Your business had a good year. Revenue climbed, clients paid, payroll went out, and you finally felt like the thing was working. Then tax time hit, and instead of a manageable balance due, you got a federal bill that punched your cash flow in the throat.

That's how a lot of Northeast Florida owners learn about estimated quarterly tax payments. Not from a neat checklist. From pain.

In Jacksonville, I see the same movie over and over. A contractor, clinic owner, retailer, consultant, or nonprofit leader focuses on running operations. They assume they'll “settle up” at filing time. The IRS doesn't work that way. Federal taxes run on a pay-as-you-go system, and if you wait too long, the bill gets uglier than it needed to be.

The Tax Surprise You Never Want

A business owner in Northeast Florida has a record year. They hire help, buy equipment, and take draws because the bank balance looks healthy. April rolls around and the return says they owe far more than expected, plus penalties for not paying along the way. That's not bad luck. That's a broken system inside the business.

Estimated quarterly tax payments aren't some weird side rule for the ultra-wealthy or the unusually organized. They're part of the normal federal tax system for people whose income isn't fully covered by paycheck withholding. If you own a business, earn pass-through income, or bring in money outside a standard W-2 setup, you need to pay attention.

Why this catches business owners off guard

Most owners watch the checking account, not tax exposure. Those are not the same thing.

A strong month in your business can create a tax obligation long before you file a return. If you treat every extra dollar like spendable cash, you'll eventually end up financing the IRS with panic. That's a rotten way to run a company.

Practical rule: If your income rises and nobody is actively updating your tax projection, you are guessing. Guessing is not tax planning.

Attorney guidance can help frame how serious this is. Stephen Weisberg on estimated taxes makes the point clearly. Skipping these payments isn't a harmless delay. It can turn into penalties and a nasty surprise.

If you want a plain-English read on the topic, this piece on quarterly taxes and how to prepare for them is worth your time.

What smart owners do instead

They build a system. They don't wait for April to tell them what happened. They forecast, set money aside, and adjust as the year unfolds.

That's the professional approach. It protects cash flow, keeps you compliant, and lets you make decisions based on reality instead of hope.

What Are Estimated Taxes and Who Must Pay

Estimated taxes are installment payments toward federal tax liability on income that doesn't have enough withholding attached to it. Think business profit, pass-through income, side income, investment income, or any other income stream where the government isn't skimming enough off the top during the year.

The IRS doesn't care whether you meant well. It cares whether enough tax was paid in on time.

Who usually has to deal with this

The rule is tied to underpayment risk, not to whether you call yourself a “small business.” According to the IRS, individuals, including sole proprietors, partners, and S corporation shareholders, generally must make estimated quarterly tax payments if they expect to owe $1,000 or more when the return is filed, while corporations generally use a $500 threshold. The IRS also frames the calculation around expected adjusted gross income, taxable income, deductions, and credits, as explained on the IRS estimated taxes page for small businesses and self-employed taxpayers.

That means these businesses commonly get pulled into the estimated tax world:

- Sole proprietors who report business profit on their personal return

- Partners who receive pass-through income from a partnership

- S corporation shareholders whose owner income isn't fully covered by payroll withholding

- C corporations that have their own estimated income tax obligation

- Owners with multiple income streams who assume one paycheck will somehow cover everything

Why Florida owners still need to care

Florida doesn't have a state personal income tax. That's nice. It also fools some owners into thinking taxes are simpler than they are.

They aren't.

Federal compliance still applies, and for many Jacksonville businesses, federal estimated quarterly tax payments are the main tax rhythm that drives cash planning during the year. If you run a medical practice in Southside, a trade business in Orange Park, a retail operation near the Beaches, or a service company anywhere in Northeast Florida, this rule set can land squarely on your desk.

You don't get a pass because your business is local, small, new, or busy.

The mistake I see most

Owners confuse filing with paying. Filing happens later. Payment responsibility starts as income is earned.

That distinction matters. A lot.

If your business throws off profit and nobody is checking whether taxes are being prepaid, you're not saving time. You're just delaying the mess.

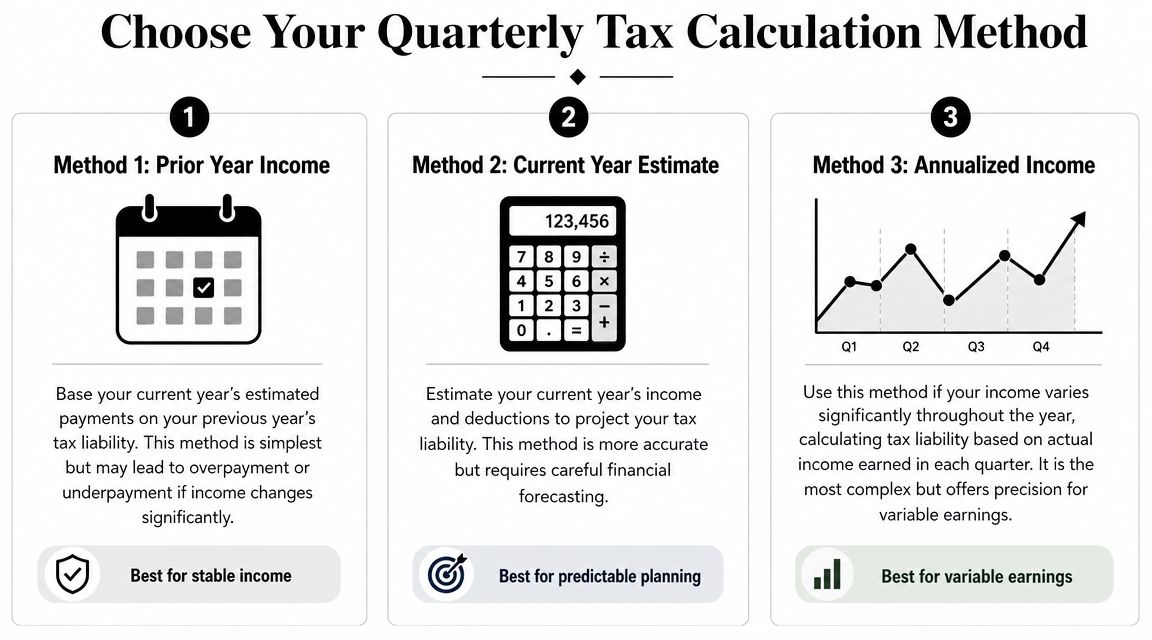

How to Calculate Your Quarterly Payments

There's more than one way to calculate estimated quarterly tax payments. That's useful, but it also creates trouble. Business owners pick the wrong method, use stale numbers, or choose the easy path when the business has changed too much for “easy” to be safe.

The tax year is split into four payment periods, and common safe-harbor approaches include paying 90% of the current year's expected tax or basing installments on prior-year tax. For the prior-year safe harbor, the target is 100% of last year's tax, rising to 110% for higher-income taxpayers, and businesses with seasonal revenue should consider annualized-income methods so payments align with actual earnings, as outlined in Chase's guide to managing and paying quarterly taxes.

Method one uses prior-year tax

This is the blunt instrument. It works best when your income is fairly stable and last year is still a decent proxy for this year.

You look at last year's tax, use that as the benchmark, and spread the required amount across the year. It's simple. It's predictable. It's also not always efficient.

This method often makes sense for owners who want a cleaner compliance path and don't want to rebuild a full tax model every quarter.

Method two uses a current-year projection

This is the grown-up method for a business that's changing. If your revenue is up, margins moved, payroll changed, or deductions look different, a fresh projection usually gives you a better answer.

You estimate current income, factor in deductions and credits, and calculate payments based on what the year appears to be becoming, not what it used to be.

That sounds straightforward until reality shows up. Current-year projection only works if your books are current and your forecasting isn't nonsense. If your bookkeeping is behind, this method turns into educated fiction.

Here's a good litmus test:

- Stable company. Prior-year approach may be fine.

- Fast-growing company. Current-year projection is usually more realistic.

- Messy books. Neither method will save you until the records are fixed.

A visual comparison helps make the choices clearer:

Method three annualizes income

This is the method seasonal businesses should stop ignoring. In Florida, plenty of companies don't earn evenly. Construction firms, tourism-linked operations, specialty retail, and project-based service businesses can have lumpy income.

If you make the same payment every period while your income swings around, you can end up paying too much too early or too little when the IRS expects more. Annualizing income lines payments up with what the business earned during each period.

If your revenue comes in waves, your tax method should too.

My recommendation

Don't choose a method because it sounds convenient. Choose the one that fits the economics of your business.

And if nobody inside your company can produce a timely profit and loss statement, cash forecast, and tax projection, then you don't just need bookkeeping. You need higher-level financial guidance. A fractional CFO earns their keep by providing it. They help decide which method fits, monitor whether the estimate still holds, and keep taxes from wrecking your working capital.

A lot of owners think that's overkill. It isn't. Flying blind is overkill.

The 2026 Payment Schedule and Filing Methods

The payment schedule trips people up because it looks quarterly, but it doesn't line up neatly with calendar quarters. If you assume “every three months” and move on, you're asking for trouble.

For 2026, widely cited due dates are April 15, June 15, and September 15, with the final installment due in January 2027, and businesses and individuals who expect to owe more than $1,000 typically use Form 1040-ES for calculations and payments, according to the U.S. Chamber's overview of estimated tax payments and 2026 due dates.

2026 Federal estimated tax payment deadlines

| Payment Period | Due Date |

|---|---|

| First payment period | April 15, 2026 |

| Second payment period | June 15, 2026 |

| Third payment period | September 15, 2026 |

| Fourth payment period | January 2027 |

How to file and pay

You've got a few ways to make the payment, but the practical advice is simple. Use an electronic method whenever possible. It's faster, cleaner, and easier to track.

Common approaches include:

- Electronic IRS payment options for direct submission and better recordkeeping

- EFTPS if you want a structured federal payment process

- Form 1040-ES if you're calculating and documenting individual estimated payments

- Paper voucher by mail if you insist on doing things the hard way

My advice on process

Don't rely on memory. Put each due date on the company calendar and the owner's calendar. Then tie those dates to an internal review a bit earlier so somebody checks year-to-date profit, distributions, withholding, and cash reserves before money moves.

Late payment problems usually start as calendar problems, then turn into tax problems.

Also, keep proof. If the payment went out electronically, save the confirmation. If your staff handles it, make sure the documentation lands in a place your tax preparer can find later. Year-end cleanup costs more when the records are sloppy.

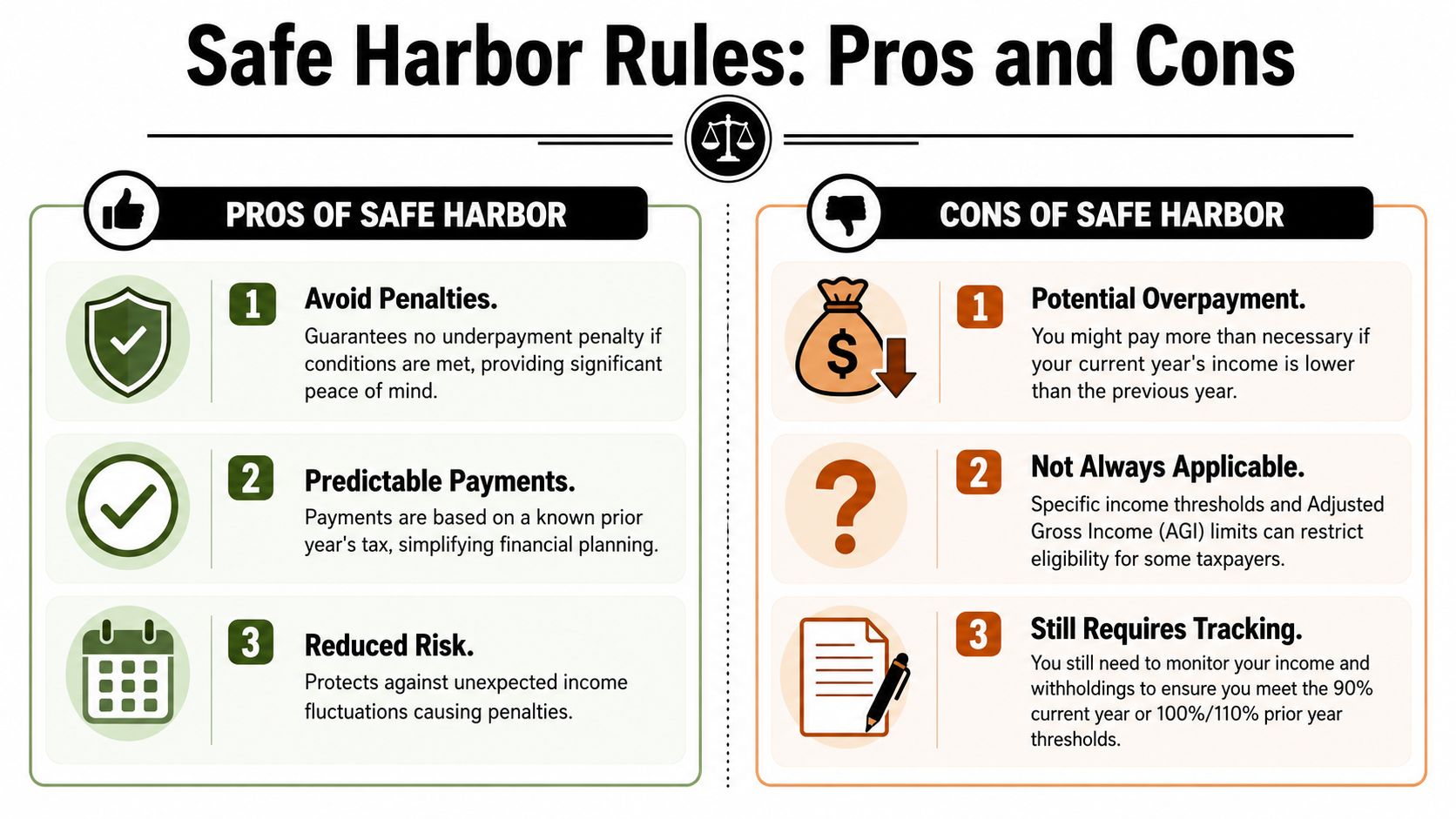

Avoiding Penalties with Safe Harbor Rules

Underpayment penalties are the IRS way of saying, “You should have paid us earlier.” They don't care that your equipment broke, a client paid late, or you meant to deal with it after busy season. If the required amount wasn't paid during the year, the penalty conversation starts.

The best defense is understanding safe harbor rules and using them on purpose.

The two main safe harbor lanes

The IRS says individuals generally must make estimated payments when withholding will cover less than 90% of the current year's liability or 100% of the prior year's liability. That prior-year safe harbor rises to 110% if adjusted gross income exceeded $150,000, and for many taxpayers, W-2 withholding adjustments can be used to meet these targets without making separate quarterly payments, as summarized by Fidelity's article on estimated tax payments and safe harbor rules.

Those rules create two practical lanes:

- Current-year lane if you have a solid tax projection and want payments to match this year's actual tax picture

- Prior-year lane if you want a more predictable benchmark and a simpler compliance path

The right choice depends on your income pattern, your records, and how much uncertainty you can tolerate.

The strategy many owners miss

Owners who also receive W-2 wages sometimes have another lever. They can adjust withholding.

That matters because withholding can help satisfy the safe harbor test. In plain English, a business owner with salary income, a spouse with wages, or another withholding source may be able to reduce or even eliminate separate estimated quarterly tax payments if withholding is coordinated correctly.

A lot of online tax content ignores that. Good planning doesn't.

If you want to sharpen that side of your tax strategy, this guide on business tax planning strategies is a useful next read.

What I recommend in practice

If your income is volatile, don't flirt with the line. Use a disciplined estimate and revisit it during the year.

If your income is stable and you value predictability, the prior-year safe harbor often gives you cleaner execution.

If you have payroll, don't overlook withholding adjustments. They can be simpler than sending separate payments all year and can help clean up a shortfall before year-end.

The safest tax move is rarely the fanciest one. It's the one you'll actually execute on time, with records to prove it.

Bookkeeping Best Practices for Accurate Payments

You can't calculate good estimated quarterly tax payments from bad books. That's not opinion. That's mechanics.

If your QuickBooks file is behind, bank feeds are uncategorized, owner distributions are mixed in with operating expenses, and payroll isn't tied out, your tax estimate is just a dressed-up guess. Business owners hate hearing that, but it's true.

The QuickBooks workflow that actually helps

Start with current books. Run a year-to-date Profit & Loss in QuickBooks. Compare it to the prior period. Look at owner draws, payroll, unusual expenses, and any major swings in revenue.

Then ask the questions that matter:

- Has profit changed materially from what you expected?

- Did the owner take draws that affect cash planning, even if they don't change taxable profit the same way?

- Is payroll withholding doing enough to support the overall tax plan?

- Are there one-time transactions that distort the picture?

This is also where many owners miss the coordination issue. As discussed by The Tax Adviser in its article on minimizing estimated tax payments through withholding coordination, many business owners don't know how to align payroll withholding, owner draws, or spouse income with safe-harbor targets.

Don't book estimated taxes as a business expense

This one causes a mess every year.

For many pass-through owners, federal estimated tax payments are not a deductible business expense on the company books. They're generally treated as an owner draw or equity distribution. If you book them as tax expense in QuickBooks, your financial statements get distorted and your reports start lying to you.

That's how owners think the business is less profitable than it really is. Then they make bad decisions based on bad numbers.

If your chart of accounts needs cleanup, this guide on setting up a chart of accounts in QuickBooks is a solid place to start.

Clean systems beat heroic catch-up

Certified QuickBooks ProAdvisors earn their value in the boring parts. Proper account mapping. Timely reconciliations. Consistent coding. Clear owner equity entries. Those things don't sound exciting, but they make accurate tax planning possible.

And yes, operational systems matter too. If your front office is swamped, missed calls and scattered admin work can create downstream bookkeeping delays. The overview of AI reception for accounting firms is an interesting look at how firms are using technology to keep communication and workflows from falling apart.

Good estimated tax planning starts with clean books. Not vibes. Not bank balance logic. Books.

Move from Tax Stress to Strategic Growth

Estimated quarterly tax payments aren't the underlying problem. They're the symptom.

The deeper issue is that many small businesses are operating without enough financial leadership. They have a tax preparer once a year, maybe a bookkeeper trying to keep up, and nobody watching the full picture. Cash flow, profitability, compliance, owner compensation, and tax strategy all get handled in fragments. That's how surprises happen.

Why guidance matters

A strong business doesn't just record history. It uses financial information to make decisions while there's still time to change the outcome.

That's why I'm opinionated about this. Most growing companies need more than basic bookkeeping. They need someone who can connect the books to tax planning and connect tax planning to operations. In other words, they need fractional CFO-level guidance, whether they call it that or not.

The better way to run it

When your financial systems are working, estimated taxes stop being a recurring panic attack. Deadlines get met. Cash gets reserved. Withholding gets coordinated where appropriate. QuickBooks reflects reality. The owner knows what can be spent, what must be saved, and what decisions need attention before they become expensive.

That's not luxury accounting. That's competent business management.

If you run a business in Jacksonville or anywhere in Northeast Florida, stop treating tax compliance like an annual emergency. Put a system in place and get people around you who know what they're doing.

If you want help turning messy books, surprise tax bills, and deadline stress into a clean financial system, talk with Bookkeeping and Accounting of Florida Inc.. Their Jacksonville team handles bookkeeping, tax preparation, payroll, audits, and fractional CFO support for Northeast Florida businesses that want accurate numbers, better compliance, and less chaos.