You know the feeling. Payroll hits, the month was slow, and the labor number still looks fat. Inventory says you bought enough material for three jobs, but you only finished two. A vendor invoice gets paid twice, or a refund shows up in the bank and nobody in the office can explain it cleanly.

That’s usually where this starts.

Most Jacksonville business owners don’t call because they’ve proven fraud. They call because the numbers stopped making sense, and that nagging feeling won’t go away. In construction, it might be job costs drifting with no operational reason. In a healthcare practice, it might be billing activity that doesn’t line up with provider schedules. In a non-profit, it might be restricted funds that somehow don’t stay where they were supposed to stay.

The mistake is waiting for a smoking gun. Fraud rarely announces itself. It leaks through small inconsistencies, bad explanations, and books that feel a little too hard to trust. If you’ve been reviewing statements and thinking, “Something’s off, but I can’t prove it,” you’re exactly the kind of business owner who needs a forensic accounting fraud investigation.

And the timing matters more now than most owners realize. Tax rules shift. filing requirements change. Payroll, sales tax, contractor reporting, reimbursement rules, grant restrictions, and documentation standards don’t get simpler with time. In that environment, weak bookkeeping doesn’t just create confusion. It creates cover.

If you want a plain-English primer on spotting fraud in financial statements, that’s a useful outside resource. And if you want a practical look at warning signs before things get ugly, this piece on spotting financial fraud before it wears a mustache and disappears is worth your time.

That Gut Feeling Your Numbers Are Wrong

A lot of owners think they’re overreacting.

They’re not.

I’ve seen plenty of situations where the first red flag was boring. Not dramatic. Not criminal-looking. Just boring enough to get ignored. A payroll report that looked too high for a slow month. Materials purchased faster than jobs were closing. Credit card charges rounded in ways that didn’t fit normal purchasing. Deposit timing that kept drifting.

What your gut is really telling you

Your gut usually isn’t telling you the exact scheme. It’s telling you that the story and the math no longer match.

That matters because fraud, sloppiness, and weak controls often produce the same first symptom. Confusion. If your office manager says one thing, your bank feed says another, and your P&L tells a third story, you’ve got a problem, whether it's theft, bad process, or both.

Practical rule: If you need three conversations to explain one transaction, you probably need outside review.

Owners often wait because they don’t want to accuse a loyal employee. That’s understandable. It’s also how losses keep growing. A forensic review doesn’t start with blame. It starts with evidence.

Why this is harder now

Small business finances are more layered than they used to be. You’ve got cloud accounting, app integrations, payroll systems, card processors, reimbursement platforms, ACH payments, and tax filing obligations stacked on top of each other. Add tax law changes and compliance pressure, and a business owner can miss a real issue because the reporting chain is messy.

That’s why I’m direct about this. You shouldn’t try to solve a suspected fraud issue with guesswork, and you shouldn’t treat compliance as an afterthought. Clean books, documented controls, and regular oversight aren’t luxury items anymore. They’re the floor.

What Is Forensic Accounting Really

A regular accountant helps you keep score. A forensic accountant figures out what happened when the score looks wrong.

That’s the simplest way to think about it.

The financial detective analogy

A standard audit is like a traffic cop. It checks whether rules were followed and whether reporting appears reasonable.

A forensic accounting fraud investigation is more like a financial detective. It follows money, tests explanations, examines documents, and looks for evidence that will hold up under scrutiny. That last part is the big distinction. This work isn’t just about finding something odd. It’s about building an evidence trail.

If you suspect payroll fraud, ghost vendors, expense abuse, billing manipulation, or diverted receipts, you don’t need broad reassurance. You need proof. Or you need proof that nothing improper happened. Both outcomes have value.

Where this work started

The profession has old roots, and the origin story is still useful. The field of forensic accounting was invented in the 1920s when IRS accountant Frank Wilson investigated organized crime leader Al Capone's financial records. Unable to prosecute Capone on his more notorious crimes through conventional evidence gathering, Wilson meticulously analyzed stacks of financial statements and records and uncovered enough evidence to secure Capone’s conviction on 23 counts of tax evasion. That case established the principle that financial records can serve as definitive evidence when direct proof is unavailable, as described by William & Mary’s overview of forensic accounting and fraud examination.

That story matters for one reason. Paper trails still talk.

A thief can lie. A bad employee can delete emails. A manager can give you a polished explanation. But money moves in patterns, and records usually leave fingerprints.

Why small businesses need it too

Some owners hear “forensic accounting” and think lawsuits, giant corporations, and national scandals. Wrong category.

Small and mid-sized businesses need this work just as much because they usually have fewer layers of review. In a big company, one person might approve purchases, another records them, and another reconciles the account. In a small business, one trusted employee may touch all three steps. That’s convenient until it isn’t.

Here’s a quick way to separate the services:

| Service | Main purpose | End result |

|---|---|---|

| Bookkeeping | Record transactions accurately | Clean day-to-day financials |

| Audit or review | Check reporting and compliance | Assurance over statements |

| Forensic accounting | Investigate suspicious activity | Evidence, findings, and support for action |

Later in the process, visual explanations can help owners understand what the work looks like in practice.

What the work usually uncovers

Sometimes it uncovers fraud. Sometimes it uncovers weak controls, duplicate payments, process breakdowns, undocumented reimbursements, or tax and compliance exposure. Those aren’t small issues. They affect profit, cash flow, and your ability to defend your records if a regulator, lender, board member, or attorney asks hard questions.

Financial clarity isn’t just about knowing your profit. It’s about knowing whether the records deserve your trust.

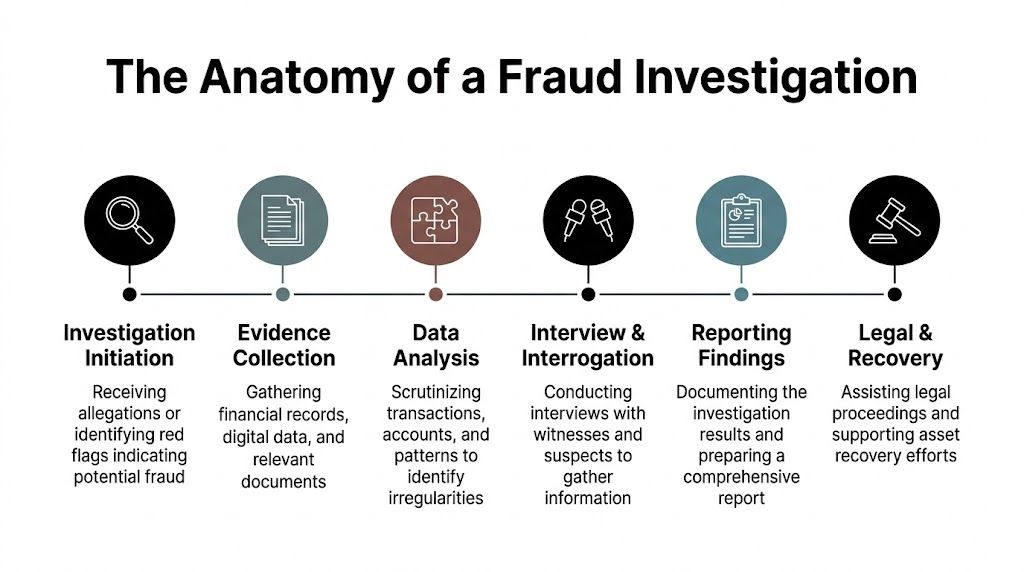

The Anatomy of a Fraud Investigation

A fraud investigation should answer one question fast. What happened, how much did it cost you, and how do you stop it from happening again?

For a Jacksonville contractor, that question might start with job costs that keep drifting higher without a clean explanation. For a medical practice, it may be adjustments and write-offs that no one can explain clearly. For a non-profit, it could be restricted funds getting muddy inside everyday operating expenses. Different industries. Same problem. If you wait too long, the records get messier and the fix gets more expensive.

Start with a tight question, not a broad accusation

Owners often open with, “I think someone is stealing.”

That is emotionally honest. It is also a poor starting point.

A useful investigation starts with a narrower issue that can be tested against records:

- Payroll concern: Labor cost climbed, but output and hours do not support it.

- Vendor concern: New payees showed up without solid setup documents or approval history.

- Revenue concern: Deposits do not match invoices, collections, or expected patient receipts.

- Grant or fund concern: Restricted money appears to cover general overhead or unrelated spending.

That framing matters because it determines what records need to be locked down first and which people should stay out of the review.

Secure the records before anyone “fixes” them

The first step is evidence preservation.

If a controller, office manager, or bookkeeper starts cleaning up entries after suspicions surface, you lose the ability to tell what happened and when. In serious cases, investigators create exact digital copies of devices and accounting files before review. That protects timing, edits, and deletion history.

The core record set usually includes:

- Bank records: Statements, check images, ACH details, wire activity

- Accounting data: General ledger, subledgers, audit logs, QuickBooks exports

- Support files: Invoices, receipts, contracts, purchase orders

- Communications: Emails, approval messages, vendor setup notes, internal chats

Small businesses miss this step all the time. Then they wonder why the story never gets clear.

Test the numbers for patterns that do not fit normal business activity

A proper investigation does more than read transactions line by line. It tests for patterns, timing, duplication, and behavior that falls outside the company’s normal flow.

That can include repeated invoice amounts, round-dollar payments, entries posted late at night, duplicate vendors with slightly different names, or payments set just under approval limits. Owners should care about this because these patterns often show up long before anyone catches the scheme.

A solid set of books makes this work much faster. If your records are sloppy, every review costs more. That is one reason small business fraud prevention starts with accurate books and review routines.

Field note: The goal is not to inspect every transaction with the same intensity. The goal is to isolate the few that deserve a closer look.

Follow the money through the mess

Once funds leave the business, they rarely sit in one obvious place. They move through operating accounts, payroll accounts, personal accounts, debit cards, and sometimes a vendor file that should never have been approved.

Funds tracing reconstructs that path. Aprio explains how forensic accountants use tracing methods to separate suspicious movement from legitimate activity in mixed accounts in its discussion of investigative techniques used in forensic accounting.

Here is the plain-English version. If somebody dumps clean water and dirty water into the same bucket, tracing work helps determine how the dirty water got in and where it spread. That matters if you need to recover losses, file a claim, explain the issue to a board, or fix tax reporting.

Interviews come after the document work, not before

By the time interviews start, the records should already point to the right questions.

Good interviews are structured and document-based. If an employee says a vendor was approved months before payments began, the file, approval trail, and emails should support that statement. If they do not, that gap matters.

Three rules keep owners out of trouble:

- Keep the circle small. Loose talk gives the wrong person time to delete files or shape a story.

- Do not run your own interrogation. Angry owner interviews create risk and muddy the record.

- Match every explanation to documents. Verbal answers alone are never enough.

The report should lead to action, not just tell a story

A useful forensic report gives you decisions to make. It should show what happened, how it happened, who had access, what records support the conclusion, and what corrections need to happen next.

| Question | Why it matters |

|---|---|

| What happened | You need facts, not office speculation |

| How it happened | This shows the control gap |

| Who had access | Opportunity matters when you assess responsibility |

| What records support the conclusion | Findings need to hold up with attorneys, lenders, insurers, or boards |

| What should happen next | You may need recovery steps, tax corrections, policy changes, or legal action |

For a small or midsize business, the best outcome is not “we found the problem.” The best outcome is “we fixed the weak spot before it drained more cash.”

That is why smart owners pair investigations with stronger internal controls to prevent fraud. In practice, that often means adding fractional CFO oversight, better approval rules, monthly balance sheet review, cleaner vendor onboarding, and industry-specific compliance checks. Bookkeeping and Accounting of Florida Inc. helps Jacksonville and Northeast Florida businesses put those routines in place before suspicion turns into a six-month cleanup.

A sloppy investigation costs money. A disciplined one gives you clarity, protects your position, and shows you exactly which process needs to change.

From Red Flags to Fortified Defenses

Most fraud content lives in cleanup mode. That’s backwards.

The cheaper move is prevention. Not paranoia. Prevention. If you run a construction company, medical practice, or non-profit in Northeast Florida, you don’t need a giant corporate compliance department. You do need structure, review, and someone senior enough to ask hard questions before a problem turns expensive.

The red flags aren’t the same in every industry

A generic fraud checklist won’t help much. Your business has its own weak points.

For construction, watch job-costing variances that never get explained cleanly, subcontractor billing that outpaces job progress, and vendors that appear once and vanish. Payroll is another hot spot, especially when timekeeping, field approval, and processing are separated poorly.

For healthcare, pay attention to billing patterns that don’t fit provider schedules, adjustments that increase without a clear operational reason, and reimbursement activity that staff can’t explain in plain language. If coding, billing, and reconciliation all live too close together, risk goes up.

For non-profits, the danger often sits in restricted funds, reimbursement practices, debit card use, and weak segregation around disbursements. Boards often assume mission-driven organizations are insulated from fraud. They aren’t.

Quarterly risk checks beat annual surprises

One of the more useful facts in this space is that fraud content often skips practical guidance for these industries, even though fraud losses in construction and healthcare average $150,000 per case, 40% of SMB frauds go undetected for years due to collusion, and forensic accountants recommend quarterly fraud risk assessments using tools like Benford’s Law on QuickBooks data, which can potentially reduce risk by 50%, according to Bonadio’s discussion of fraud investigations and forensic accounting.

That’s why I recommend a routine, not a panic response.

A quarterly fraud risk assessment can be simple and disciplined:

- Review user access: Who can create vendors, approve bills, cut checks, and edit prior-period entries?

- Test transaction patterns: Run anomaly checks on payroll, AP, reimbursements, and refunds.

- Inspect reconciliations: Make sure the person reconciling doesn’t also control disbursements.

- Look at exceptions: Credit memos, write-offs, voids, and manual journal entries deserve attention.

If you want a helpful outside read on internal controls to prevent fraud, that’s a solid place to pick up practical ideas. We also put together guidance on preventing small business fraud starts with your books because prevention is usually an accounting discipline problem before it becomes a legal problem.

Weak controls don’t just allow theft. They also make honest mistakes harder to catch.

Why a fractional CFO makes sense here

At this point, many owners stall. They agree they need tighter controls, but they don’t have the budget for a full-time senior finance hire.

That’s exactly why a fractional CFO model works. You get experienced oversight without full-time overhead. Someone reviews trends, pressure-tests reports, watches compliance, helps separate duties, and makes sure the books tell a believable story month after month.

That doesn’t replace your bookkeeper. It gives your bookkeeper adult supervision.

One practical option in Jacksonville is Bookkeeping and Accounting of Florida Inc., which provides bookkeeping, internal audit support, tax preparation, forensic audits, and fractional CFO services for small and growing businesses. For owners who need guidance without building a full internal finance department, that kind of setup is functional.

Why Your Jacksonville Business Needs a Local Expert

Fraud work is local in more ways than people think.

Yes, the accounting principles are universal. But the business context isn’t. A Jacksonville contractor, a local clinic, and a Northeast Florida non-profit each deal with their own vendor habits, staffing realities, tax deadlines, reporting pressures, and regional operating patterns. A local CPA sees those patterns faster.

Local knowledge changes the conversation

A remote provider may understand spreadsheets. That doesn’t mean they understand your environment.

A local expert can usually move faster on practical details:

- Industry context: Construction draws, payroll pressure, retainage, reimbursements, and job-costing quirks

- Healthcare realities: Payer mix, billing workflows, provider compensation issues, and documentation expectations

- Non-profit oversight: Board reporting, grant restrictions, fund tracking, and audit-readiness

And when a matter turns serious, being able to coordinate with local counsel, management, and stakeholders in real time helps.

What to look for before you hire

Don’t hire based on a polished website. Hire based on fit for the problem.

Use a simple screen:

| What to check | Why it matters |

|---|---|

| CPA background | You need technical accounting judgment |

| Fraud and investigation experience | Suspicion is different from proof |

| Ability to explain findings clearly | Owners need plain English, not jargon |

| Knowledge of internal controls | Fixing the breach matters as much as finding it |

| Tax and compliance awareness | Fraud issues often spill into filings and reporting |

You should also ask whether the firm can support the business after the investigation. A one-time report is useful. Ongoing oversight is better.

That’s where services like internal audits matter. Once you identify a weakness, you need a process to keep it from coming back.

This isn’t just about fraud

A lot of owners come in looking for an investigation and stay because they realize the deeper issue is financial leadership.

They don’t just need someone to catch a thief. They need someone to guide the business, keep the books compliant, interpret the numbers, and flag risks before tax filings, payroll reporting, or board reviews turn into a mess. Most small businesses don’t know everything that’s required of them. That’s not a moral failure. It’s a capacity issue.

A good finance advisor doesn’t just find problems. They help you run a cleaner business.

That’s why I push owners toward stronger monthly accounting discipline, senior review, and fractional CFO support. If your reporting is late, your reconciliations are weak, and your compliance depends on memory, you’re not managing risk. You’re borrowing luck.

Fraud in Northeast Florida Real Case Snapshots

The patterns repeat. The names change.

I’m not going to invent flashy case studies for effect. Real fraud usually looks smaller and more ordinary at the start than people expect. That’s why it survives.

Construction contractor with payroll drift

A local contractor noticed labor costs staying stubbornly high during a slower stretch. Nothing looked outrageous on a single payroll run. The problem sat in the trend.

The review found that time approval and payroll processing were too close together. Supervisory review existed on paper, but not in practice. Once transaction details, approvals, and job costing were lined up side by side, the owner could finally see where the process was failing.

The lesson was simple. If payroll, job costing, and reconciliation don’t talk to each other, money leaks.

Healthcare practice with billing questions

A small clinic started asking questions because collections and scheduling weren’t moving in sync. The providers were busy, but the numbers felt uneven. Staff had explanations. None of them held together for long.

The deeper review focused on billing patterns, adjustments, and account activity over time. That kind of work matters because healthcare businesses often have multiple systems touching the same dollar before it lands in the bank. If nobody is reconciling those systems with discipline, a bad actor or a bad process can hide in the gap.

In that case, the owner didn’t just need better reports. The owner needed reports that could be trusted.

Non-profit with restricted fund confusion

A non-profit board noticed growing discomfort around how certain expenses were being described. The issue wasn’t dramatic at first. It was inconsistency. One month a charge was administrative. Another month it looked program-related. Then reimbursements started raising eyebrows.

Once a forensic-style review starts, the question isn’t “Does this feel wrong?” It becomes “What do the supporting records show, and does the flow of funds match the stated purpose?” That standard is especially important in organizations that answer to donors, grantors, and boards.

The common thread

None of these situations began with a confession.

They began with mismatch. A mismatch between activity and reporting. Between explanation and evidence. Between trust and documentation.

That’s why I tell owners not to wait for certainty. If the books are giving you a headache, that’s enough reason to bring in experienced eyes.

Your Next Steps to Financial Security

You do not need a courtroom-sized disaster to act. If you run a Jacksonville construction company, medical practice, or non-profit, a small control problem can turn into a very expensive one fast. The smart move is to tighten the system before you are forced into a full fraud investigation.

Start with protection.

Do these three things first

Lock down the records

Preserve your accounting file, bank activity, payroll reports, invoices, receipts, vendor records, and relevant email threads. Freeze deletion rights if needed. If someone starts editing history after questions come up, your cleanup cost goes up and your answers get weaker.Separate duties now

Review who can set up vendors, approve payments, post journal entries, run payroll, and reconcile accounts. One person should not control an entire money trail. In small businesses, that setup is common. It is also how fraud and sloppy reporting hide in plain sight.Bring in an outside reviewer

Internal conversations rarely fix internal blind spots. An independent CPA or fractional CFO can test transactions, trace cash movement, and spot control gaps without office politics getting in the way.

Stop treating fraud prevention like a luxury

For small and midsize businesses in Northeast Florida, prevention costs less than cleanup. A few hours of control testing, monthly review, and better reporting can stop the kind of mess that leads to tax problems, lender questions, board conflict, or a long forensic review later.

That matters even more in industries with moving parts. Construction companies deal with job costing, change orders, draws, and subcontractor payments. Healthcare groups deal with billing adjustments, insurance timing, and payroll complexity. Non-profits have donor restrictions, reimbursement rules, and board oversight. If the reporting is weak, the risk is high.

Use better methods, not more guessing

A professional review goes beyond scanning the profit and loss statement and asking whether something looks odd. It includes transaction testing, account reconciliation, access review, trend comparison, and pattern analysis across large volumes of entries.

That work functions like a pressure test on your financial system. It shows where money can slip out, where documentation breaks down, and where one employee has too much control.

Build a finance function that catches problems early

If your books depend on one overworked staff member, memory-based processes, or reports you do not fully trust, fix that now. Waiting usually makes the repair more expensive.

What works for Jacksonville area SMBs is straightforward. Clean bookkeeping. Timely reconciliations. Clear approval rules. Regular compliance review. Senior financial oversight without the cost of a full-time CFO.

That is where fractional CFO and compliance support earn their keep. They help owners make fraud harder, errors easier to catch, and reporting easier to trust.

If your numbers do not add up, your controls feel loose, or you need senior guidance without hiring a full-time finance executive, talk with Bookkeeping and Accounting of Florida Inc.. The firm supports Jacksonville and Northeast Florida businesses with bookkeeping, tax preparation, internal audits, forensic audits, and fractional CFO services so owners can stay compliant, understand their numbers, and make decisions with confidence.