Your receipts are in email, your card charges are in three different apps, payroll is due, and your tax preparer keeps asking for “clean books.” Meanwhile, your spreadsheet has tabs named Final, Final 2, and Use This One.

That is not bookkeeping. That is risk wearing a business-casual outfit.

If you want the blunt answer on how to hire a bookkeeper, here it is: stop treating the role like data entry. A good bookkeeper protects compliance, cleans up cash flow visibility, supports tax filing, and gives your business a usable financial picture. A bad one gives you late reports, ugly reconciliations, and year-end misery.

In Jacksonville and across Northeast Florida, I see the same pattern in small businesses, medical practices, contractors, and non-profits. Owners wait too long, hire too casually, and discover the problem when a bank balance looks wrong, payroll is off, or an audit request lands in the inbox.

Why Your Business Needs More Than a Spreadsheet

A spreadsheet is fine for a lemonade stand. It is not fine for a growing business with payroll, sales tax, vendor payments, reimbursements, and changing tax rules.

Nearly half of small businesses, 45%, operate without employing either an accountant or a bookkeeper, which leaves owners juggling critical financial work themselves and increases the risk of errors, compliance issues, and missed growth opportunities, according to Clutch’s small business accounting resource study.

Bookkeeping is not clerical cleanup

Owners often think bookkeeping means entering transactions and reconciling the bank. That is only the surface.

A competent bookkeeper tracks income correctly, codes expenses properly, keeps payroll support organized, issues or tracks invoices, and makes sure your reports reflect reality. If the numbers are wrong at the bookkeeping level, everything built on top of them is wrong too. Tax filings. Cash planning. Loan applications. Profit analysis. All of it.

Messy books cost you twice

The first cost is the obvious one. You spend time fixing mistakes.

The second cost is worse. You make decisions from bad information. You hire too soon, delay purchases you could afford, miss deductions, or assume a job was profitable when it was not.

Practical rule: If you cannot pull a current Profit and Loss, Balance Sheet, and a sensible view of cash activity without scrambling through emails, you need a bookkeeping process that works.

Compliance got harder, not easier

Tax law changes, reporting requirements, payroll rules, and industry-specific filing expectations do not slow down because you are busy. Small business owners often do not know what is required until a deadline is close or already missed.

That is why hiring a bookkeeper should be treated as a strategic move, not an administrative one. The right person or firm gives you current books, cleaner tax prep, fewer surprises, and a much better shot at staying compliant all year instead of panicking in March.

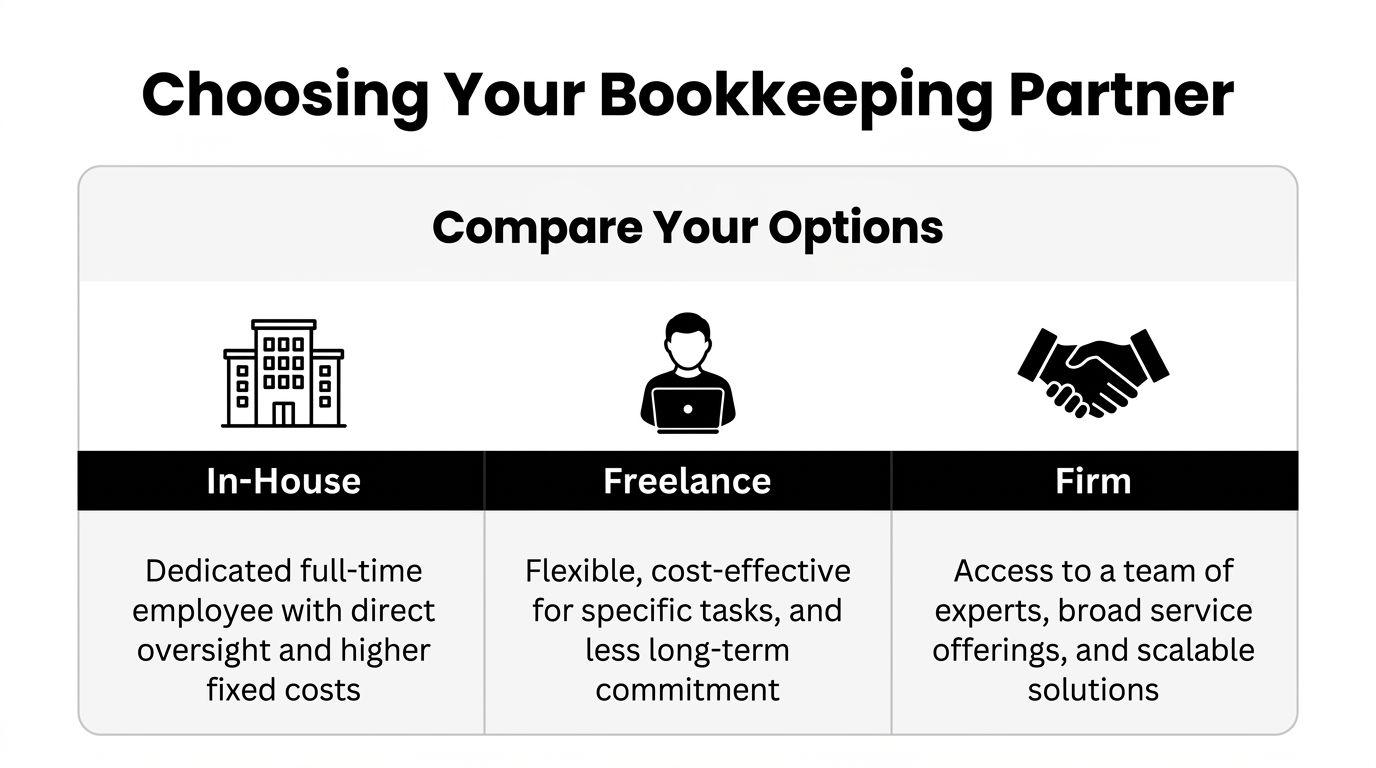

Choosing Your Financial Partner In-House Freelance or Firm

There are three common ways to hire bookkeeping help. You can bring in an employee, hire a freelancer, or work with an outsourced firm.

All three can work. Only one is the best fit for most growing businesses.

In-house works when volume is heavy

An in-house bookkeeper gives you direct oversight and immediate access. That matters if you process a high volume of transactions, handle lots of paper, or need someone on-site regularly.

The downside is obvious. You are responsible for hiring, training, supervision, coverage, and quality control. If that person quits, gets sick, or is not strong enough technically, your finance function goes with them.

Freelancers look cheap until they are not

Freelancers can be a decent fit for very small businesses with straightforward books. If your operation is simple and your expectations are modest, a freelancer may be enough for a while.

But freelancers create a single point of failure. They also vary wildly in responsiveness, documentation habits, industry knowledge, and cleanup ability. Some are excellent. Some are just good at saying “I know QuickBooks.”

Firms give you depth, continuity, and adult supervision

This is my clear recommendation for most small and mid-sized businesses. A firm gives you process, backup, review layers, broader expertise, and room to grow.

That matters because bookkeeping should not stop when one person is unavailable. It also should not rely on one person’s memory. You want a system.

Outsourced bookkeeping services show 90% client retention versus 70% for in-house hires, largely because team redundancy and consistent coverage reduce the disruption that comes with relying on one employee, according to Enkel’s bookkeeping hiring benchmarks.

Bookkeeping models compared

| Criteria | In-House Employee | Freelancer | Outsourced Firm (e.g., B&A of Florida) |

|---|---|---|---|

| Oversight | Direct day-to-day supervision | Limited unless you manage closely | Structured process and review |

| Coverage | Weak if one person is out | Weak if one person is out | Stronger due to team support |

| Scalability | Requires another hire later | Can become stretched quickly | Easier to expand services |

| Industry expertise | Depends on one hire | Inconsistent | Broader bench and specialization |

| Strategic guidance | Limited unless senior | Usually limited | Easier path to fractional CFO support |

| Risk management | Tied to one employee | Tied to one contractor | Shared knowledge and continuity |

My opinion on who should choose what

Choose in-house if your transaction volume is constant, you need someone physically present, and you are prepared to manage the role properly.

Choose freelance only if your books are simple, your internal controls are solid, and you are comfortable monitoring the work closely.

Choose a firm if you want bookkeeping, compliance support, tax-readiness, and the option to add advisory help without building an internal department. If you are weighing those tradeoffs, this overview of which bookkeeper business model fits your company is useful.

Key takeaway: Most owners do not need one person with a laptop. They need a reliable accounting function.

Why the firm model wins for growing companies

A growing company usually needs more than reconciliations. It needs monthly reporting, payroll coordination, sales tax awareness, year-end support, and somebody who notices when a number looks off.

Sooner or later, it also needs guidance. That is where fractional CFO support becomes valuable. Not because every business needs a boardroom deck, but because every business needs someone to interpret the numbers and help the owner make better decisions.

If your bookkeeping setup cannot grow into that relationship, you will end up hiring twice.

Attracting the Right Talent for Your Financials

Most owners write terrible bookkeeping job descriptions.

They ask for “detail oriented,” “organized,” and “good with numbers,” then wonder why they get a pile of vague resumes from people who have touched QuickBooks once and now call themselves accounting professionals.

If you want to know how to hire a bookkeeper well, start by writing a role that filters people out.

Write the job around real work

Do not post a fluffy summary. List the actual duties.

Your description should mention tasks such as bank and credit card reconciliations, accounts payable, accounts receivable, payroll support, month-end close, sales tax support, and financial reporting. If you need cleanup work, say so. If you need job costing, say so. If you need someone who can keep the CPA fed with clean records at tax time, say that too.

The more specific you are, the fewer unqualified applicants you will have to sort through.

Name the software and the environment

If your business runs on QuickBooks Online, say it plainly. If you also use bill pay tools, payroll platforms, point-of-sale integrations, or donor tracking systems, include them.

You are not looking for a person who is “comfortable learning software.” You are looking for a person who can operate in the software you already use without turning the first month into a rescue mission.

A strong posting usually includes:

- Core platform requirement: QuickBooks Online proficiency, not vague “accounting software experience.”

- Reporting expectations: Monthly Profit and Loss, Balance Sheet, and supporting reconciliations.

- Workflow reality: Remote, hybrid, or on-site. Daily, weekly, or monthly communication cadence.

- Industry background: Healthcare, construction, non-profit, retail, or whichever environment matches your business.

- Problem level: Maintenance, cleanup, catch-up, or full rebuild.

Ask for proof, not adjectives

“Experienced” means nothing without context.

Require candidates to explain what types of accounts they reconciled, what reports they prepared, how they handled uncategorized transactions, and whether they have worked with payroll, sales tax, or year-end handoff to a CPA. If they claim industry experience, ask what that looked like in practice.

Don’t forget the hidden requirement

The essential work is not just entering transactions. The job involves maintaining a dependable reporting process.

That means your job description should also mention communication. You want someone who can ask for missing documents, flag anomalies, and explain what changed from one month to the next without sounding like they are reading from a help article.

Hiring shortcut: If the role you need includes bookkeeping, compliance support, cleanup, software setup, and owner guidance, you are no longer hiring a simple bookkeeper. You are hiring a finance function.

The alternative most owners overlook

The DIY route sounds cheaper because you only think about wages. You do not think about screening, training, process design, supervision, backup, and cleanup if the hire goes sideways.

That is why many owners eventually decide not to recruit this role from scratch at all. They choose a firm with a vetted team, documented workflows, and the ability to provide both day-to-day bookkeeping and bigger-picture advice when the business gets more complex.

Screening Candidates Beyond the Resume

A resume can tell you where someone worked. It cannot tell you whether they can untangle a bad reconciliation, catch duplicate expenses, or keep your books clean during a busy month.

That is why screening matters more than sourcing.

Common hiring mistakes include skipping industry-specific vetting and ignoring trial periods, which can lead to 25% post-hire churn, while structured trials and reference checks improve success rates by over 50%, according to Beancount’s guide to hiring a professional bookkeeper.

Ask situational questions, not biography questions

“Tell me about yourself” is polite. It is also useless.

Ask what they would do when a bank reconciliation does not match, when payroll numbers differ from expectations, when an owner mixes personal and business transactions, or when month-end documents arrive late. Those answers expose judgment, process, and communication style.

Good candidates explain their steps clearly. Weak candidates hide behind jargon.

A few interview questions I like:

- Reconciliation test: “You find a discrepancy in the bank rec at month-end. What do you check first?”

- Payroll judgment: “How do you handle a payroll issue that affects prior periods?”

- Owner management: “What do you do when a client or owner is slow to provide documents?”

- Reporting discipline: “What reports do you expect to deliver monthly, and what should accompany them?”

- Error ownership: “Tell me about a mistake you found in bookkeeping records and how you corrected it.”

Run a paid skills test

If you skip the test, you are guessing.

Give the finalist a paid project inside QuickBooks or in a sample file. Ask them to categorize a small set of transactions, identify issues in a reconciliation, or clean up a short period with obvious coding errors. You do not need a circus. You need evidence.

This also tells you how they document work, how they ask questions, and whether they panic when the file is imperfect. Real books are always imperfect.

Check references like you mean it

Do not ask, “Were they nice?”

Ask whether the person met deadlines, communicated clearly, kept records organized, and could be trusted with recurring financial work. Then ask the blunt question: would you rehire them?

If you want a more complete hiring process, this guide on how to find a good accountant helps sharpen the screening standard.

Red flags that should end the process

Red flags

- Vague software answers: They “used QuickBooks” but cannot explain what they did in it.

- No reconciliation discipline: They talk about bookkeeping without mentioning monthly reconciliations.

- Weak industry awareness: They claim sector experience but cannot describe relevant workflows.

- Defensive communication: They get irritated by follow-up questions.

- No testing tolerance: They resist a paid trial or practical exercise.

Video can also help frame what to look for in a capable bookkeeping partner:

Why resumes fail in regulated industries

In healthcare, construction, and non-profits, a generic background is not enough. You need a bookkeeper who understands the shape of the work, not just the software menu.

That is why the interview should include industry-specific scenarios. Ask a construction candidate about job costing. Ask a healthcare candidate how they keep records organized for compliance and reporting. Ask a non-profit candidate how they handle restricted funds and audit preparation.

A strong answer sounds practical. A weak answer sounds memorized.

Industry-Specific Needs for Healthcare Construction and Non-Profits

Generic bookkeeping advice is usually written for generic businesses. Your business is not generic.

If you operate a medical practice, a construction company, or a non-profit in Northeast Florida, hiring the wrong bookkeeper is not just annoying. It creates compliance trouble, reporting mistakes, and expensive cleanup.

A 2025 AICPA survey found 62% of small healthcare practices struggled with financial compliance because of mismatched bookkeeping hires, which is a strong warning that industry-specific expertise matters, as summarized in Lendio’s bookkeeping hiring guide.

Healthcare needs precision and documentation

Healthcare bookkeeping has little tolerance for sloppy process. You need clean records, consistent reporting, organized payroll support, and disciplined handling of financial documentation tied to practice operations.

A candidate who has only worked in a basic retail or service environment may not understand the level of structure a healthcare business needs. Ask about prior work with medical practices, reporting cadence, vendor controls, and how they handled documentation for year-end and compliance reviews.

Construction lives and dies by job costing

Construction bookkeeping is where weak hires get exposed fast.

A contractor needs someone who understands job costs, subcontractor payments, payroll support, draw tracking, and the difference between revenue on paper and cash in the bank. If the bookkeeper cannot keep projects separated properly, your reporting becomes fiction.

Ask candidates to explain how they would organize costs by job, track billable categories, and support reporting that helps you see whether a project is profitable.

Contractor rule: If your bookkeeper cannot speak clearly about job costing, they are not your bookkeeper.

Non-profits need accountability, not generic small business books

Non-profits face a different kind of pressure. Boards expect timely reporting. Grant activity needs clean tracking. Audits demand organized records.

That means your bookkeeper must understand how to maintain books that support stewardship and transparency. A generic small business setup can leave a non-profit with reporting that makes sense to no one.

What to verify before you hire

Do not settle for “I’ve worked with lots of industries.” That answer is fluff.

Verify these points:

- Healthcare: Familiarity with the reporting discipline and documentation standards a practice needs.

- Construction: Ability to support job costing, payroll-related recordkeeping, and project-based reporting.

- Non-profit: Comfort with audit-ready books, grant tracking, and board-friendly financial reporting.

- Software fit: Real experience in the tools your organization already uses.

- Tax-readiness: A habit of keeping records organized so tax prep and year-end work do not become a scramble.

The closer your industry is to regulation, grant oversight, or project accounting, the less room you have for a generalist.

Onboarding Your New Partner for Long-Term Success

Hiring the right person is only half the job. A strong bookkeeper can still fail if you onboard them badly.

Owners often assume the new hire will “figure it out.” That is how books stay messy for another year.

The better approach is simple. Give clear access, define the workflow, set expectations, and decide what success looks like before the first month closes.

The labor market gives you options, and the economics often favor firm support. The average salary for a bookkeeper is $49,210 per year ($23.66/hour), not including benefits, while small businesses can access QuickBooks-certified experts through a firm for $30 to $60 per hour, according to the U.S. Bureau of Labor Statistics occupational outlook for bookkeeping, accounting, and auditing clerks.

Start with secure access and clean boundaries

Give your bookkeeper access to the systems they need. Banking feeds, accounting software, payroll platform, merchant accounts, loan statements, and document storage all matter.

Use secure, appropriate permissions. Not everyone needs full authority in every system. A clean access setup protects your business and avoids confusion later.

Build a monthly workflow

You need a repeatable routine, not random requests by email.

Set a document cadence for receipts, invoices, payroll reports, loan updates, and owner questions. Decide when month-end closes, when reports are delivered, and when review meetings happen.

A basic monthly workflow should cover:

- Transaction capture: Bank feeds, card activity, bills, deposits.

- Reconciliation: Bank and credit card accounts reviewed and matched.

- Review: Unusual items flagged and clarified.

- Reporting: Profit and Loss, Balance Sheet, and discussion of key changes.

- Tax-readiness: Sales tax, payroll support, and year-end documentation kept current.

Define what good work looks like

A lot of bookkeeping relationships go bad because the owner never defined success.

Do you want reports by a certain day each month? Do you want questions bundled weekly instead of daily interruptions? Do you want payroll coordination handled in a specific way? Say it up front.

Best practice: Good bookkeeping is measurable. Reports arrive on time, reconciliations are complete, open questions are tracked, and the owner understands the numbers.

Use onboarding to prepare for tax season

This matters more than most owners realize.

Tax prep gets expensive when the books are late, inconsistent, or full of uncategorized activity. If you hire a bookkeeper and still hand your tax preparer a mess, you did not solve the problem. You outsourced it.

A good onboarding process should identify how transactions are categorized, how owner draws or distributions are handled, how payroll entries flow into the books, and how year-end documents will be maintained. This is also where changing tax rules and filing requirements should be accounted for in your reporting routine.

Add fractional CFO guidance before you think you need it

Many owners wait until cash is tight or growth is chaotic before they ask for advisory help. That is backwards.

If your business is growing, adding locations, taking on new contracts, hiring heavily, or managing tight margins, fractional CFO support can turn bookkeeping from recordkeeping into decision support. That means better visibility into cash flow, cleaner planning, and someone who can explain the story behind the numbers.

Not every company needs a full-time CFO. Plenty need a smart financial guide.

The handoff should feel organized, not heroic

If your new bookkeeping partner needs to chase every login, ask repeatedly for the same documents, and rebuild your chart of accounts from scratch without context, you are making the engagement harder than it needs to be.

A better onboarding experience includes a checklist, a clear first-close timeline, and someone driving the process. If you want to see what a cleaner transition looks like, review this accounting client onboarding process.

My final advice

Do not hire for the cheapest hourly rate. Hire for reliability, judgment, and fit with your business.

Do not confuse software with expertise. QuickBooks is a tool. It does not supervise itself.

Do not wait until the books are a disaster. By then, you are paying for cleanup, not just bookkeeping.

If you want stable reporting, fewer tax-time surprises, stronger compliance, and financial guidance that helps you run the business, hire a bookkeeping partner who can grow with you. For a lot of Florida businesses, that means choosing a team that can handle bookkeeping, taxes, payroll coordination, audits, and fractional CFO support under one roof.

If your books are behind, your reports are unreliable, or you need a bookkeeping partner who understands healthcare, construction, or non-profit accounting in Northeast Florida, talk to Bookkeeping and Accounting of Florida Inc.. Their Jacksonville-based CPA team helps businesses stay compliant, clean up financials, manage tax changes, and add fractional CFO guidance without full-time overhead.