You know the drill. Receipts are stuffed in a drawer, payroll is due, your bank balance looks busy, and tax deadlines keep sneaking up like a raccoon in the garage. You’re working hard, but you’re still asking the question that makes business owners grind their teeth: “Am I making money, or just moving cash around?”

That’s where cpa and bookkeeping stops being accounting jargon and starts becoming a survival issue.

A lot of owners treat bookkeeping like flossing. They know they should do it, they put it off, and then they act surprised when something expensive starts hurting. A bookkeeper and a CPA are not the same thing, and hiring the wrong one at the wrong stage creates problems that show up in taxes, cash flow, audits, lender conversations, and growth decisions.

The short version is simple. A bookkeeper keeps the financial engine clean and running. A CPA reads the gauges, spots the risk, and helps you steer. If you want real financial management, not just year-end panic control, you need to understand both.

Are You Managing Your Books or Are They Managing You

A Jacksonville business owner called me once with a sentence I hear all the time: “I think everything’s fine, but I’m not sure.” That’s not a financial system. That’s a crossed-fingers strategy.

She had sales coming in, vendors getting paid, and a tax preparer she talked to once a year. What she didn’t have was a clean set of books, a real view of cash flow, or confidence in her numbers. She was running the business by checking the bank app and hoping for the best. That works right up until it doesn’t.

The two roles most owners confuse

A bookkeeper handles the day-to-day financial recordkeeping. They track income, expenses, bills, invoices, payroll, and account balances. They make sure what happened in your business gets recorded correctly.

A CPA steps in at a higher level. They deal with tax planning, compliance, financial interpretation, higher-risk accounting issues, and strategic advice. If the bookkeeper builds the map, the CPA helps you decide where to go and keeps you from driving into a swamp.

Clean books don’t just make tax season easier. They tell you whether your business is healthy or just loud.

What this means for a Florida business owner

If your books are always behind, if you dread tax notices, or if you don’t know which customers, jobs, or service lines are profitable, you don’t have a bookkeeping problem alone. You have a financial leadership problem.

This is the core idea. CPA and bookkeeping work best as a partnership. One gives you accurate records. The other turns those records into decisions, compliance, and a plan for growth.

The Foundation What a Bookkeeper Really Does

A good bookkeeper is not a glorified data-entry clerk. That idea needs to die. A good bookkeeper is the person who keeps your financial pulse accurate every day.

Think of a bookkeeper like the nurse who takes your vitals before the doctor walks in. If the chart is wrong, the diagnosis is wrong. Same thing in business. If your numbers are late, sloppy, or incomplete, every tax decision, cash flow decision, and hiring decision sits on bad information.

The daily and monthly work that keeps a business upright

A real bookkeeping function usually includes:

- Recording transactions: Sales, deposits, expenses, transfers, loan payments, owner draws, and credit card activity.

- Managing accounts receivable: Sending invoices, tracking customer payments, and following up before old balances become fossils.

- Managing accounts payable: Making sure vendor bills are entered, approved, and paid on time.

- Processing payroll support: Keeping wage records, tax withholdings, and payroll entries in order.

- Maintaining the general ledger: So your profit and loss statement and balance sheet aren’t fiction.

- Bank and credit card reconciliations: Matching your books to real statements, not to your memory.

That last one matters more than most owners realize. Monthly bank reconciliation is a critical control mechanism that detects discrepancies averaging 1-5% of monthly transactions if performed inconsistently, can reduce year-end audit adjustments by up to 40%, and cut tax preparation costs by 30% when books are kept clean, according to NerdWallet’s discussion of startup bookkeeping controls.

Why contemporaneous records matter

“Contemporaneous” is accountant language for “record it while it’s still fresh and provable.” Not six months later when you’re staring at a mystery charge from a vendor whose name sounds vaguely familiar.

If you run construction, this matters because job costs move fast. If you run a healthcare practice, this matters because billing, reimbursements, and timing issues can muddy the water quickly. If you run any business at all, this matters because stale books turn simple questions into archaeology.

Here’s the practical rule:

Practical rule: If your reconciliations are behind, your financial statements are not decision-ready.

Tools help, but process matters more

QuickBooks can do a lot. Bank feeds, rule-based categorization, recurring transactions, and reporting can save time. But software doesn’t fix bad habits. It just lets you make mistakes faster if nobody’s reviewing the work.

If you want your team to sharpen fundamentals, there are solid bookkeeping resources for accounting professionals that explain the nuts and bolts well. For business owners who want practical cleanup habits, these small business bookkeeping tips are the kind of basics that keep small messes from turning into year-end disasters.

The Strategist What a CPA Brings to the Table

If the bookkeeper keeps the records clean, the CPA decides what those records mean and what you should do next. That’s the difference.

A CPA is the specialist doctor in this analogy. The nurse gets accurate vitals. The specialist studies the chart, spots the underlying issue, and tells you whether the problem is diet, stress, surgery, or all three. In business terms, that means taxes, compliance, entity issues, revenue recognition, planning, and long-range financial decisions.

Where a CPA earns their keep

A CPA should help you with work that has consequences if handled badly:

- Business tax preparation and filing

- Tax planning tied to business decisions

- Audit and review support

- Financial statement analysis

- Owner compensation planning

- Cash flow forecasting

- Compliance with accounting rules that are easy to get wrong

- Guidance when tax law changes affect your filings or structure

Tax law changes matter because they change how you plan, not just how you file. Owners who wait until return-prep time usually miss the chance to act while the year is still in motion. By then, the toothpaste is out of the tube and accountants are left trying to make the best of what already happened.

The high-stakes stuff a bookkeeper shouldn’t wing

One of the clearest examples is ASC 606 revenue recognition. This rule matters when revenue has to be recognized over contract performance periods instead of when cash lands in the bank. That comes up in SaaS, construction progress billings, retainers, and other multi-period contracts.

Non-compliant firms can face audit restatements of 20-30% and up to 15% higher effective tax rates due to premature income booking, and proper implementation requires a 5-step model that CPAs are trained to execute, as explained in Bench’s overview of startup accounting and ASC 606.

That’s not a “watch a video and figure it out” area. That’s a “get qualified help before you create a mess” area.

Compliance is broader than income tax

Many owners hear “compliance” and think only about filing returns. That’s too narrow. Compliance also means recognizing revenue correctly, documenting positions, keeping support for deductions, and preparing financial records that won’t collapse under lender, investor, or audit scrutiny.

If your business has software subscriptions, investor reporting, internal controls, or formal reporting needs, it also helps to understand the bigger picture around SaaS compliance costs and scope. Different frameworks have different requirements, and a CPA helps you sort out what applies and what’s just noise.

For owners who want practical tax-side planning instead of last-minute scrambling, these business tax planning strategies are the right conversation to have before year-end, not after.

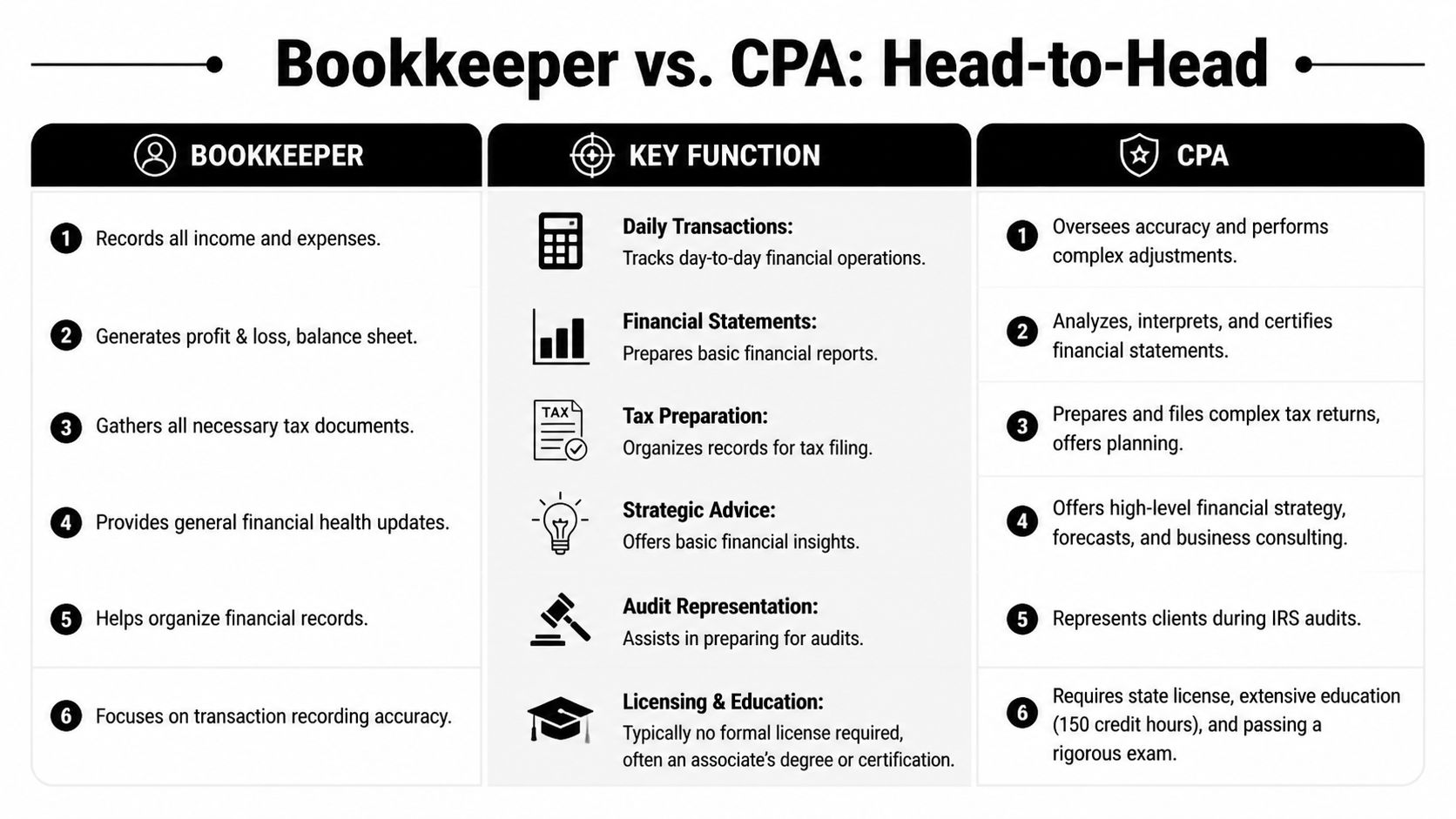

Bookkeeper vs CPA A Head-to-Head Comparison

People ask whether they need a bookkeeper or a CPA as if they’re choosing between a hammer and a wrench. That’s the wrong question. These roles are different because the work is different.

Bookkeeping has been around since 3300 BC in Mesopotamia, the modern double-entry system was codified in 1494, and the U.S. CPA designation arrived later in 1896, with demand surging after income taxes began in 1913, according to this history of bookkeeping and the accounting profession. That history matters because it explains why the roles are still separate today. One role records. The other interprets, certifies, and advises.

What happens in real business situations

Daily operations

The bookkeeper records the money moving in and out, posts bills and invoices, and reconciles accounts.

The CPA usually doesn’t enter every daily transaction. The CPA reviews the quality of the records, makes higher-level adjustments when needed, and flags accounting issues that affect reporting or taxes.

Tax season

The bookkeeper organizes the records, closes out the books, and makes sure the documentation isn’t a junk drawer.

The CPA uses those records to prepare returns, apply tax rules, and identify planning opportunities. If the books are a mess, the CPA spends time cleaning history instead of advising on the future.

Financial planning

The bookkeeper can tell you what happened.

The CPA should help you understand why it happened and what to do about it. That includes forecasting, timing decisions, entity questions, compensation planning, and guidance that ties accounting to operations.

Bad books create bad decisions. Fancy reporting on top of bad books just gives you prettier confusion.

Audits and compliance

The bookkeeper gathers records and keeps support organized.

The CPA handles the technical side, prepares or reviews financial statements, responds to issues, and helps you deal with auditors, tax authorities, lenders, or other stakeholders.

Bookkeeper vs. CPA at a Glance

| Aspect | Bookkeeper | CPA (Certified Public Accountant) |

|---|---|---|

| Primary focus | Daily financial accuracy | Compliance, tax, analysis, and strategy |

| Typical work | Transaction entry, AP, AR, payroll support, reconciliations | Tax returns, planning, audits, complex accounting, advisory |

| Main output | Clean books and routine reports | Tax filings, guidance, adjustments, financial interpretation |

| Time horizon | Day to day and month to month | Quarterly, annual, and long term |

| Licensing | Usually not state-licensed as a CPA | State-licensed CPA |

| Best use | Keeping records current and usable | Turning records into decisions and compliance |

| Cost structure | Often hourly or monthly service | Often project-based, retainer, or advisory engagement |

The plain-English takeaway

If your bookkeeper is trying to be your tax strategist, that’s a problem. If your CPA is trying to reconstruct a year of missing bookkeeping in March, that’s also a problem.

Different jobs. Different training. Same goal. Healthy financials.

When to Hire a Bookkeeper a CPA or Both

It’s Friday afternoon. Payroll is due, sales tax is coming up, your loan officer wants current financials, and your CPA just asked why last quarter still isn’t reconciled. That’s the moment a lot of owners realize they do not have an accounting system. They have a pile of receipts, a bank balance, and a prayer.

Here’s the straight answer. Hire based on complexity, risk, and how expensive your mistakes have become.

Stage one, the startup or solo owner

If your business is simple, start with bookkeeping. Good bookkeeping gives you clean records, current numbers, and a tax return that does not turn into an archaeological dig every spring.

You do not need a CPA in your inbox every week at this stage. You do need your chart of accounts set up properly, your QuickBooks file organized, your accounts reconciled, and your records updated on time. Skip that work and you are building a house on wet sand.

Bring in a bookkeeper now if any of this sounds familiar:

- You are behind every month: If you cannot close the books cleanly, you are already driving by looking in the rearview mirror.

- You mix business and personal spending: That creates tax problems and makes your reports unreliable.

- You send invoices late or randomly: Cash flow gets ugly fast when billing is sloppy.

- You run the business from the bank balance: Your bank account shows cash. It does not show profit, debt, margins, or trouble brewing.

Stage two, the growing SMB

Once revenue picks up, employees are added, and compliance starts multiplying, you need both. Many owners often wait too long, usually because they still see accounting as a tax-season expense instead of a year-round operating tool.

A bookkeeper keeps the engine running. A CPA helps you avoid driving it into a ditch.

That partnership matters because bad records do more than create a messy tax return. They can lead to payroll mistakes, sales tax problems, lender issues, missed deductions, bad pricing decisions, and reports you cannot trust. If you are making hiring, purchasing, or expansion decisions from shaky numbers, you are guessing in a nicer spreadsheet.

Different businesses feel this at different pressure points. Contractors need clean job costing before they can tell which jobs make money. Medical practices need orderly billing and reimbursement records before they can judge performance. Retailers need inventory controls that match reality, not wishful thinking. Same lesson every time. If the books are weak, the decisions are weak.

Analysts at Thomson Reuters found that many CPA firms decline clients whose records are in poor shape, and many firms still limit their work to compliance rather than advisory, as explained in Thomson Reuters’ discussion of advisory obstacles for accounting firms. Messy books do not just waste time. They can block access to better advice.

If you want strategy from a CPA, give them numbers worth trusting.

Here’s a useful overview of what that relationship can look like in practice:

Stage three, the scaling company

Once you are hiring managers, opening locations, adding service lines, chasing financing, or trying to improve margins, bookkeeping plus tax prep is no longer enough. At that point, many businesses also need fractional CFO support.

A fractional CFO helps you set budgets, forecast cash, track KPIs, prepare for lenders, and make owner-level decisions with less guesswork. You may not need a full-time CFO. You probably do need someone watching the big picture before a small leak turns into a flood.

There is another practical issue owners ignore until it bites them. Continuity. If your whole financial operation depends on one outside CPA who is overloaded, slowing down, or nearing retirement, you have a succession risk whether you planned for one or not. A coordinated team is safer because your records, history, and decision support are not trapped in one person’s head.

For businesses that want bookkeeping, tax, payroll, audit, and advisory support working together, one option is accounting and taxation services for Florida businesses under one roof. That setup reduces handoff problems and gives you better odds of getting timely answers when the business starts moving faster.

Why Florida Businesses Choose Our Firm for Stability and Growth

A lot of firms can prepare a tax return. Fewer can keep the books clean, explain the numbers in plain English, and stay with you as the business changes.

That matters more right now because the profession has a continuity problem. With 75% of experienced accountants nearing retirement age, the accounting pipeline crisis creates continuity risk for small businesses, and choosing an established firm over a solo practitioner helps reduce the risk of losing support when one advisor retires, as noted by The CPA Journal’s analysis of the accounting pipeline.

Why continuity beats personality-only relationships

A lot of owners have “their accountant.” That feels comfortable until that person retires, slows down, gets overloaded, or disappears during the busiest week of the year. Then you’re left scrambling for context, records, and help.

An established team model is safer. It gives you process, shared knowledge, and coverage when one person is unavailable. That’s not cold or corporate. It’s practical.

What businesses actually need from an accounting partner

Florida businesses usually don’t need more jargon. They need someone to:

- Clean up messy books: Especially in QuickBooks, where small setup mistakes can snowball.

- Keep them compliant: Tax filings, payroll support, reporting, and documentation all have moving parts.

- Help them adjust to tax law changes: Not by panicking, but by planning early and acting deliberately.

- Provide fractional CFO guidance: Because many growing companies need financial leadership before they can justify a full-time executive.

- Understand industry quirks: Construction job costing is not the same as healthcare reimbursements or nonprofit reporting.

That’s why many owners move toward firms with a broad service base instead of relying on a single person who mainly handles returns. If you want to see the scope of support available, accounting and taxation services cover the practical mix most small and midsize companies need, from bookkeeping and tax prep to audits and advisory work.

My opinion, plain and simple

If your current setup only talks to you at tax time, that’s not enough.

If nobody is helping you read the numbers, plan around tax law changes, and make decisions before problems show up, you don’t have financial guidance. You have historical paperwork.

Your Next Steps to Financial Clarity

You don’t need more spreadsheets. You need a cleaner system and better decisions.

Start with a blunt self-check:

- Are your books current? If reconciliations and reports lag, your numbers aren’t usable.

- Do you know your real profit? Not your bank balance. Your actual profit.

- Can you hand over organized records today? If a lender, auditor, or CPA asked, could you do it without a scavenger hunt?

- Are you planning for tax law changes before year-end? If not, you’re reacting, not managing.

- Do you have anyone acting as a financial guide? If not, that gap will eventually cost you.

Then schedule a real conversation with an accounting professional who can look at your books, your tax posture, and your growth plans together.

The payoff isn’t just compliance. It’s peace of mind. It’s knowing what’s happening in your business without guessing. It’s being able to focus on operations, customers, and growth instead of trying to decode your own ledger at midnight.

If your business needs clearer books, stronger tax planning, or fractional CFO guidance, talk to Bookkeeping and Accounting of Florida Inc.. We help Florida business owners turn messy financials into usable numbers, stay compliant, and make decisions with more confidence.