At its core, "bank reconciliation" is just a fancy way of saying you’re matching your company’s books to your bank statement. It’s a financial health check-up where you compare every single transaction—deposits, withdrawals, pesky bank fees, and interest earned—to make sure both records are singing the same tune. The goal is to hunt down and fix any differences so you have a true picture of your cash. Learning how to reconcile bank accounts is a fundamental skill for every business owner, but it's also a process that highlights the critical need for professional financial oversight.

Why Bank Reconciliation Is a Must-Do for Florida Businesses

Bank reconciliation is so much more than just a bookkeeping chore. Think of it as a critical control for protecting your business’s financial health. For Florida businesses trying to navigate complex state tax laws, federal tax law changes, and a fast-moving economy, knowing exactly what's happening with your cash is non-negotiable. It’s the bedrock of smart decisions, fraud detection, and staying compliant.

This process became a standard practice because cash is one of the easiest assets to get wrong on the books. A solid reconciliation confirms that the money you think you have is what's actually sitting in your account. The logic is simple but incredibly powerful: after you account for things like uncleared checks or bank fees, your book balance and bank balance should match perfectly, leaving you with a $0 unreconciled amount. You can dig deeper into this foundational process at Numeric.io.

Staying Compliant and Profitable in an Era of Change

Most small business owners don't have the time to track every tiny change in tax laws and financial rules. This is where so many fall behind, leading to painful penalties and missed opportunities. Most small businesses simply do not know what is required to stay compliant. Without accurate financials—which you can't have without regular reconciliations—you're basically flying blind.

Our business accounting services solve this problem. We provide the expert guidance needed to keep your company compliant and your financial data accurate, so you can focus on growth instead of paperwork.

Every company, no matter its size, needs a financial guide. We act as your fractional CFO—a strategic partner who is genuinely dedicated to your success. We help you make sense of your numbers, manage your cash flow, and make decisions with confidence. We make sure you stay compliant because we know what’s required, even when you don’t. This isn't a luxury; it's essential for survival and profitability.

Gathering Your Financials for a Smooth Reconciliation

A solid bank reconciliation doesn't start when you sit down to match transactions. No, the real work begins before you even glance at your bank statement. Getting organized first is the secret to turning this monthly chore from a migraine-inducing nightmare into a quick, satisfying check-up.

Learning how to reconcile bank accounts is all about having the right documents ready to go. If you’re staring at a stack of paper statements, your first move should be to digitize them. You might need to convert bank statement PDFs to CSV to get them into your accounting software without wanting to pull your hair out from all the manual entry.

Before we dive into the nitty-gritty, let's get a few things straight. These aren't "mistakes" in your books; they're just the messy reality of how money moves.

Understanding Timing Differences

The biggest reason your books and your bank account never seem to agree is timing. Here are the two main culprits:

- Outstanding Checks: You wrote a check to a vendor, recorded it, and mailed it. But that vendor is using it as a bookmark and hasn't cashed it yet. Your books show the money is gone, but the bank doesn't know that yet.

- Deposits in Transit: You deposited a customer's check on the 31st. You recorded the payment (go you!), but the bank is still processing it. It's your money, but it hasn't officially landed in your account according to the statement.

These timing issues are completely normal, but they’re also why keeping clean records is non-negotiable. If your receipt system is a disaster, this whole process falls apart. Our guide on how to organize receipts for taxes has tips that will save your sanity here, too.

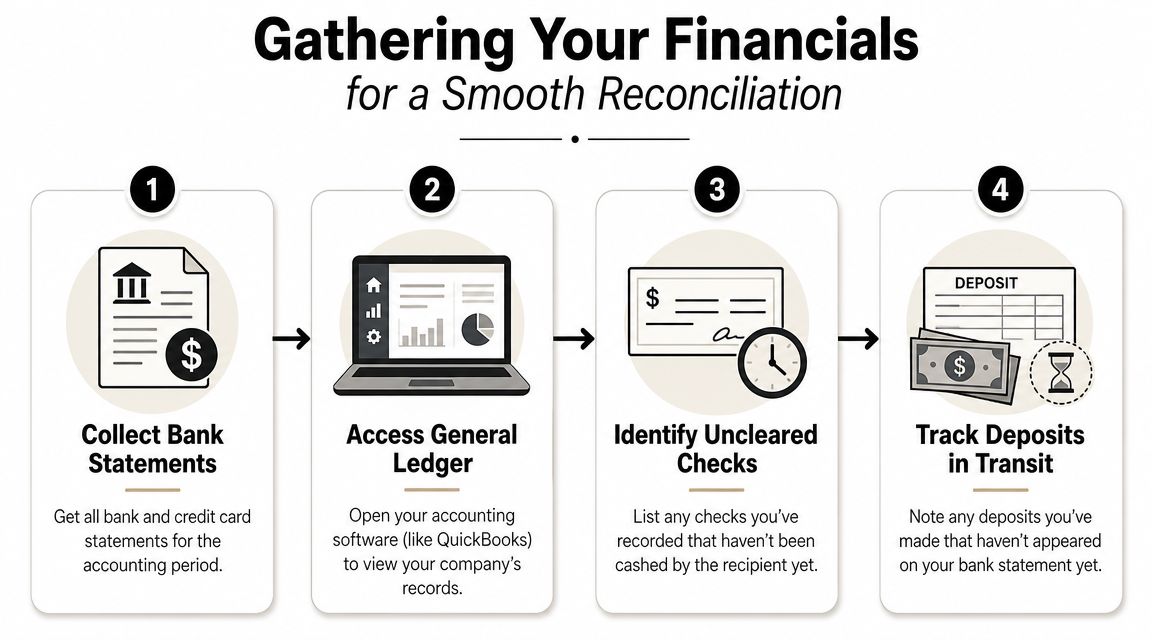

To get started, you'll need to gather a few key documents. Think of it as your pre-reconciliation toolkit—having everything on hand makes the process much smoother.

Your Bank Reconciliation Toolkit

| Item | Description | Why You Need It |

|---|---|---|

| Bank Statements | Official monthly statements for all business bank and credit card accounts. | This is the bank's version of the story. It shows every transaction that has cleared. |

| General Ledger | Your business's record of all transactions for the same period. | This is your version of the story. You'll compare this against the bank statement. |

| Previous Reconciliation Report | The report from the prior month's reconciliation. | This report lists any outstanding items from last month that should have cleared this month. |

| Check Register | A list of all checks written from your business account. | Helps you quickly identify which checks have cleared and which are still outstanding. |

| Deposit Slips & Records | Records of all cash and check deposits you made. | Essential for spotting any deposits in transit that haven't shown up on the bank statement yet. |

With these items in hand, you're ready to tackle the reconciliation process without getting sidetracked searching for missing information.

Most business owners are experts in their field, not in financial compliance. And that's okay. From tax law changes to obscure federal reports, there's a lot to track. We know what's required, and we protect our clients from expensive penalties that come from simply not knowing.

When we handle your books, we're more than just number-crunchers. We act as your fractional CFO, giving you the strategic financial guidance that every business needs but few can afford full-time. We worry about changing tax laws so you can get back to running your business.

How to Actually Reconcile Your Bank Accounts

Alright, you've got your documents. Now for the main event: learning how to reconcile bank accounts. Forget what you think you know about rigid accounting steps; this is really just a matching game.

Your job is to go line by line, comparing every single transaction on your bank statement to the entries in your accounting software. When you find a perfect match, check it off. Done.

Anything that doesn't match—a surprise bank fee, a check a vendor hasn't cashed yet, or a dreaded duplicate charge—gets its own special list. Don't panic. This list of discrepancies isn't a sign you messed up. It's the entire point of doing this in the first place.

Matching Your Deposits and Payments

Start with the money coming in. Look at each deposit on your bank statement and hunt down its partner in your general ledger. For instance, if the bank shows a $1,500 deposit on the 15th, find the sales receipt or invoice payment in your books for that exact amount and date. Once they match up, check them both off your list.

Now, do the same thing for all the money going out—withdrawals, checks, and debit card swipes. That $250 payment to your office supplier? It needs to show up in both places. Stick to a monthly cycle for this. The longer you let an item sit unreconciled, the more of a headache it becomes to figure out where it came from. The FDIC has tons of data on banking cycles if you want to geek out, but a month is the gold standard for a reason.

This image shows you exactly what documents you need to have handy before you even start this matching game.

As you can see, having your statements, ledger, and a running list of uncleared items ready makes this whole process less of a puzzle and more of a simple verification task.

Pinpointing Discrepancies and Staying Compliant

Those items left unchecked on your list? Those are your discrepancies. This is where most business owners throw their hands up. It’s not that they can’t find the problems; it’s that they have no idea how to fix them or what they mean for tax compliance.

If that sounds familiar, it's a blaring signal that it's time to bring in professional business accounting help.

Staying compliant is a full-time job. With tax law changes constantly impacting businesses, you need someone in your corner who actually understands the rulebook. Every company needs a guide to make sure they're protected from costly mistakes and penalties.

Think of us as your fractional CFO. We don't just fix the reconciliation errors you have now; we build the systems to stop them from happening again. Most small businesses don't know what's required of them to stay compliant, and that's okay. Let us handle the financial chaos so you can get back to what you do best—running your business.

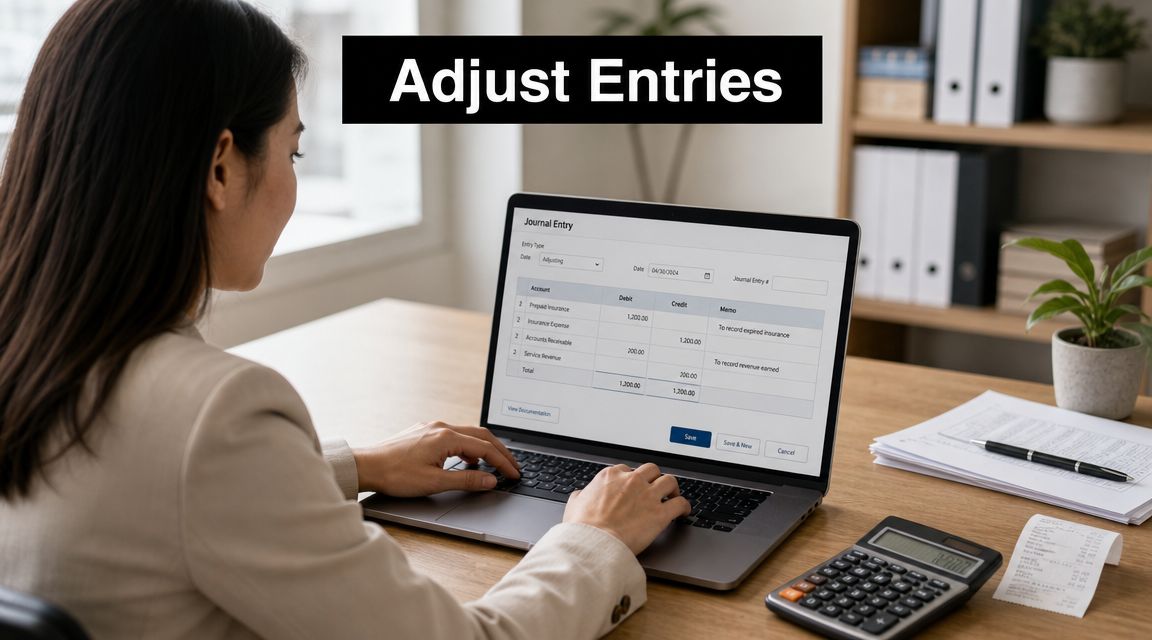

Fixing Discrepancies and Making Adjusting Entries

So, you've compared your books to the bank statement, and—surprise!—they don't match. This is where the real work of learning how to reconcile bank accounts begins. Finding the differences is just the first step; fixing them with adjusting journal entries is what actually makes your financials trustworthy again.

You’ll almost always find things like unrecorded bank fees, a little bit of surprise interest income, or maybe a customer's check that bounced. For example, that $25 monthly service fee the bank charged you? If it's not in your books, you need to create a journal entry to account for it. It's a simple fix: debit "Bank Service Charges" and credit your "Cash" account. Done. Your books are now a little closer to reality.

Why You Can't Afford to Go It Alone

This process shines a spotlight on a major risk for small businesses. Most owners are experts in their trade, not in keeping up with ever-changing tax law changes or confusing compliance rules. A missed entry is one thing. Failing to file a required report you didn't even know existed can bring on penalties that cripple your business.

This is exactly why you need a financial guide. As experts point out, bank reconciliation is more than a monthly chore—it's a critical internal control that should involve an independent review to catch errors and prevent fraud. You can learn more about how it prevents costly mistakes on SOG.UNC.edu.

Your expertise is running your business, not deciphering IRS code. We act as your fractional CFO, providing the high-level financial guidance you need to navigate compliance and make smart decisions.

Our business accounting services are built to take this weight off your shoulders. We manage the mess of financial compliance because it’s our job to know what’s required, even when you don’t. By making sure your books are consistently accurate, we give you the solid foundation you need to stay compliant and get back to focusing on growth. If you’re stuck here, our article on the ugly truth about unreconciled accounts can shed more light on the problem.

Beyond Reconciliation: Why Your Business Needs a Financial Guide

Learning how to reconcile bank accounts is a fantastic start. Seriously. But it’s just the first mile in a marathon.

True financial control isn't just about making numbers match. Especially for a Florida business owner, you're juggling shifting tax law changes, confusing local regulations, and the constant pressure to actually grow the business. It's a lot.

Most business owners hit a wall where they realize they can't—and absolutely shouldn't—do it all. Your genius is in running your company, not becoming a part-time tax law professor. And frankly, this is where businesses get into hot water. They just don't know what they don't know, and ignorance of compliance requirements is not a defense.

From Bookkeeping to Real Guidance

This is where we step in. We go way beyond basic bookkeeping to give you the strategic guidance you actually need. Think of us as the financial co-pilot who can read the map and see the storm clouds ahead.

Every company needs a fractional CFO to guide the ship. We provide that high-level expertise—making sure you’re compliant and profitable—without you having to pay a six-figure executive salary.

Our job is to keep you compliant because we know what’s required, even when you don’t. A great starting point for any business owner is understanding the basics of preventing compliance issues for SMBs. Partnering with us means you have an expert in your corner, protecting you from expensive penalties that pop up from simply not knowing the rules.

Your Partner in Growth (Not Just Paperwork)

Don't let financial management become the anchor dragging your business down. We handle the headaches of tax law changes and compliance so you can get back to what you do best: running your company.

We offer more than balanced books—we provide peace of mind. To see how this high-level partnership works, check out our guide on what fractional CFO services can do for you.

Let us handle the numbers. You go lead your company with confidence.

Common Bank Reconciliation Questions Answered

You’ve followed all the steps, but your books and the bank statement are still giving each other the silent treatment. Sound familiar? Knowing how to reconcile bank accounts is one thing; playing detective when things don't add up is another.

Let's cut through the confusion. Here are the most common questions and sticking points we see business owners get tangled up in.

How Do Changing Tax Laws Affect Reconciliation?

This is a big one. While a tax law change won't rewrite the basic steps of matching transactions, it raises the stakes from "good housekeeping" to "absolutely critical."

Think about it: a new tax credit, a different way to deduct expenses, or new reporting rules mean your bookkeeping categories have to be flawless. A sloppy reconciliation leads to misclassified transactions. That could mean missing a huge deduction or, even worse, filing your taxes incorrectly and inviting an IRS audit. Suddenly, accurate books aren't just a nice-to-have—they're your first line of defense against compliance nightmares.

What If I Still Can't Find the Discrepancy?

You've hunted for transposed numbers. You’ve scoured for duplicate entries. You’re still off by some stubborn, infuriating amount. This is a classic frustration and a sign that it’s time to tag in a professional.

Before you lose another evening to this one error, think about what your time is worth.

Every business hits a point where DIY accounting costs more in lost time and potential mistakes than getting professional help. Your time is better spent growing your business, not hunting down a $47 discrepancy for three hours.

This is exactly why businesses bring our firm in. Our business accounting services are built to solve these headaches efficiently. We know all the weird places errors hide, and we can fix them fast, so you can get back to doing what you actually love.

Why Do I Need a Fractional CFO?

Most small business owners are experts in their field—plumbing, marketing, software development—not in financial strategy and compliance. That's a huge gap. All companies need a fractional CFO and someone to guide their business.

A fractional CFO fills that gap by providing the high-level financial guidance every growing company needs, but without the six-figure salary of a full-time executive. We're not just balancing the books; we're your strategic partner. We help you make smarter financial decisions, stay compliant with laws you didn't even know existed, and build a more resilient, profitable company. You need us to help you stay compliant since most small businesses do not know what all is required.

Don't let financial chaos hold your business back. The team at Bookkeeping and Accounting of Florida Inc. is here to bring clarity to your numbers so you can focus on your vision. Contact us today for a consultation and let us handle the spreadsheets.