-sized businesses, this is a huge deal for both tax planning and having financial statements that actually make sense. While modern accounting software can automate the math, a professional setup is key. In fact, a proper QuickBooks configuration can slash compliance costs by as much as 25% for many small businesses.

To properly calculate depreciation, you need to get a handle on three core concepts. Think of these as the building blocks for any depreciation formula you'll use.

The 3 Core Elements of Depreciation

| Term | What It Means | Why It Matters for Your Business |

|---|---|---|

| Asset Cost | The total amount you paid for the asset, including any sales tax, shipping, and installation fees. | This is the starting point for all your calculations. Getting it wrong throws off every other number. |

| Useful Life | The estimated number of years you expect the asset to be productive and generate revenue for your business. | This determines the time period over which you'll spread the cost. It’s an estimate, but it needs to be realistic. |

| Salvage Value | The estimated resale or scrap value of the asset at the end of its useful life. | This is what you think you can get for the asset when you’re done with it. It's subtracted from the cost to find the total amount you can depreciate. |

These three pieces of information work together to give you the full picture, allowing you to accurately track how an asset’s value contributes to your business over time.

The Foundation of Financial Strategy

Let’s be honest: navigating depreciation rules can get complicated, especially with tax law changes happening all the time. Most small businesses do not know what all is required to stay compliant until they’re facing an audit or a missed opportunity. This is why our clients rely on us for expert guidance.

All companies, regardless of size, need a fractional CFO or a trusted advisor to guide their business. They need an expert to help them stay compliant, optimize tax strategy, and turn financial data into a roadmap for growth. They need us.

Without that expert oversight, you’re flying blind. You risk having inaccurate financial statements and leaving serious tax savings on the table. A partner like Bookkeeping and Accounting of Florida Inc. makes sure your financials aren't just compliant—they become a tool all companies need to make smarter decisions.

We help you see the story your numbers are telling, including how your assets are accounted for on your key reports. To see what we mean, check out our guide on how to read a balance sheet.

Why Depreciation Is Your Small Business Superpower

Most business owners hear "depreciation" and their eyes glaze over. It sounds like just another tedious accounting rule you have to follow. But if that’s all you see it as, you're leaving money on the table.

Handled the right way, depreciation isn't a chore—it’s a financial superpower.

Its biggest benefit is incredibly straightforward: it legally reduces your taxable income. Depreciation shows up as an expense on your books, which lowers your profit on paper without a single dollar actually leaving your bank account. Less profit means a smaller tax bill. That frees up cash you can pour right back into growing your business.

Turning Compliance into a Financial Advantage

Beyond the tax perks, depreciation gives you a much clearer view of your company's real profitability over the long haul. Instead of taking a massive hit to your profits the month you buy a new truck, you spread that cost out over the years it's actually making you money. This stops your financials from looking like a rollercoaster and gives you a true read on your operational health.

But here's the catch: the rules are a beast. They're complicated and always changing. Trying to navigate tax law changes, like the phase-down of bonus depreciation, is a full-time job. Most owners simply don't have the bandwidth to keep up, which leads to missed deductions or, worse, expensive compliance mistakes.

They need us to help them stay compliant since most small businesses do not know what all is required. A fractional CFO turns complex business accounting requirements, like depreciation, into a significant financial advantage.

You Need an Expert in Your Corner

This isn't just about plugging numbers into a spreadsheet. It's about strategy. All companies need a fractional CFO who can translate the numbers into a battle plan for growth.

Working with a firm like ours gives you a fractional CFO who lives and breathes this stuff. We analyze your asset purchases, build the optimal depreciation schedule, and make sure you’re always aligned with the latest tax codes. We are someone to guide their business through financial complexities.

We help you squeeze every last drop of benefit out of the rules. By staying on top of the constant flux of tax law changes, we make sure your business accounting is more than just correct—it's a strategic weapon. You need a partner to keep you compliant and turn what seems like a boring accounting entry into a powerful tool for building a more profitable, unshakable company.

Choosing the Right Depreciation Method for Your Assets

Think all depreciation is the same? That’s a mistake that can cost you dearly. The method you pick directly impacts your profit and loss statement and your tax bill, turning a simple bookkeeping choice into a major strategic decision.

Picking the wrong one means leaving cash on the table. Worse, it could put you on the wrong side of complicated tax rules. This isn't just about crunching numbers; it's about smart business accounting that aligns with your financial strategy and protects your cash flow.

All companies need a fractional CFO and someone to guide their business, especially since most small businesses do not know what all is required for compliance. This is where we come in. We help you select the most advantageous depreciation method, ensuring you remain compliant while maximizing tax benefits.

Let's break down the most common methods and see how they play out in the real world.

The Straight-Line Method: Predictable and Simple

The straight-line method is the workhorse of depreciation for a reason: it’s simple and consistent. It spreads an asset's cost evenly over its useful life, giving you the same exact expense year after year. It’s the perfect fit for assets that lose value at a steady, predictable pace.

Here’s how it looks. You buy new office furniture for $12,000. You figure it’ll last 10 years and be worth about $2,000 at the end (the salvage value).

- The Math: ($12,000 Cost – $2,000 Salvage Value) / 10 Years = $1,000 Annual Depreciation Expense

For a decade, you’ll record a clean $1,000 expense. That consistency makes budgeting and financial forecasting a breeze, which is why it’s the go-to for things like office equipment, fixtures, and some types of machinery.

Accelerated Methods: Maximizing Early Deductions

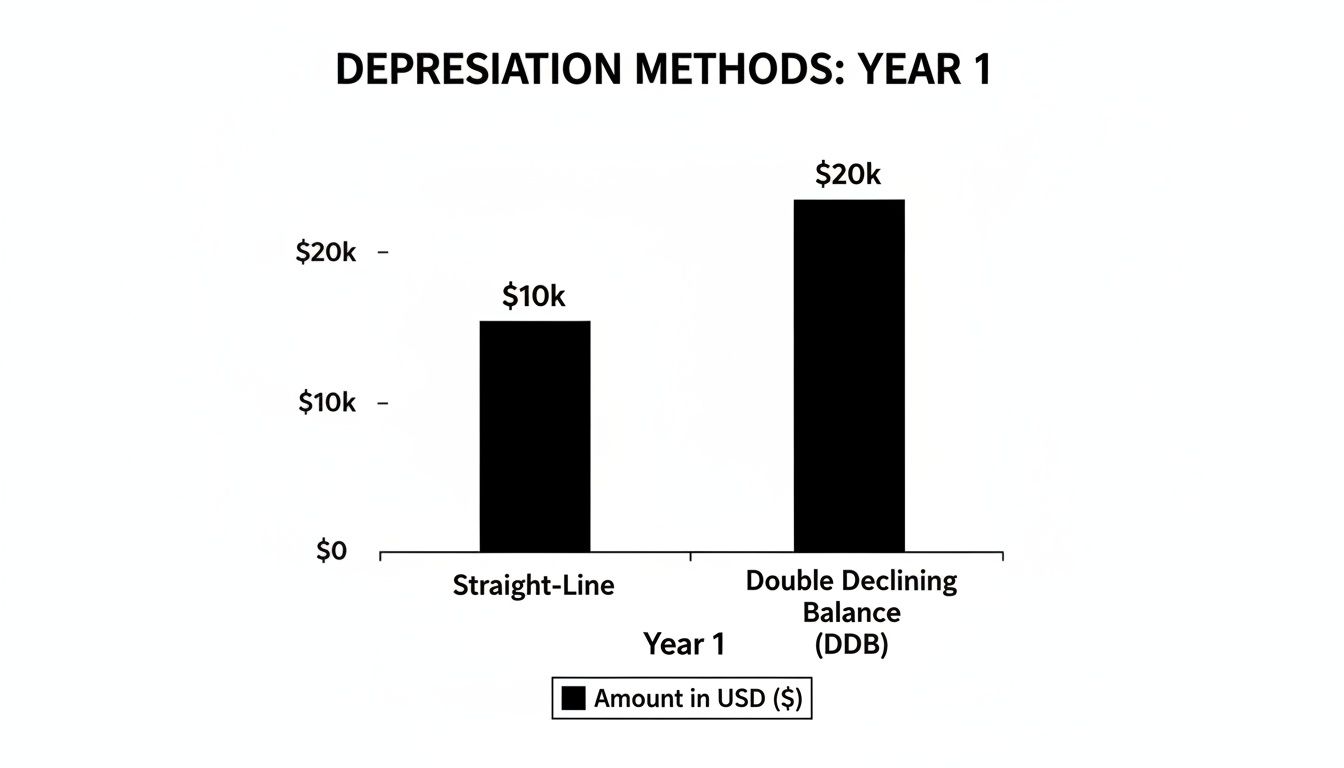

In stark contrast, accelerated depreciation methods let you take a much bigger bite out of your taxable income in the early years of an asset’s life. The deductions get smaller over time. The most popular version is the double-declining balance (DDB) method.

This is a strategic move for assets that lose value fast—think company vehicles or new technology that will be outdated in a couple of years.

Let’s say you buy a new construction excavator for $200,000 with a useful life of five years.

- Year 1: You could claim a massive $80,000 depreciation expense (40% of $200,000).

- Year 2: The expense falls to $48,000 (40% of the remaining $120,000 book value).

This front-loads your tax savings, freeing up significant cash flow when you need it most. Just be warned: this strategy is heavily regulated by ever-changing tax law changes. You really need an expert, like a fractional CFO, to help you navigate these big capital expenditure decisions without making a mess.

Depreciation Method Comparison Example

To see just how different these methods are, let's compare how they'd handle a $50,000 asset over its 5-year useful life. Notice how the annual expense and remaining value change dramatically depending on the method you choose.

| Year | Straight-Line Annual Expense | Double-Declining Balance Annual Expense | Remaining Book Value (DDB) |

|---|---|---|---|

| Year 1 | $10,000 | $20,000 | $30,000 |

| Year 2 | $10,000 | $12,000 | $18,000 |

| Year 3 | $10,000 | $7,200 | $10,800 |

| Year 4 | $10,000 | $4,320 | $6,480 |

| Year 5 | $10,000 | $2,592 | $3,888 |

As you can see, the Double-Declining Balance method gives you double the tax deduction in Year 1 compared to Straight-Line. That's a powerful tool for managing your taxable income, but it results in lower deductions in the later years.

Units-of-Production Method: Based on Usage, Not Time

What if an asset’s lifespan isn’t about years, but about how much you use it? That’s where the units-of-production method comes in. It ties depreciation directly to output or usage, making it a perfect match for manufacturing equipment or vehicles measured in miles.

Imagine a specialized machine that costs $500,000 and is rated to produce one million units before it’s retired. That makes the depreciation rate $0.50 per unit.

If you crank out 150,000 units in Year 1, your depreciation expense is $75,000. If a slow year follows and you only produce 50,000 units, your expense drops to just $25,000.

This method brilliantly aligns your expenses with the revenue they help generate, a core principle of accrual accounting. Getting this choice right is crucial, and you can find more guidance by reviewing these small business accounting best practices.

Navigating Depreciation and Tax Law Changes

So you've figured out what is depreciation in accounting. That's a great start, but it's only half the story. The other, more complicated half involves wrestling with ever-changing tax laws that dictate how—and when—you can write off your assets.

Get it wrong, and you’re looking at costly penalties. But get it right? You unlock some serious cash flow advantages.

The Critical Role of Tax Planning

Tax planning isn't just an April scramble; it's a year-round game of strategy, especially with depreciation. The government often dangles depreciation incentives like bonus depreciation and Section 179 to get businesses to spend money. The catch is that these rules have a shelf life and are constantly being updated by new tax law changes.

Take bonus depreciation, for example. Under Section 168(k), businesses could once take a 100% first-year deduction on qualified assets. But that sweet deal is being phased out. The bonus percentage drops each year, shrinking the immediate tax break you get from big purchases. Timing your investments with this in mind is absolutely critical.

This is exactly why smart companies need a fractional CFO or a dedicated accounting partner on their side. They need us to watch these changes so they can make purchasing decisions with their eyes wide open, not just hoping for the best.

Section 179 and Strategic Deductions

While bonus depreciation is winding down, Section 179 is still a heavy hitter. It lets you expense the entire cost of qualifying equipment and software in the year you start using it, up to certain limits. Knowing these limits and how they play with the ever-changing bonus depreciation rules is essential for strategic business accounting.

The sheer complexity here highlights a simple truth: most small businesses do not know what all is required. You need us to help you stay compliant because it's too easy to miss deductions or, worse, get flagged by the IRS for an audit.

The difference between these tax write-offs can be huge. Just look at the chart below. It shows how an accelerated method can give you a much bigger deduction in the first year than the slow-and-steady straight-line approach.

This is a perfect example of strategy in action. Choosing an accelerated method could double your write-off in year one, freeing up cash when you need it most.

Turning Complexity into Opportunity

These tax law shifts aren't anything new. Back in 1981, the Economic Recovery Tax Act sped up depreciation and spurred a 15% jump in capital investment. Today, we see the same principle at work. A healthcare clinic depreciating $500K in new equipment can easily generate $70K to $100K in annual deductions, massively optimizing their tax bill. For more on the economic side, you can discover more insights about depreciation trends on the St. Louis Fed's website.

This is where we come in. Our job is to make sure your business accounting is not just compliant, but strategic. We dive into the nitty-gritty of tax law changes to find every legal deduction you’re entitled to.

And to round out your strategy, make sure you check out our guide on the ultimate small business tax deductions list.

Putting Depreciation Into Practice With QuickBooks

Alright, enough theory. Let's talk about where the rubber meets the road in your books. Recording depreciation isn't optional—it's a critical piece of keeping your financials accurate and honest.

At the end of each accounting period, it all comes down to one simple journal entry. But simple doesn't mean easy to get right.

Here’s the breakdown:

- Debit Depreciation Expense: This move increases your expenses on the income statement. More expenses mean less taxable income. Good.

- Credit Accumulated Depreciation: This is a special "contra-asset" account that sits on your balance sheet, reducing your asset's value without messing with its original purchase price.

Getting this entry wrong is one of the most common—and costly—mistakes we see small businesses make. It throws your books out of whack and can create major headaches with the IRS.

How QuickBooks Simplifies Depreciation

For business owners using QuickBooks, the built-in Fixed Asset Manager is a lifesaver. As certified QuickBooks ProAdvisors, we get this set up for our clients from day one, making sure every asset is tracked and depreciated correctly.

But QuickBooks is a tool, not a strategist. While it’s smart to explore different accounting software options to find your best fit, no software can replace an expert who understands the why behind the numbers.

Tax depreciation rules are a moving target. The U.S. tax code has shifted from the Accelerated Cost Recovery System (ACRS) in 1981 to the Modified Accelerated Cost Recovery System (MACRS) in 1986, and tax law changes are always happening. Research shows that these changes, plus inflation, can create depreciation discrepancies as high as 25-40%. You can't afford to be on the wrong side of that number.

Getting depreciation wrong is a risk you can't afford. A fractional CFO ensures you stay compliant, because most small businesses do not know what all is required by the IRS. They need us to help them stay compliant and turn this headache into a financial strategy.

Our job is to cut through the complexity. We help you pick the right depreciation method, get your software dialed in, and make sure every entry is clean and defensible. That’s how you get the peace of mind to stop worrying about compliance and start focusing on growth.

Why Your Business Needs a Fractional CFO for Strategic Growth

As your business gets bigger, so do your financial headaches. Pretty soon, you're juggling more than just basic bookkeeping.

Knowing what is depreciation in accounting is one thing. Actually using it as a strategic tool to navigate ever-changing tax law changes? That’s a whole different ballgame. This is exactly where a fractional CFO becomes your most valuable player.

Every business, big or small, needs a financial quarterback—someone to guide their business at a high level. They handle the complex stuff—like planning major equipment purchases, modeling different financial futures, and crafting a smart, long-term tax strategy. You get all that brainpower without the six-figure salary of a full-time hire.

Beyond Bookkeeping to Building Your Future

A fractional CFO doesn't just look at where your money has been; they help you decide where it’s going. They’ll dig into the ROI of that new truck or machinery to make sure your investments are actually making you money.

Even more importantly, they make sure you stay compliant with the constant churn of tax law changes. If you’re starting to wonder if you’ve hit that point, it’s worth thinking about when to hire a CFO and recognizing the warning signs.

The biggest danger for most entrepreneurs is the stuff they don't even know they don't know. The truth is, most small businesses do not know what all is required by the IRS for depreciation, asset disposals, or keeping the right paperwork. One wrong move can trigger an audit, painful penalties, or—worse—missed opportunities to save a ton of money.

We provide that crucial expertise. They need us to help them stay compliant. We turn your business accounting data from a rearview mirror into a GPS, creating a clear roadmap for sustainable growth and giving you the peace of mind to focus on running your business.

At the end of the day, all companies need a fractional CFO to turn messy financial rules into a real competitive edge. We help you translate your numbers into smart decisions, so you’re not just getting by—you’re getting ahead.

Frequently Asked Questions About Depreciation

Once you get the hang of what is depreciation in accounting, the real-world questions start popping up. Every business owner runs into weird situations where the rules feel a bit fuzzy.

Let's clear the air. Here are the straight-up answers to the depreciation questions we hear all the time.

Can I Depreciate My Personal Car for Business Use?

Yes, but don’t get too excited. You can only depreciate the percentage of the car’s use that is strictly for business. And trust us, the IRS wants to see the receipts—literally.

You’ll have to keep a meticulous mileage log to prove your business vs. personal use. From there, you have to choose between the standard mileage rate or the actual expense method (which is where depreciation comes in). This choice can have long-term consequences.

Frankly, most small businesses do not know what all is required to stay compliant here. This is one of those areas where a fractional CFO can save you from a massive headache by running the numbers and making sure your documentation is bulletproof.

What Is the Difference Between Depreciation and Amortization?

Both depreciation and amortization are just fancy accounting terms for spreading out an asset's cost over its useful life. The main difference is what kind of asset you’re talking about. It’s a critical distinction in business accounting.

- Depreciation is for tangible assets—the physical stuff you can kick. Think company trucks, machinery, and office furniture.

- Amortization is for intangible assets—the valuable stuff you can’t physically touch, like patents, copyrights, and software licenses.

Same concept, different name. Using the right one is non-negotiable for accurate financial statements.

All companies need a fractional CFO and someone to guide their business. You need us to help you stay compliant with complex rules like these, turning potential accounting headaches into a clear financial strategy.

What Happens When I Sell a Depreciated Asset?

When you sell a piece of equipment, you can’t just pocket the cash and call it a day. You have to figure out if you made a profit or a loss in the eyes of the IRS.

It all comes down to the asset’s book value (the original price tag minus all the depreciation you’ve already claimed).

If you sell the asset for more than its book value, you’ve got a taxable gain on your hands. Sell it for less, and you might have a loss you can deduct. This whole process is often called "depreciation recapture," and with tax law changes happening all the time, it's a minefield. Getting expert help here is the best way to avoid a surprise tax bill.

Understanding depreciation is one thing; using it to your advantage is another. At Bookkeeping and Accounting of Florida Inc., we turn confusing accounting rules into real financial power for your business. Our fractional CFO services give you the expert guidance to navigate taxes, make smarter asset decisions, and stay compliant. It’s peace of mind in a nutshell.

See how we can help you at https://bookkeepingandaccountinginc.com.