You’re probably living this right now. The jobs are moving, crews are working, customers are calling, and money is flowing in and out fast enough to make your head spin. Then your banker asks for clean financials, your surety wants backup, or your tax preparer starts asking questions you can’t answer because your books are a pile of half-coded transactions, vendor bills, payroll reports, and hope.

That’s normal in construction. It’s also dangerous.

I’ve worked with enough contractors in Jacksonville to know the pattern. The owner can run a jobsite, manage subs, solve field problems, and close work. But if you can’t tell which jobs are making money, which customers are slow-paying, and whether payroll taxes and reporting are clean, you’re not running a business. You’re operating a very expensive guessing game.

Bookkeeping for construction companies isn’t regular bookkeeping with a hard hat on top. It’s project accounting, compliance control, cash flow management, tax planning, payroll discipline, and job-level profit analysis rolled into one. Get it right and you can grow with confidence. Get it wrong and the problems don’t stay small for long.

The High Stakes of Construction Bookkeeping

A lot of contractors think bookkeeping is back-office admin. It isn’t. It’s your profit engine, your compliance shield, and your early warning system.

If your books are messy, your bids are probably off. If your bids are off, your margins are fiction. If your margins are fiction, the “good year” you think you had can disappear the second someone cleans up your numbers properly.

That’s why I pay close attention to gross profit. According to the CFMA 2024 Construction Financial Benchmarker survey summarized by Kirsch CPA, the top 25% of construction companies achieved a gross profit margin of 21.8% of total revenue. That number matters because gross profit margin tells you what’s left after the direct costs of doing the work are accounted for.

Why this number should bother you

A contractor who doesn’t know their labor burden, materials usage, subcontractor exposure, and indirect job costs has no idea whether a project was profitable. They might feel busy. Busy is not the same as profitable.

Here’s the blunt truth:

- Revenue can hide problems: A big sales year can still be a bad year if your direct costs are bleeding you dry.

- Bad coding ruins good decisions: If field costs hit overhead or overhead gets dumped into jobs randomly, every report becomes suspect.

- Tax time exposes sloppiness: What gets ignored during the year becomes urgent when returns, 1099s, payroll filings, and financial statements are due.

Practical rule: If you can’t identify your most profitable job and your worst job without digging through emails and paper folders, your bookkeeping system is broken.

What strong bookkeeping does

It gives you answers, not noise.

A proper construction accounting process should tell you:

- Which jobs are making money

- Whether your WIP is believable

- How much retainage is tying up cash

- What your payroll really costs

- Whether your tax and reporting obligations are being handled on time

That’s the difference between a company that survives a rough quarter and one that gets blindsided by it.

Building Your Financial Foundation Correctly

A Jacksonville contractor lands three solid jobs, stays busy for six months, and still cannot explain where the cash went. I see that mess all the time. The usual cause is not lack of work. It is a sloppy accounting foundation that never matched how a construction company operates.

Stop using generic accounting setups

Construction accounting needs to track jobs, phases, cost codes, billing terms, retainage, and payroll detail without guesswork. A generic setup might survive in a simple service business. In construction, it creates bad reports, bad bids, and ugly tax surprises.

Foundation Software’s summary of the CFMA 2023 Financial Survey points in the same direction many of us see in practice. Contractors using industry-specific systems report better project profitability than contractors forcing general software to do specialized work. No CPA who works with builders should be surprised by that.

QuickBooks can work. Sage can work. Foundation, Deltek, and other construction platforms can work. The software matters less than the setup. If the system cannot produce clean job cost detail, reliable WIP, progress billing support, payroll by job and phase, and clear retainage tracking, it is the wrong system or it has been configured badly.

Contractors outgrowing basic tools should also understand how construction enterprise resource planning (ERP) systems connect accounting, purchasing, field reporting, and project management. That connection matters because disconnected systems create duplicate entries, missed costs, and expensive confusion.

Build the chart of accounts for a contractor, not a coffee shop

A construction chart of accounts should mirror how jobs are estimated, staffed, billed, taxed, and reviewed. If it came straight from a default template, fix it now.

At a minimum, separate these categories clearly:

- Direct labor: Field payroll assigned to specific jobs

- Direct materials: Materials purchased for named projects

- Subcontractor costs: Trade partner costs by job and phase

- Equipment and job usage: Fuel, rental, repairs, and allocated use tied to the field

- Indirect construction costs: Costs related to production but not tied to one bid item

- Administrative overhead: Office payroll, rent, software, insurance, and back-office expense

- Retainage receivable: Earned revenue you have not collected yet

- Work in progress accounts: Accounts that support accurate overbilling and underbilling reporting

- Sales and payroll tax liabilities: Compliance accounts that must stay current

This is also where Florida contractors get careless. Sales tax treatment on materials, payroll tax deposits, worker classification, and entity-level tax planning all need to be built into the accounting system from day one. Recent federal tax changes have made timing and classification decisions more expensive to get wrong, especially for companies buying equipment, expanding crews, or changing entity structure. If your books are not organized correctly, your tax return turns into an expensive reconstruction project.

Set the reporting structure before the backlog grows

Your file needs rules, not just accounts.

Give every project a unique job number. Use cost codes that match how you estimate and manage the work. Set billing items to follow the contract schedule of values. Push payroll through the same job and phase structure so labor ends up where it belongs.

That setup work decides whether your reports are useful or decorative.

If you are reviewing options, study construction job costing software for contractors before you add more volume to a broken system. Fixing the foundation early costs far less than cleaning up twelve months of miscoded labor, retainage errors, and half-baked WIP schedules.

Software does not replace judgment

Someone still has to decide how labor burden is assigned, how retainage posts, how change orders affect revenue recognition, and whether a cost belongs in overhead or direct job expense. Software records decisions. It does not make them wisely.

That is why bookkeeping alone is not enough for a growing contractor. You need accounting oversight and fractional CFO discipline. A strong CPA firm will set up the books correctly, keep compliance tight, and translate the numbers into bid strategy, cash planning, tax planning, and profit improvement. Bookkeeping and Accounting of Florida Inc. provides that kind of support for Florida businesses. For many contractors, that level of financial leadership is not a luxury. It is how you stop guessing and start protecting margin.

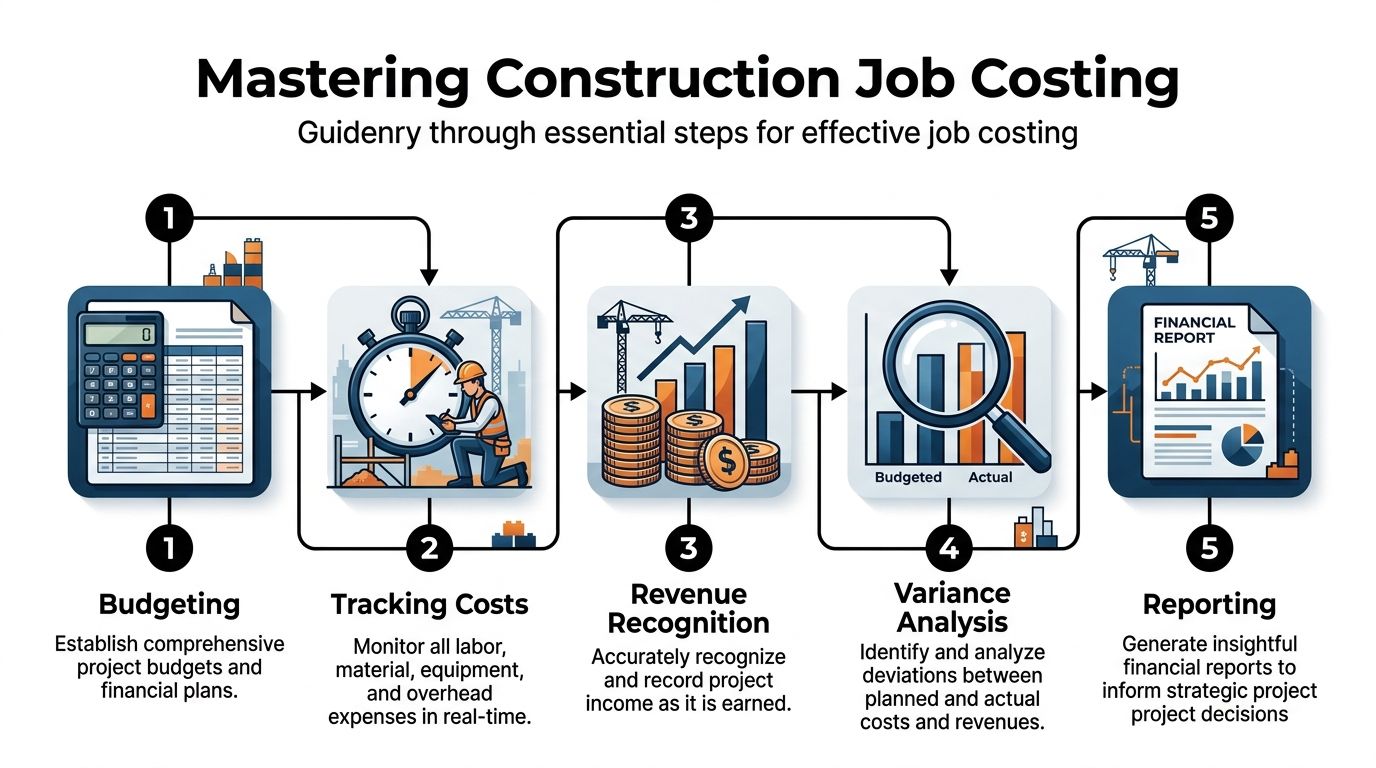

Mastering Job Costing and Project Financials

If your chart of accounts is the foundation, job costing is the engine. This process helps determine if bookkeeping for construction companies becomes useful or decorative.

A contractor doesn’t need prettier reports. A contractor needs to know whether Job 241 made money.

The four habits that keep job costing honest

According to Deltek’s construction bookkeeping guidance, a core methodology includes assigning a unique job number, breaking the job into phases and expense categories, recording every expense against the job daily, and reconciling budgets against actuals regularly. The same source notes that companies with integrated field-office systems report 23% fewer data entry errors and 15% faster month-end closes, and warns that lumping project and general costs can lead to 30-40% inaccurate profitability reports.

That’s exactly what I see in practice. The damage usually starts small. A fuel charge gets dumped into a general account. A superintendent’s time doesn’t hit the right job. Materials bought for one project get coded to another because someone was in a hurry. By month-end, the reports are polished nonsense.

Use this operating discipline instead:

Give every project a job number

No exceptions. If a transaction can’t be tied to a job when it should be, somebody stops and fixes it.Break the project into phases

Site work, framing, electrical, finishes, concrete, equipment, subcontracted scopes. Whatever reflects how you manage the work.Post costs daily

Waiting until month-end is how details get lost and overruns get discovered too late.Compare budget to actual constantly

If a category is drifting, you want to know while the project can still be corrected.

If you’re reviewing systems or tools, this guide to https://www.bookkeepingandaccountinginc.com/construction-job-costing-software/ is a useful starting point for what construction job costing software should support.

WIP is not optional

A work in progress report tells you whether the financial side of the job matches the progress in the field. That matters because revenue recognition, billing status, and cash flow can all drift out of alignment.

A decent WIP review helps you spot:

- Overbilling: You’ve billed ahead of earned revenue

- Underbilling: You’ve done work you haven’t billed properly

- Margin fade: The expected profit is eroding as costs rise

- Documentation gaps: The books say one thing and project records say another

A contractor who ignores WIP often ends up shocked by cash flow. They think a job is healthy because invoices went out. Meanwhile, the project may be underperforming, underbilled, or carrying retainage that won’t convert to cash quickly.

If your WIP schedule only gets attention when the banker asks for it, you’re using it wrong.

Here’s a simple way to think about it. Billing does not equal performance. Cash received does not equal profit. WIP is the check against self-deception.

Revenue recognition needs discipline

Longer-term jobs raise another issue. Revenue often has to be recognized based on the progress of the work, not just when the final invoice goes out. If job costing is sloppy, revenue recognition gets sloppy too.

That creates problems with financial statements, taxes, lending conversations, and owner decision-making. It also creates timing distortions that make one month look fantastic and the next one look awful, even when operations didn’t change much.

This video gives a useful overview of job costing mechanics in plain language.

Retainage and progress billing need their own controls

Progress billing keeps work moving. Retainage slows cash. Both need to be tracked carefully or your receivables report turns into fiction.

Keep these rules in place:

- Bill from approved schedules: Don’t let accounting invent billings without project documentation.

- Track retainage separately: It is earned money, but it is not the same thing as cash in hand.

- Match billing to approved change orders: Unapproved extra work is a donation, not revenue.

- Review old receivables by project: Aged AR means nothing if nobody ties it back to project status.

What I’d fix first in a messy file

When a contractor brings me a bad set of books, I don’t start with cosmetic cleanup. I start by asking three questions.

| Problem area | What usually went wrong | What to fix first |

|---|---|---|

| Job costs | Costs posted to broad categories or wrong jobs | Rebuild job mapping and cost categories |

| Billing records | Invoices not tied cleanly to project progress | Reconcile billings to contracts and approved changes |

| WIP support | Field status and books don’t agree | Review project schedules and financial postings together |

That’s where clarity starts. Not with prettier dashboards. With accurate cost assignment.

Handling Change Orders Subcontractors and Payroll

Construction accounting gets ugly in practice. Not because the rules are mysterious, but because people get busy and skip steps.

A project manager approves extra work in a text message. A subcontractor starts before anyone collects a W-9. Payroll runs fast because the crew needs checks, but the certified payroll backup is a mess. Then everyone acts surprised when billing, tax forms, and compliance reports don’t line up.

They do line up. They line up with the chaos that created them.

Change orders can’t live in email purgatory

Here’s a common Jacksonville scenario. The customer asks for additional scope. Your superintendent moves forward because the crew is already there. Weeks later, accounting tries to bill it. The owner says, “We never approved that amount.”

That argument starts because the process was weak.

A workable change order flow looks like this:

- Field identifies the change: Scope, labor impact, material impact, and time impact are documented immediately.

- Management prices it: Someone reviews cost, markup, and contract implications before work gets too far ahead.

- Customer approval is documented: Signed approval is ideal. Clear written authorization is the bare minimum.

- Accounting updates the job: Budget, billing schedule, and forecast all get revised.

- Collections tracks it aggressively: Change order revenue gets old fast when it sits unbilled.

Subcontractor compliance is boring until it gets expensive

You can’t treat subcontractor setup like an afterthought. Before payment goes out, the file should include a W-9, contract documentation, insurance information when required, and a process for year-end information reporting.

That sounds tedious. It’s still cheaper than fixing year-end 1099 problems after the fact.

I also recommend using document capture and approval workflows to keep vendor paperwork organized. If your AP process is still driven by inbox clutter and paper piles, this roundup of OCR software for invoices is worth reviewing.

A subcontractor should not be easier to pay than to verify.

Payroll mistakes can become compliance problems

Construction payroll isn’t simple. Even on private jobs, you’re dealing with job allocations, overtime, workers’ comp classifications, and tax deposits that must be right. Add public work, prevailing wage, or certified payroll, and the room for error gets even smaller.

A few examples I see repeatedly:

- Hours are correct, jobs are wrong

- Overtime is paid, but allocated poorly

- Certified payroll reports don’t match payroll records

- Fringe benefit treatment is misunderstood

- Employee and subcontractor classifications are sloppy

Public work makes this even less forgiving. If certified payroll is part of the job, your reports need to agree with payroll registers, employee classifications, pay rates, and job records. This overview of https://www.bookkeepingandaccountinginc.com/certified-payroll-reporting-requirements/ is a good reference for what those reporting obligations involve.

Three files every contractor should be able to produce fast

When books are controlled well, these records are easy to pull:

| File | What should be in it | Why it matters |

|---|---|---|

| Change order file | Approval, price backup, billing update | Prevents free work and invoice disputes |

| Subcontractor file | W-9, agreement, payment history, support | Keeps 1099 and vendor compliance clean |

| Payroll compliance file | Time records, payroll reports, job allocations, certified payroll support | Protects the company during audits and public project reviews |

Most small contractors don’t have a revenue problem. They have a documentation problem dressed up like a revenue problem.

The Monthly Close A Non-Negotiable Rhythm

The monthly close shows discipline. Not in January when your CPA is begging for missing statements. Every month. Same order. Same standards. Same follow-through.

If you skip the monthly close, you train your business to operate blind. You also guarantee that tax season will be miserable.

What a construction monthly close should include

A good close is not complicated. It is repetitive, and that’s the point.

Here’s the checklist I expect construction companies to follow:

| Task Category | Action Item | Why It Matters |

|---|---|---|

| Cash | Reconcile all bank accounts | Confirms your books match reality |

| Credit cards | Reconcile every card and review coding | Catches miscoded job costs and duplicate charges |

| Accounts receivable | Review open invoices, retainage, and old balances by project | Improves collections and keeps cash flow honest |

| Accounts payable | Match vendor balances to unpaid bills and due dates | Prevents missed payments and duplicate entries |

| Payroll | Tie payroll reports to the general ledger and job costing | Confirms labor is hitting the right places |

| Job costing | Review budget-to-actual reports for active jobs | Flags margin erosion early |

| WIP | Compare earned revenue, billings, and project status | Keeps project financials credible |

| Fixed assets and equipment | Review purchases, disposals, and capitalization treatment | Supports tax reporting and depreciation decisions |

| Taxes | Verify payroll filings, sales tax issues, and other compliance items | Keeps you from learning about problems too late |

| Financial statements | Review P&L, balance sheet, and project reports with management | Turns data into decisions |

Internal controls are not corporate fluff

Owners of smaller contractors often roll their eyes at “internal controls.” Then money disappears, duplicate payments go out, or payroll errors sit undetected for months.

You don’t need a giant accounting department. You do need basic guardrails.

Use controls like these:

- Separate approval from payment entry: The person entering bills shouldn’t be the only one approving them.

- Require review of unusual transactions: Big journal entries and reclasses deserve scrutiny.

- Limit software access: Not everyone needs permission to edit payroll, vendors, or reconciliations.

- Review checks and ACH activity: Owners should know where cash is going.

Clean books come from routine. Fraud and errors thrive in delay, confusion, and over-trust.

Close fast enough to matter

Financial statements that arrive long after month-end are less useful. You need timely information while the jobs are still active and the decisions still matter.

A disciplined monthly close provides an advantage. You can challenge a drifting project, collect old receivables, question payroll allocations, and fix coding errors before they infect a full quarter.

That rhythm is what turns accounting from recordkeeping into management.

Why Your Numbers Need a Guide The Fractional CFO

A bookkeeper records history. A fractional CFO helps you decide what to do next. Those are not the same job, and too many contractors learn that late.

If your company is growing, juggling multiple jobs, carrying equipment debt, bidding more aggressively, or dealing with tighter lender and bonding expectations, you need more than reconciled accounts. You need interpretation, planning, and somebody willing to tell you when your strategy is sloppy.

What a fractional CFO does

A strong fractional CFO helps a construction company:

- Forecast cash flow by project and company-wide

- Review bid strategy against real cost history

- Analyze whether overhead is under control

- Plan for tax obligations and entity-level decisions

- Prepare for lender, bonding, and investor conversations

- Build accountability around financial reporting

That matters because construction owners make expensive decisions fast. Hiring, equipment purchases, financing, expansion into new markets, and pricing strategy all depend on whether the numbers are understood properly.

Tax law changes don’t wait for you to catch up

The author’s brief is right about one thing most contractors underestimate. Tax law changes matter, and small businesses often don’t know what’s required until they’re already behind.

Construction companies deal with equipment purchases, depreciation questions, payroll tax obligations, contractor reporting, and revenue recognition issues that can affect tax filings significantly. The rules shift. Filing requirements change. Documentation standards tighten. A contractor who relies on last year’s assumptions is asking for trouble.

That’s why I’m opinionated here. You need someone watching the tax side during the year, not just filing returns after the damage is done.

New compliance issues are creeping in

Many owners get blindsided by this. Compliance is no longer limited to payroll filings and year-end tax forms.

According to Uplinq’s summary of an emerging ESG reporting trend in construction, a 2025 Deloitte report notes that 68% of construction firms face ESG disclosure mandates under updated SEC rules, with non-compliance risking 15-20% financing cost increases. If that feels far away, it won’t stay that way for firms seeking financing, larger contracts, or work with more advanced counterparties.

A standard bookkeeper usually won’t build systems for that. A fractional CFO should.

That may involve asking smarter questions about project cost tracking, vendor documentation, reporting structure, and whether sustainability-related costs or compliance obligations need to be mapped cleanly into your financial process. The point isn’t to chase buzzwords. The point is to stay finance-ready and contract-ready.

This is the practical case for outside guidance

Hiring a full-time CFO is expensive. Many small and midsize contractors don’t need one every day. They do need executive-level financial oversight on a consistent basis.

That’s what fractional CFO support is for. If you want a plain-language breakdown of the role, this page on https://www.bookkeepingandaccountinginc.com/what-is-fractional-cfo-services/ lays out what those services typically cover.

Good bookkeeping tells you what happened. Good CFO guidance tells you what to stop, what to fix, and what to fund.

If your company is still treating accounting as a cleanup function, you’re behind. The contractors that grow safely use financial leadership before the crisis, not after it.

Frequently Asked Questions

Do construction companies really need specialized bookkeeping

Yes. Construction is too complex for generic bookkeeping. You’re dealing with job costing, progress billing, retainage, subcontractors, payroll compliance, and project-level profitability. If your system doesn’t track those items cleanly, the reports won’t help you make decisions.

Can QuickBooks handle bookkeeping for construction companies

It can, if it’s configured correctly. QuickBooks is not magic. The chart of accounts, customer and job structure, payroll mapping, billing workflow, and reporting setup all matter. A bad QuickBooks file is still a bad accounting system.

How often should job costs be reviewed

Daily posting is ideal for active costs. Formal review should happen at least monthly, and more often on larger or tighter-margin jobs. Waiting until quarter-end is lazy accounting and bad project management.

What’s the biggest bookkeeping mistake contractors make

Mixing job costs, overhead, and billing activity in a way that destroys visibility. The owner then reads reports that look official but aren’t accurate enough to trust. That leads to bad bids, bad tax planning, and bad cash decisions.

Do I need a fractional CFO if I already have a bookkeeper

Probably, if you’re growing or making larger financial decisions. A bookkeeper records transactions. A fractional CFO helps with forecasting, cash planning, margin analysis, tax strategy coordination, and decision support. If nobody is advising you at that level, the owner usually ends up making financial calls with incomplete information.

What records should I keep for subcontractors and payroll

For subcontractors, keep tax forms, agreements, invoices, payment records, and related compliance documents. For payroll, keep time records, pay details, job allocations, tax filings, and support for any certified payroll or prevailing wage reporting. If pulling those files feels difficult, your process needs work.

Why does month-end take so long in construction

Because many contractors delay coding, approval, and reconciliation work during the month. Then accounting tries to reconstruct reality after the fact. Fast closes come from discipline during the month, not heroics after it.

When should a contractor bring in professional accounting help

Early. Not when the IRS sends a notice, not when your bonding company questions the numbers, and not when you realize your most recent “profitable” job lost money. Good accounting support costs less than cleanup, penalties, missed deductions, and poor decisions.

If your construction company needs clean books, stronger compliance, better job costing, and real financial guidance, Bookkeeping and Accounting of Florida Inc. can help you get your numbers under control before they start controlling you. For contractors in Jacksonville and across Northeast Florida, that means bookkeeping, payroll, tax support, and fractional CFO guidance built around how construction businesses operate.