Your phone buzzes. A vendor wants payment. A customer says they already paid. Your bank balance looks decent, but payroll hits tomorrow and sales tax is lurking in the shadows like a raccoon near a dumpster.

That's how most small business owners live. Not because they're lazy. Because they're busy, and the books become a cleanup project instead of a daily control system.

That's a mistake.

If your bookkeeping happens when you “get a minute,” you don't have a bookkeeping system. You have financial leftovers. And leftovers go bad fast. Good bookkeeping by day gives you clean numbers, faster decisions, smoother tax prep, and fewer ugly surprises. It also tells you when you need more than bookkeeping. You need a CPA. You need advisory. In many cases, you need a fractional CFO.

Why Your Business Runs on "Bookkeeping by Day"

The shoebox method is alive and well. Receipts in a drawer. Bank feeds half-reviewed. Personal charges mixed with office supplies. Then month-end shows up, and everyone acts shocked that the numbers don't make sense.

That's not bookkeeping. That's archaeology.

Daily records are older than most business advice

Bookkeeping isn't some modern admin chore invented by software companies. Bookkeeping's roots stretch back to ancient Mesopotamia, where accounting records on clay tablets date to more than 7,000 years ago, around 3300 BC, and those records tracked livestock, crops, goods, debts, and inventory as practical business controls for real economic activity, according to this history of accounting.

That matters for one simple reason. The basic job hasn't changed. Record what happened. Record it accurately. Record it while it's still fresh. That's how merchants kept control then, and that's how business owners keep control now.

A contractor in Jacksonville doesn't need clay tablets. But he does need to know whether yesterday's deposit cleared, whether the fuel charges were coded right, and whether that “small” supply run was a personal purchase slipped onto the business card.

Daily clarity beats monthly panic

When you handle bookkeeping by day, you stop guessing. You know what came in. You know what went out. You know which customers are slow-pay and which vendors need attention. You also catch problems while they're still fixable.

Practical rule: If you wait until month-end to understand your cash position, you're already late.

A daily routine also forces discipline around documents. If your receipts, invoices, contracts, and approvals are scattered across email, text messages, and somebody's truck console, you're asking for trouble. If you want a practical read on organizing that side of the house, take a look at handling document compliance at Documind. Clean books depend on clean records.

Here's my opinion. Most owners don't need more hustle. They need better financial habits. Bookkeeping by day is the habit that keeps small problems small.

The Daily Financial Five Your Foundation for Accuracy

A solid daily routine isn't glamorous. Neither is brushing your teeth. Skip either one long enough and somebody's going to pay for it.

1. Record all income

If money came in today, it gets recorded today. Sales. deposits. online payments. checks. Everything.

Too many owners get sloppy at this stage. They see cash hit the bank and assume that's enough. It isn't. You still need to tie that deposit to the right customer, invoice, or revenue category. Otherwise, your reports are junk.

Back in 1494, Luca Pacioli published the first book documenting the double-entry bookkeeping system, using a day book, journal, and ledger to create a standardized control system for detecting errors and producing trustworthy financial statements that still underpins accounting today, as explained in this summary of Pacioli's framework. In plain English, every transaction needs a proper home.

2. Track every expense

Expenses don't become legitimate because you vaguely remember them. They need to be posted, categorized, and supported.

A debit card swipe at the office supply store might belong in supplies, software, equipment, or owner draws depending on what was purchased. That distinction matters. If you lump everything into “miscellaneous,” you're telling me you've given up.

3. Digitize and categorize receipts

Paper fades. People lose things. Phones make this easier than ever, so there's no excuse.

Use receipt capture tools inside QuickBooks or your expense app. Match the receipt to the transaction while the purchase is still fresh in your mind. If you need a practical workflow for cleaning up imported statement data, these automation tips for bank statements can help reduce manual grunt work before reconciliation.

A receipt without a category is clutter. A transaction without backup is a future argument.

4. Update accounts payable and accounts receivable

Your vendors and customers don't care that you were busy. Bills still come due. Invoices still need to go out. Collections still need follow-up.

Use a short daily check:

- Review open invoices: Make sure work delivered got billed.

- Check unpaid bills: Don't let due dates sneak up on you.

- Flag old balances: Slow-paying customers rarely fix themselves.

- Confirm credits and partial payments: Small mismatches grow into big reconciliation headaches.

A business can look profitable on paper while running short on cash because receivables are stale and payables are unmanaged. That's how owners end up stressed, confused, and blaming the bank balance.

5. Monitor daily cash flow

This is not the same as glancing at your banking app. Daily cash flow means understanding what's available, what's committed, and what's about to hit.

Ask these every day:

- What cleared today

- What's pending

- What must be paid next

- What cash is free to use

If you don't know those answers, you're driving with a fogged-up windshield.

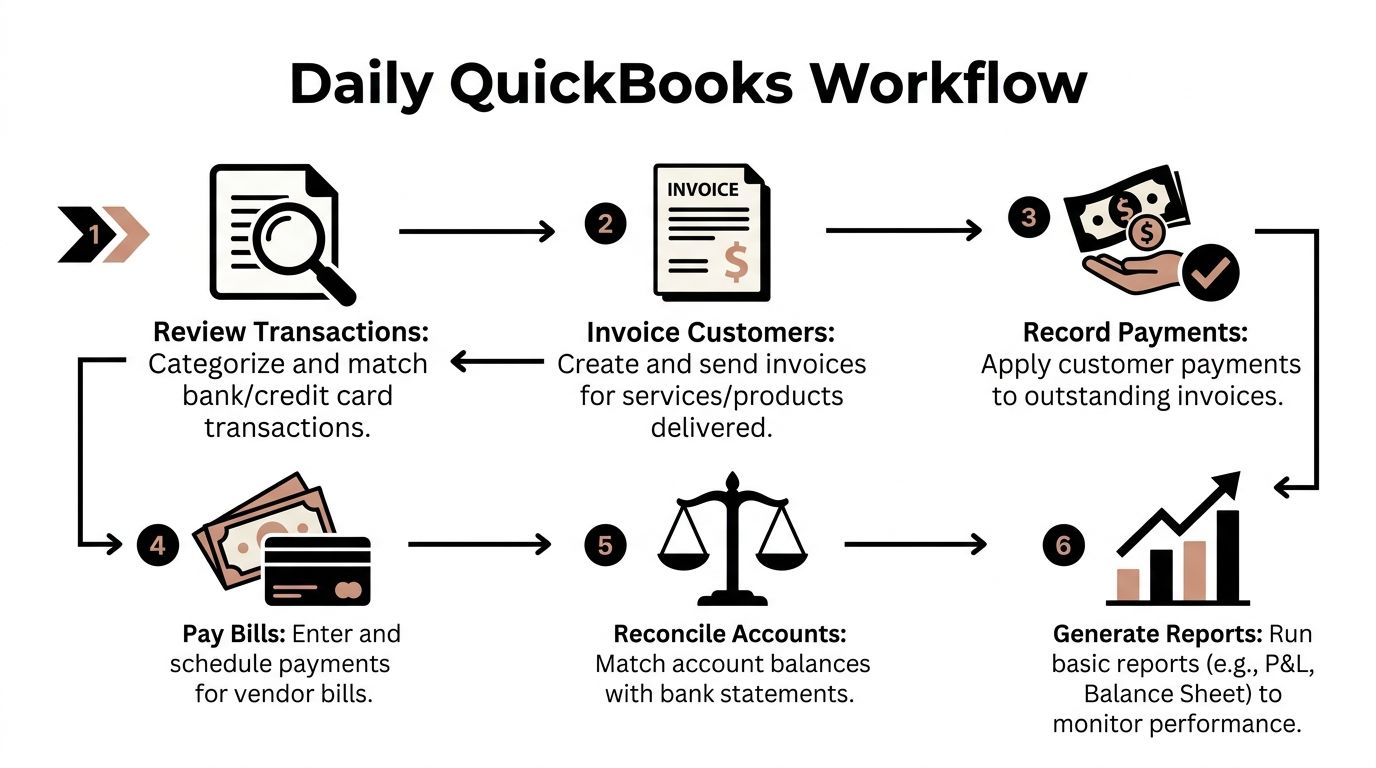

A Sample Daily Workflow in QuickBooks

QuickBooks can make daily bookkeeping easier. It can also make a mess faster if nobody's minding the store. Software is a tool, not a substitute for judgment.

Morning money check

Start the day with the bank feed and credit card feed. Review overnight activity. Look for anything odd. Duplicate charges. Customer payments that didn't match automatically. Transactions that hit the wrong account.

This is also the right time to confirm your chart of accounts isn't working against you. If your categories are messy, every daily task takes longer and produces worse reports. A clean setup matters, and this guide on how to set up a chart of accounts in QuickBooks lays out the structure clearly.

Use the morning review to answer one blunt question. Did money move in a way that makes sense?

Midday entry and cleanup

By midday, code uncategorized transactions while details are still fresh. Attach receipts. Enter vendor bills. Send customer invoices for completed work. Apply any payments that came in.

Don't overcomplicate it. The point is speed with accuracy.

A clean midday pass usually includes:

- Categorize bank feed items: Don't leave them sitting in limbo.

- Match receipts: Attach backup to the transaction immediately.

- Create invoices: Bill completed work before memory fades.

- Record bill entries: Keep payables current so cash planning stays honest.

If you're in retail, healthcare billing, construction, or another high-volume business, this daily rhythm isn't optional. It's how you keep control.

End-of-day close

The best operators don't stop at entry. They do a daily close.

To maintain a reliable daily workflow, experts recommend four controls: posting all transactions, reconciling cash and card feeds, scanning for data-quality issues, and tracking close KPIs such as time-to-close, reconciling items, and report accuracy, as described in this guide to the daily accounting close. The point is simple. Standardization reduces human error and supports same-day decision-making.

Daily close mindset: Post it. Reconcile it. Scan it. Move on with confidence.

That data-quality scan matters more than owners think. Wrong-account postings, duplicates, and missing fields turn a good-looking dashboard into fiction. We see it all the time.

One practical option for businesses that want help maintaining this kind of workflow is Bookkeeping and Accounting of Florida Inc., which provides bookkeeping, accounting, QuickBooks support, payroll, tax preparation, and fractional CFO services for growing companies. That kind of outside structure is useful when the owner no longer has time to babysit the books.

Owner vs Bookkeeper Who Should Do What

Owners love control. I get it. It's your company. But if you're spending your best hours fixing transaction categories and chasing missing receipts, you're doing technician work with owner-level time. That's expensive.

The owner should keep strategic control. The bookkeeper should handle tactical execution. Clean separation makes the business run better.

The split that works

| Financial Task | Owner's Role (Strategic) | Bookkeeper's Role (Tactical) |

|---|---|---|

| Approving large purchases | Decide whether the spend fits budget and priorities | Record the transaction correctly and attach support |

| Customer billing policies | Set payment terms and escalation rules | Issue invoices, apply payments, track aging |

| Vendor management | Approve key vendors and payment timing strategy | Enter bills, schedule routine payments, maintain records |

| Cash decisions | Review available cash and upcoming obligations | Update daily cash activity and reconciliation status |

| Financial review | Read reports and ask hard questions | Generate accurate reports from clean books |

| Budgeting | Set targets and spending limits | Track actual activity against those expectations |

| Compliance support | Respond to major tax, payroll, and legal decisions | Maintain documentation, coding, and reconciliations |

What owners should stop doing

Owners should not be the default dumping ground for receipts, coding, reconciliations, and cleanup. That's how backlogs happen. You miss entries. You approve bad assumptions. You end up reviewing reports that are wrong because the underlying work was rushed.

If you're trying to figure out what good delegation looks like, this overview on how to hire a bookkeeper is worth reading before you hand the books to your cousin, your office manager, or the last person who said, “I've used QuickBooks before.”

What a professional bookkeeper actually buys you

A real bookkeeper buys you consistency. That sounds boring until you've lived through inconsistent books. Then it sounds beautiful.

Here's the practical payoff:

- Cleaner reporting: You can trust the P&L and balance sheet enough to use them.

- Faster tax prep: Your CPA spends less time cleaning and more time advising.

- Better owner focus: You spend more time on pricing, staffing, and sales.

- Fewer compliance surprises: Missing support and sloppy classifications get caught earlier.

The owner should steer the ship. The bookkeeper should keep the engine room from catching fire.

That division is where smart businesses grow up. They stop treating bookkeeping like an afterthought and start treating it like infrastructure.

Common Pitfalls That Turn Profit into Problems

Some businesses don't fail because sales are weak. They fail because the books lied to them long enough to make bad decisions feel reasonable.

The ugliest bookkeeping problems are also the most common. The highest-risk daily bookkeeping failures are mixing personal and business transactions, misclassifying accounts, skipping documentation, and confusing profit with cash flow, and those mistakes distort liquidity analysis, tax readiness, and financial statement reliability while creating audit exposure and missed deductions, according to this breakdown of bookkeeping task risks.

Mixing personal and business is a mess, not a shortcut

Stop buying lunch for the family on the company card. Stop paying personal subscriptions from the business account. Stop pretending you'll “sort it out later.”

Later never comes clean.

When personal and business activity mix, every reconciliation takes longer. Every report gets fuzzier. Every tax conversation gets more annoying. You also increase the odds that something deductible gets missed and something non-business gets left in by mistake.

Misclassification warps the whole picture

A transaction in the wrong account doesn't just sit there. It changes the story your books tell.

Put equipment into office expense, and your expenses may spike while your asset records stay wrong. Dump loan proceeds into income, and your revenue report becomes fiction. Code payroll taxes incorrectly, and now payroll reporting may need cleanup too.

That's why the details matter. Not because accountants enjoy nitpicking. Because classification drives decision-making.

Profit is not cash

This one clobbers owners all the time. They see profit on the P&L and assume they can spend. Then the bank account says otherwise.

Here's a useful explainer to watch if this gap keeps tripping you up:

You can show a profit while cash is tied up in receivables, inventory, debt payments, or upcoming payroll. You can also have cash in the bank from a loan and still not be profitable. Those are not the same thing. Treating them as the same is how businesses get blindsided.

Tax compliance is where sloppiness gets expensive

Most small businesses don't fully understand what's required. Sales tax rules, payroll filings, owner compensation treatment, documentation standards, contractor issues, and year-end adjustments all have consequences. Tax law changes also keep moving the goalposts, which makes DIY bookkeeping even riskier.

Use this quick warning list as a gut check:

- Missing receipts: Weak support creates avoidable headaches.

- Late reconciliations: Old errors get harder to fix.

- Bad classifications: Reports become less useful for tax and management.

- No review process: Small errors stack up until month-end or year-end explodes.

If your bookkeeping by day routine doesn't include oversight, it's incomplete. Daily data entry is helpful. Professional review is what keeps it compliant.

When to Hire a CPA and Fractional CFO

A bookkeeper keeps the records clean. A CPA keeps you compliant and helps you deal with taxes, reporting, and the rules most owners don't know they're breaking. A fractional CFO helps you make smarter business decisions before a problem lands on your desk.

That's the ladder.

Hire a CPA when compliance starts getting real

If you have payroll, sales tax exposure, entity questions, growth plans, or multi-layered reporting needs, you need a CPA involved. Not once a year. Ongoing.

That's especially true when tax law changes affect filing positions, deductions, payroll treatment, or reporting methods. A lot of small businesses don't know what's required until they're already behind. That's not a good plan.

A CPA brings review, adjustment, and interpretation. They don't just file forms. They help keep the business compliant.

Hire a fractional CFO when decisions get bigger than bookkeeping

A major gap in the market is that many bookkeeping pages still don't explain how modern delivery models like AI-assisted categorization and remote collaboration reduce close times, lower error rates, and cut owner workload, which is exactly the issue highlighted in this discussion of bookkeeping by day content gaps. That gap matters because good financial support today should do more than record history. It should help owners act on it.

A fractional CFO steps into that gap.

They help with questions like:

- Can we afford to hire

- Which service line is making money

- Are we pricing correctly

- How much cash should we keep on hand

- Can we expand without choking cash flow

If you want a practical look at that role, review what fractional CFO services include. It's the bridge between bookkeeping and real financial leadership.

Good books tell you what happened. A fractional CFO helps you decide what to do next.

Every company doesn't need a full-time CFO. Most growing companies do need CFO-level thinking. That's why fractional support makes sense. You get guidance without full-time executive overhead, and you stop making major decisions based on hunches, stale reports, or whatever your bank app showed this morning.

If your books are behind, messy, or giving you more questions than answers, it's time to get help from Bookkeeping and Accounting of Florida Inc.. We help Northeast Florida businesses stay compliant, keep records clean, understand tax obligations, and get the kind of bookkeeping, CPA support, and fractional CFO guidance that turns daily numbers into better decisions.