Sales are up. The bank balance says otherwise. Payroll hits, sales tax is due, vendors want to get paid, and somehow a “busy” month still feels skinny.

That is the gross margin problem in plain English.

A lot of owners in Jacksonville and across Northeast Florida think they have a revenue problem. Most of the time, they have a margin visibility problem. They are selling plenty. They are not keeping enough from what they sell.

If you want to know how to improve gross margin, stop staring at top-line revenue and start asking a tougher question. What does each dollar of sales leave behind after the direct cost of delivering the work? If you do not know that answer by service line, project, job, or client type, you are driving with a fogged-up windshield.

Real bookkeeping, clean QuickBooks files, tax compliance, and fractional CFO guidance stop being “nice to have” and start being mandatory. Especially now, with tax law changes, reporting requirements, payroll rules, and industry-specific compliance issues getting more complicated, bad numbers are not just annoying. They are expensive.

Why Your Profits Are Not Matching Your Sales

I see the same story all the time.

A contractor lands more work than last year. A medical practice is booked solid. A nonprofit wins another grant and adds activity. Revenue looks respectable. The owner assumes profit should follow. Then they open the financials and feel punched in the throat.

The problem is usually not effort. It is math.

Revenue is vanity until margin proves the work is worth doing

Gross profit is the dollars left after direct costs. Gross margin is that amount expressed as a percentage of revenue. One is the pile of money left. The other tells you how efficient the business is at creating that pile.

That distinction matters.

A company can post strong sales and still bleed cash because direct labor, software, subcontractors, supplies, rework, overtime, or poor pricing eat the value before overhead even enters the room. Then the owner blames taxes, payroll, or “the economy,” when the leak started much earlier.

If your books cannot tell you which jobs, services, or clients make money, then your business is not being managed. It is being guessed at.

Service businesses get this wrong more than product businesses

Retail and manufacturing owners usually expect to track costs per item. Service business owners often do not. That is a mistake.

In healthcare, the leak may be labor that is not tied cleanly to patient billing cycles. In construction, it is often project overhead that sits in the wrong bucket until the job closes and everyone wonders where the margin went. In nonprofits, it can be compliance-heavy work and audit prep that consume staff time without clean allocation.

The ugly truth is simple. Many businesses are not under-earning because they are lazy. They are more willing to look directly at the ugly parts of the business and act on them.

Bad bookkeeping makes gross margin impossible to trust

I do not care how polished your dashboard is. If your chart of accounts is sloppy, payroll is misclassified, job costs are inconsistent, and QuickBooks is treated like a junk drawer, the gross margin number is fiction.

That fiction causes bad decisions:

- You keep low-margin work because it “feels busy.”

- You underprice profitable work because you do not know what clients value.

- You miss compliance risks because messy books hide payroll, tax, and reporting issues.

- You delay action because the reports never feel solid enough to trust.

Owners do not need more theory. They need clean records, blunt analysis, and decisions tied to real numbers. Once you have that, improving margin stops being mysterious.

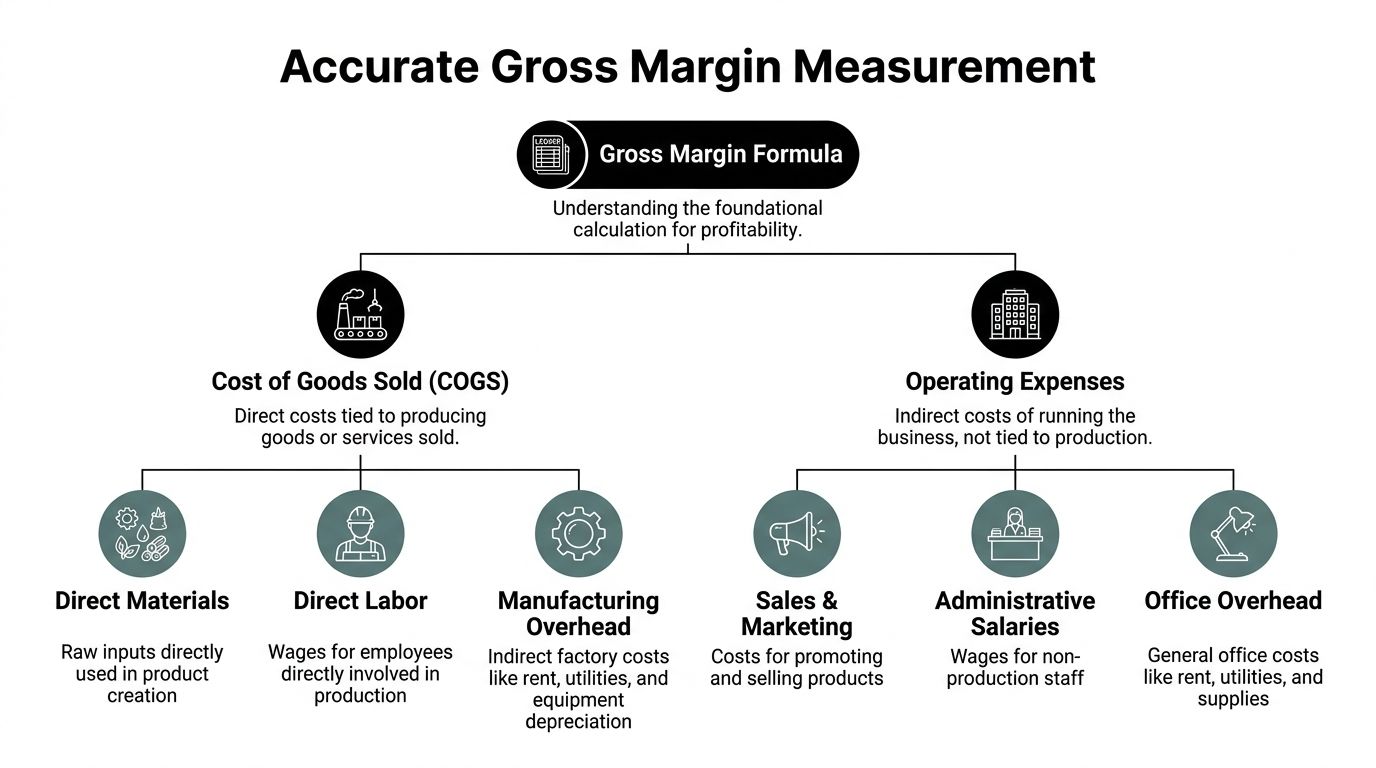

First You Must Measure Your Margin Accurately

Before you fix gross margin, you have to measure it without lying to yourself.

That means using a real formula, feeding it clean data, and putting the right costs in the right places. Not “close enough.” Not “my bookkeeper thinks so.” Accurate.

Start with the formula and then fix the inputs

The basic formula is simple:

Gross Margin = (Revenue – COGS) / Revenue

The hard part is not the formula. The hard part is getting COGS, or cost of goods sold, right.

For service businesses, that usually includes direct labor and software tied to delivery. The Gross Margin Bridge Analysis method lays this out clearly: collect financial data from QuickBooks, calculate the baseline margin, identify price, cost, volume, and mix variances, quantify the impact, and review trends quarterly. Firms using that method saw average margin gains of 8 to 12 percent within 12 months, and ignoring indirect costs can inflate margins by 10 to 20 percent according to this gross margin bridge analysis reference.

What belongs in COGS for a service business

Small businesses often trip over their own shoelaces here.

If you run an accounting firm, medical practice, construction company, or nonprofit support operation, COGS is not just “materials.” It usually includes the direct cost to deliver the work.

That can include:

- Direct labor: Billable staff time, technician wages, project labor, clinicians tied to revenue-producing services.

- Delivery software: Platforms and licenses used directly to perform client work.

- Travel tied to delivery: When it is directly connected to the service performed.

- Project-specific subcontractors: Especially in construction and specialized professional services.

What does not belong there? Usually admin salaries, general office overhead, broad marketing spend, and other costs of running the business that are not directly tied to delivering what was sold.

QuickBooks setup matters more than owners want to admit

A sloppy QuickBooks file creates fake margins. If labor is posted inconsistently, subcontractors are mixed with overhead, and software gets dumped into random expense categories, your margin report is dead on arrival.

If you want a practical walkthrough of cost classification, this guide on https://www.bookkeepingandaccountinginc.com/how-to-calculate-cost-of-goods-sold/ is useful because it forces the basic question most owners avoid: what did it cost to deliver the thing you sold?

A clean setup should let you slice margin by:

- Service line

- Project or job

- Client type

- Location or department

- Month and quarter

That is how you stop looking at one blended number and start seeing where the problem sits.

A simple example without nonsense

Suppose a business sells a service and records revenue. To calculate gross margin correctly, it subtracts only the direct delivery costs tied to that service. If the books dump unrelated admin costs into COGS, the margin looks worse than it is. If direct labor is left out, the margin looks better than it is.

Both mistakes are dangerous.

One makes you kill good work. The other makes you keep bad work.

Good margin work gets abandoned when costs are overstated. Bad margin work gets celebrated when costs are understated.

Use a bridge analysis, not a gut feeling

A Gross Margin Bridge Analysis is just a structured way to explain what changed.

You compare one period to another and isolate the impact of:

- Price

- Cost

- Volume

- Mix

That approach is far more useful than asking, “Why does profit feel off?” It tells you whether the issue came from lower pricing, higher labor cost, a shift toward weaker services, or a volume change that masked a margin problem.

If your team wants better reporting discipline, a good financial statement analysis tool can help organize the review process. But no tool rescues bad bookkeeping. The file still has to be right.

Tax law changes make clean books more important

This part gets ignored until it hurts.

When tax law changes affect payroll treatment, deductions, reporting, or industry-specific compliance, weak bookkeeping creates two problems at once. First, you misread gross margin. Second, you increase the chance of filing errors, missed deadlines, and ugly clean-up work later.

That is why owners need more than data entry. They need accounting that keeps the books clean enough to manage profitability and compliant enough to survive tax season without aspirin and regret.

The Four Levers to Immediately Boost Your Margin

Most owners attack margin the wrong way. They slash overhead first, freeze hiring, or try to “sell more” without checking whether the work is worth selling.

There are four levers that matter: pricing, input costs, sales mix, and gross margin conversion. Pull the right one and profit moves fast. Pull the wrong one and you create noise.

Pricing is the fastest lever

Most small businesses underuse pricing because they are scared of irritating customers. Fine. Stay cheap and stay tired.

A modest pricing change can have an outsized impact. According to Chortek, a 1% increase in selling prices, with costs held constant, can lift gross margin by up to 300 basis points, moving net margin from 7% to 10%, which is a 43% relative improvement in profitability. That is why pricing deserves executive attention, not guesswork at the front desk or in a rushed estimate template. The source is Chortek’s gross margin analysis.

Here is the practical version:

- Raise prices where clients buy outcomes, not hours. Advisory work, specialized reporting, compliance-heavy services, and difficult projects usually have room.

- Create tiers. Good, better, best pricing beats one flat package that undercharges your best clients.

- Stop grandfathering bad pricing forever. Loyalty is fine. Permanent underpricing is not.

- Review every estimate template. Construction bids, healthcare support packages, bookkeeping bundles, and audit scopes all drift over time.

If you want another perspective on the mechanics, this piece on how to improve profit margins is worth a read.

Owners usually have more pricing power than they think and less room for sloppy estimating than they realize.

Input costs need discipline, not whining

Some owners treat direct costs like weather. They complain, then they pay.

That is lazy management.

Direct costs should be reviewed line by line. If a software stack crept upward, renegotiate or consolidate. If subcontractor rates changed, your pricing and job costing must change too. If direct labor is chewing through margin, the answer might be training, scheduling, scope control, or staffing mix.

Look at these common offenders:

| Margin leak | What to do about it |

|---|---|

| Labor overruns | Tighten scope, approve overtime, review hours by client or job |

| Software sprawl | Eliminate duplicate tools, renegotiate licenses |

| Material waste | Improve purchasing controls and job estimates |

| Subcontractor creep | Tie vendor costs to jobs and review bid assumptions |

The point is not “cut costs everywhere.” The point is to cut the costs that do not improve delivery.

Sales mix decides whether growth helps or hurts

Not all revenue is good revenue.

A business can grow and become less profitable if it sells more low-margin work. This happens constantly in service firms. Basic payroll, entry-level bookkeeping, commodity admin work, and loosely scoped support often chew up time while premium services carry the business.

Owners need to know which services contribute margin.

A healthier mix usually comes from decisions like:

- Reducing low-margin volume

- Bundling high-value services

- Specializing in work clients cannot easily price-shop

- Training staff to upsell from compliance work into advisory work

Many businesses realize they do not need more customers here. They need better customers and a better service mix.

Gross margin conversion is the hidden lever

This often gets missed because it sounds technical. It is not.

Gross margin conversion means how efficiently your inputs turn into billable output. In a service business, that means hours, tools, and workflow discipline. In a construction business, it means labor, material use, and job execution. In healthcare, it includes process flow tied to billable services.

A business with decent pricing can still have weak gross margin because the work is delivered inefficiently.

Conversion problems show up as:

- Time not captured

- Rework

- Manual entry

- Excess approvals

- Overtime caused by poor scheduling

- Scope drift nobody billed for

- Duplicate software tasks

- Staff doing work below or above the right skill level

These are not abstract issues. They are profit leaks.

Pull the levers in the right order

If I were cleaning this up in practice, I would usually do it in this order:

- Measure margin correctly

- Fix obvious pricing errors

- Track and clean direct costs

- Cull or redesign low-margin services

- Improve operational conversion

That sequence matters. If your books are wrong, your pricing review is shaky. If your service mix is poor, cutting office expenses will not save you. If your workflow is a mess, extra sales may just multiply the mess.

The owners who improve margin fastest are not necessarily smarter. They are more willing to look directly at the ugly parts of the business and act on them.

Unlocking Hidden Profit With a Fractional CFO

A lot of businesses do not need a full-time CFO. They do need someone who knows where the money is leaking and is willing to say it out loud.

That is the value of a fractional CFO.

A decent bookkeeper records history. A strong controller keeps the machine moving. A fractional CFO studies the numbers, challenges assumptions, and shows the owner which services, clients, and processes deserve more attention and which ones deserve the exit door.

Mix analysis shows what deserves your time

Most owners think they know their best work. A fractional CFO checks the file and proves it.

In service businesses, the biggest hidden opportunity is often service mix. One line of work looks attractive because it sells easily. Another line produces more gross profit with fewer headaches. Without a proper review, owners keep feeding the wrong part of the business.

That analysis looks at:

- Revenue by service line

- Direct labor by service line

- Software and support costs tied to delivery

- Margin by client type

- Scope creep patterns

- Write-offs and unbilled time

A fractional CFO uses that information to make hard recommendations. Keep this. Raise that. Bundle this. Fire that offering. Tighten scope here. Move senior staff off low-value tasks.

If you are not sure what that role includes, this overview of https://www.bookkeepingandaccountinginc.com/what-is-fractional-cfo-services/ gives a practical description.

Conversion is where hidden profit lives

This is the part owners usually miss because the business is “busy.”

Busy is not the same as efficient.

CFO Secrets described a coffee shop case where gross margin improved from 62% to 71% without changing sales prices, input costs, or sales mix. The improvement came from operational tweaks that reduced waste and optimized labor, which is exactly why gross margin conversion matters so much in service businesses too. That case is discussed in this CFO Secrets article on improving gross margin.

The lesson is broader than coffee.

In a bookkeeping firm, conversion losses may come from manual payroll entries, duplicated data input, or review layers that should not exist. In construction, it can be field labor that is not coded to the right phase or overtime that never gets traced back to project execution. In healthcare, staff time can drift away from billable activity because procedure-level cost tracking is weak.

If your team is working hard but margins are not improving, the problem is often not demand. It is conversion.

A short video can help frame that bigger financial picture:

A fractional CFO connects operations to compliance

This part matters in Florida because businesses do not just operate. They report, file, document, allocate, substantiate, and answer questions.

That gets harder when tax law changes affect deductions, payroll handling, documentation standards, or industry-specific compliance. A fractional CFO does not replace your tax preparer or CPA. The role strengthens decision-making before year-end so the books support cleaner tax work and fewer ugly surprises.

That means:

- spotting classification issues before tax season,

- identifying labor coding problems that distort margin and payroll reporting,

- cleaning up software and direct cost treatment,

- and building reporting that management can use.

Owners need guidance, not another spreadsheet

Plenty of businesses have reports. They do not have answers.

A fractional CFO provides the missing interpretation. Not “your margin went down.” That is obvious. The useful advice is “your margin went down because your mix shifted, your labor conversion slipped, and your highest-value service is underpriced.”

That kind of guidance changes decisions quickly.

If you want to know how to improve gross margin in a service-based business, profit usually sits here. Not in another generic budgeting app. In disciplined analysis of mix, conversion, and the ugly little habits that chip away at profit every week.

Gross Margin Strategies for Florida's Core Industries

Generic gross margin advice is built for retailers and manufacturers. That is fine if you sell inventory. It is not enough if you run a clinic, a construction company, or a nonprofit in Florida.

These sectors carry heavy labor, compliance, and reporting burdens. If you treat them like a generic small business, you will misread margin and make bad decisions.

Healthcare businesses need procedure-level cost visibility

In healthcare, revenue can look strong while margin slips because labor is not tied tightly enough to patient billing cycles.

Specialized job-costing of labor to patient billing can improve margins by 5% to 15% in healthcare settings, according to the industry-specific guidance summarized by Grow Good Roots in this gross margin article. The point is not fancy jargon. It is getting staff time, support costs, and delivery systems aligned with what is billable.

A healthcare practice should be asking:

- Which services are profitable after direct labor?

- Which support tasks belong to delivery and which belong to admin?

- Are compliance-heavy activities being priced properly?

- Are coding, billing, and staffing decisions helping margin or sabotaging it?

Recent tax law changes and healthcare regulations only make this more important. If costs tied to compliance rise and the books do not separate them clearly, margin gets blurry fast.

Construction firms live or die by job costing

Construction companies in Jacksonville and across Northeast Florida often have one giant problem. They think they know job profitability because they know the contract value.

That is not job costing. That is optimism.

For construction, forensic auditing of project-specific overhead can prevent 10% to 20% margin erosion on a job, based on the same industry guidance linked above. If payroll, subcontractors, materials, fuel, equipment use, and phase-specific overhead are not tied correctly to each project, the business will underquote work and congratulate itself all the way to a thin bank balance.

Construction owners should focus on:

- labor coding by job and phase,

- subcontractor controls,

- change order discipline,

- overhead allocation that reflects reality,

- and project reviews before the damage becomes permanent.

The firms that win long term are not just good builders. They are good measurers.

Nonprofits need compliant allocation and sharper service choices

Nonprofits have a different challenge. Their financial reporting has to support funders, boards, audits, and internal decisions at the same time.

That means gross margin thinking has to respect restricted funds, grant-driven activity, and compliance-heavy work. Sloppy allocation creates two risks. It weakens management insight, and it creates reporting trouble.

One overlooked strategy is specialization. Grow Good Roots notes that specializing in high-value services like forensic audits can produce a 25% margin uplift. That same logic applies broadly. Nonprofits and the firms serving them do better when they stop spreading effort across low-value tasks and focus on work that justifies the labor and compliance burden.

In nonprofits, “busy” can hide waste better than almost anywhere else because mission-driven teams often tolerate weak economics for too long.

Florida businesses need local, not generic, guidance

National advice often falls short here.

Florida businesses face state and local filing demands, industry-specific regulation, payroll issues, and changing tax requirements that can distort margin if nobody is watching the books carefully. The answer is not more generic accounting content. The answer is bookkeeping and CFO-level analysis built around the way healthcare, construction, and nonprofit organizations operate here.

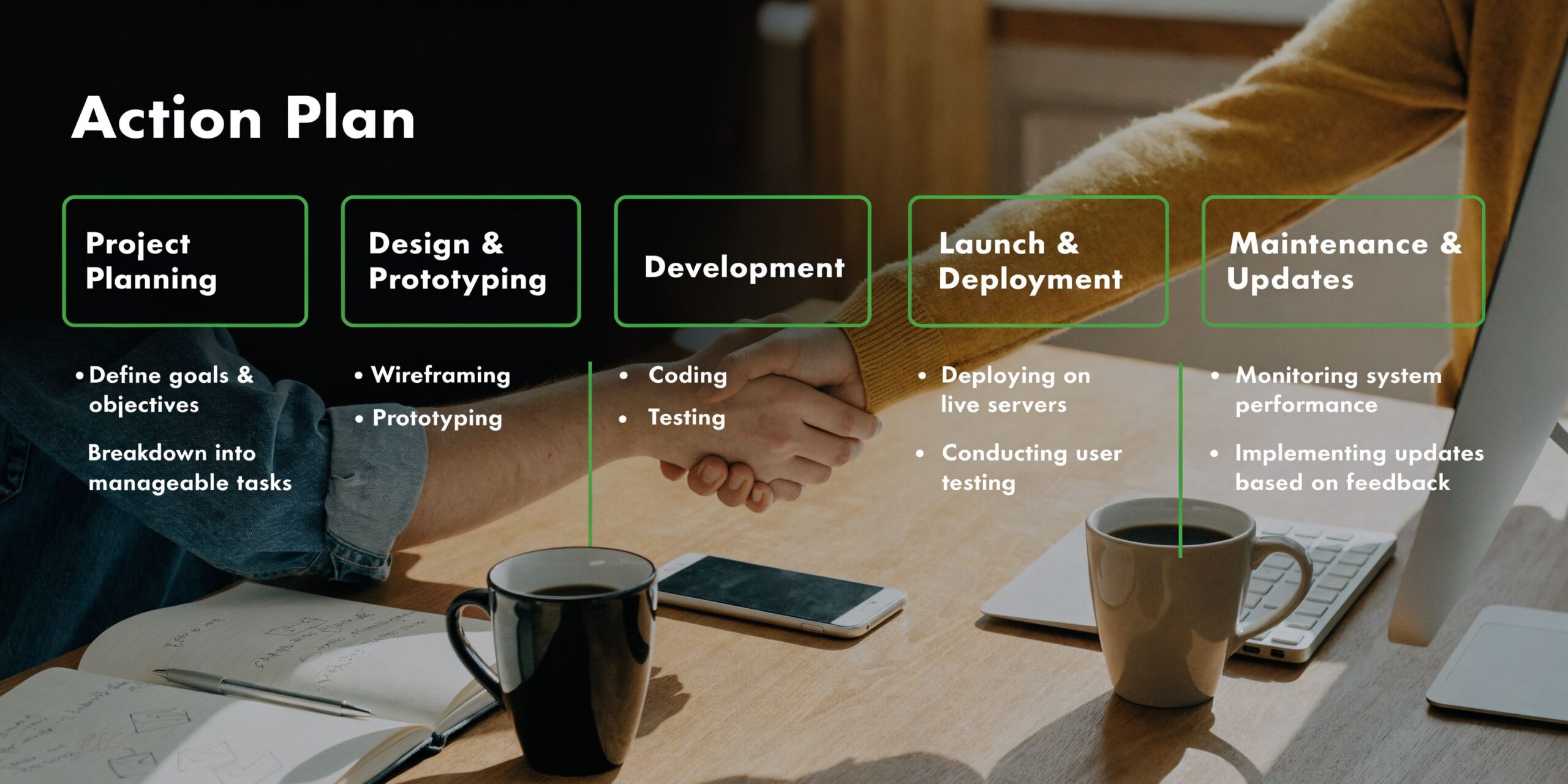

Your 90-Day Margin Improvement Action Plan

If gross margin is weak, do not spend six months talking about it. Fix it.

A solid 90-day plan gives you enough time to clean the books, identify the leaks, and make decisions without turning the project into another half-finished management initiative.

Days 1 through 30 clean up the numbers

Do not start with pricing. Start with truth.

Review the QuickBooks file, chart of accounts, payroll mapping, job or service coding, and cost classifications. Make sure direct labor, software, subcontractors, and service-delivery expenses are treated consistently.

Businesses often lose margin after the sale through hidden conversion losses. American Express notes that production inefficiencies can erode 10% to 30% of margins post-sale, and unoptimized QuickBooks workflows can create 15% waste in time-tracking. The same source says a professional 90-day audit can reveal these losses and improve margins by over 300 basis points, which is why cleanup work should come first. The source is American Express on improving gross profit margin.

Use this first month to answer basic questions:

- What is our real gross margin by service or job?

- Where are direct costs being misclassified?

- What work is being delivered without proper time or cost capture?

- Are tax, payroll, and compliance records clean enough to trust?

This is also the right time to tighten your cash planning. A reliable forecast helps you act on margin problems before they turn into a cash squeeze, and this resource on https://www.bookkeepingandaccountinginc.com/how-to-forecast-cash-flow/ is a good place to start.

Days 31 through 60 pull the right levers

Once the books are reliable, act fast.

Raise prices where the business is clearly undercharging. Trim or redesign low-margin services. Review direct software and vendor costs. Tighten approvals around overtime, write-downs, and scope creep. If you are in construction, clean up job costing and phase coding. If you are in healthcare, separate billable delivery work from support functions more clearly. If you are in a nonprofit, fix allocation methods so management reporting and compliance reporting tell the same story.

This month is about decisions, not debate.

A short checklist helps:

- Update pricing and estimates

- Review every direct cost category

- Flag low-margin clients or service lines

- Automate repetitive workflow where practical

- Assign accountability for margin by department, project, or service line

Most margin improvement does not require heroics. It requires owners to stop tolerating avoidable waste.

Days 61 through 90 review and refine

By the third month, you should not be guessing whether the changes worked.

Pull fresh reports and compare them to the baseline. Look at margin by client, service line, project, and staff mix. Check whether process changes improved delivery efficiency. Review whether tax compliance, payroll coding, and documentation standards improved along with profitability. Many owners quit too early. They clean up the books, make one price change, and then drift back into old habits.

Do not do that.

Build a recurring review rhythm around:

- monthly gross margin by line,

- labor efficiency,

- write-offs and rework,

- tax and compliance deadlines,

- and cash flow forecasting.

Tax law changes do not wait for businesses to “get around to it.” Compliance mistakes, messy books, and poor margin discipline tend to travel together. The business that wants better profit and fewer surprises needs one system, not isolated fixes.

A good 90-day margin improvement plan should leave you with cleaner books, better pricing discipline, clearer service mix decisions, tighter operations, and stronger compliance footing. That is how you improve gross margin without creating another mess somewhere else.

If your sales look healthy but profit still feels thin, it is time for a hard look at the numbers. Bookkeeping and Accounting of Florida Inc. helps Jacksonville and Northeast Florida businesses clean up their books, stay compliant with tax and reporting requirements, and use fractional CFO guidance to find hidden profit in pricing, service mix, and operations. If you want clear financials, practical advice, and less guesswork, schedule a conversation.