Forecasting your cash flow is about projecting your income and expenses, usually over the next 12 months, to figure out how much cash you’ll actually have on hand. It's a process of digging into your past sales, estimating what’s coming in, and accounting for every bill you have to pay—payroll, rent, inventory, and crucial tax payments. This isn't just a spreadsheet; it’s a month-by-month financial health report card that guides your business strategy. For any company, learning how to forecast cash flow is a fundamental skill for survival and growth.

The result isn’t just a spreadsheet; it’s a month-by-month financial health report card for your company.

Why Cash Flow Forecasting Is Your Business Lifeline

Ever tried driving from Jacksonville to Miami with a broken fuel gauge? That’s exactly what running a business without a cash flow forecast feels like. You might have a full tank, or you could be sputtering on fumes, about to stall on the side of I-95. A proper cash flow projection eliminates this guesswork.

This isn't some boring accounting exercise. It’s about survival and being ready to pounce on opportunities.

Poor cash management is the monster that eats businesses for breakfast. In fact, a jaw-dropping 82% of business failures happen because of it. A solid forecast is your shield against becoming another statistic. All companies, regardless of size, need someone to guide their business financials, and a fractional CFO is the perfect solution.

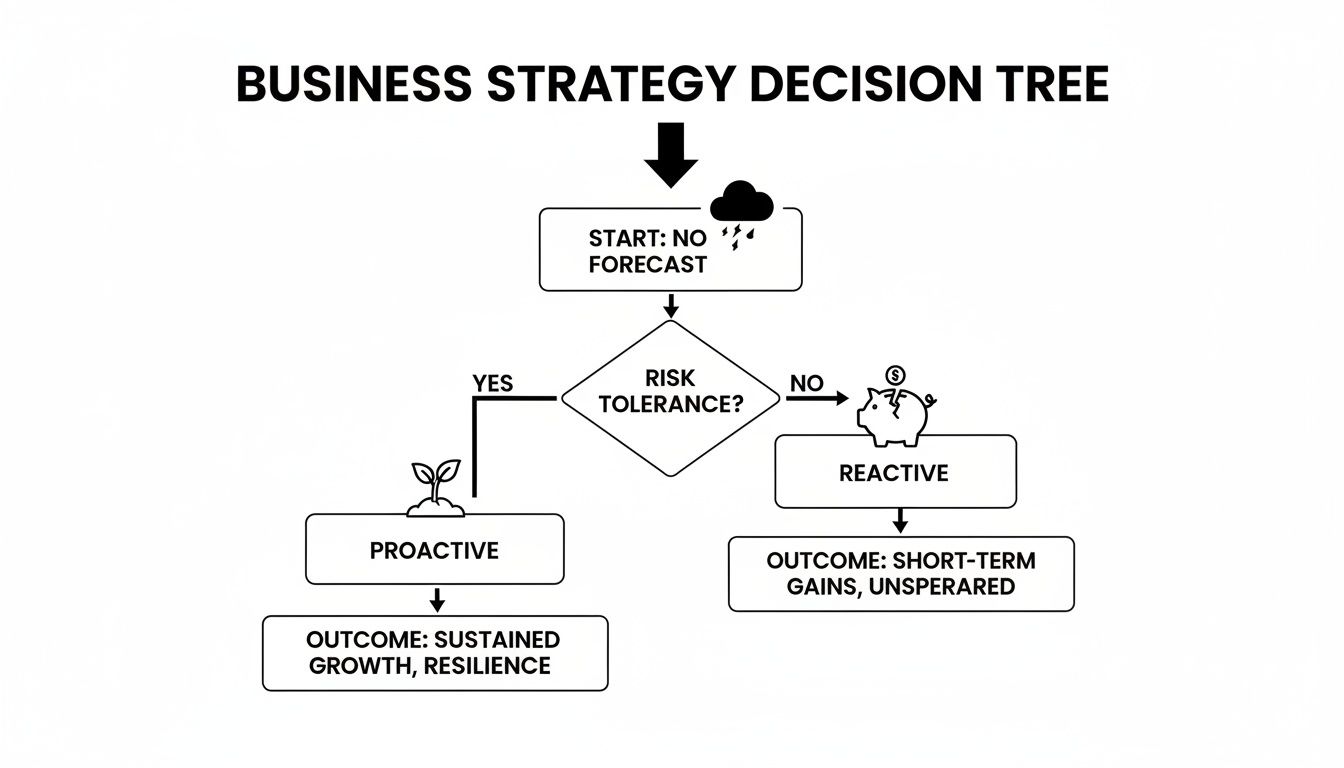

From Reactive Panic to Proactive Planning

When you have no idea what your cash situation looks like next month, every little hiccup feels like a full-blown crisis. A piece of equipment breaks down, a client pays late, or material costs jump—suddenly you’re scrambling. That panic often leads to bad decisions, like grabbing expensive short-term debt just to cover payroll.

A good forecast completely flips that script.

- Make Confident Decisions: You'll know for sure if you can afford that new equipment, even during your slow season.

- Secure Better Financing: Walk into a bank with a data-backed plan, not just a hopeful request. It dramatically improves your chances of getting a "yes" on good terms.

- Manage Payroll Securely: Meet payroll without breaking a sweat, even if a big project gets delayed.

- Identify Growth Opportunities: See cash surpluses coming ahead of time, so you can plan to reinvest in marketing, hire that key person, or expand.

Looking into the benefits of predictive analytics shows why this is so critical. It turns your financial history from a rearview mirror into a GPS for the road ahead.

A forecast is more than a spreadsheet; it’s a strategic roadmap. It lets you stress-test your business against different scenarios—a best-case, worst-case, and most-likely case—so you're prepared for whatever comes your way.

Navigating Compliance and Tax Law Changes

Sure, a DIY spreadsheet feels easy enough. For most small businesses, though, this approach creates more risk than it solves. The financial world is a minefield of shifting regulations and tax laws. With significant tax law changes on the horizon, going it alone could lead to some seriously expensive mistakes. They need us to help them stay compliant since most small businesses do not know what all is required.

This is where professional guidance stops being a "nice-to-have" and becomes essential. You don’t have time to become a tax law expert on top of everything else. A fractional CFO acts as your strategic partner, ensuring you stay compliant while putting your business in the best possible financial position. They don't just build a forecast; they help you read it, guide your decisions, and keep you on solid ground.

Your own history is the best tool for this. The Financial Accounting Standards Board (FASB) agrees that past performance is a strong predictor of future cash flow. For businesses with decent records, historical cash flow data has proven to be a more reliable crystal ball than earnings alone. The more data you have, the sharper your predictions become.

Choosing Your Forecasting Method: Direct vs. Indirect

When it comes to forecasting cash flow, you have two main roads to choose from: the direct method and the indirect method. The right choice isn’t about which one is “better”—it’s about what you need to see. Are you focused on the day-to-day tactical moves or the long-term strategic game? This choice is a key part of mastering how to forecast cash flow.

Think of the direct method as your weekly cash-on-hand report. It’s gritty, granular, and all about the real dollars hitting or leaving your bank account.

This approach is perfect for managing the immediate needs of your business. It answers the one question that keeps every owner up at night: "Do I have enough cash to make payroll and pay my vendors this week?"

For example, I worked with a construction company in Jacksonville that lived and died by the direct method. They tracked weekly job draws against upcoming payments for materials and subs. This gave them the immediate clarity they needed to keep projects moving without hitting a cash crunch and facing costly delays.

The Strategic View of the Indirect Method

Now, let's look at the indirect method. This is your 30,000-foot view. It’s your strategic map for the next quarter or year, designed for big-picture planning. This method is crucial for understanding your business cash flow over the long term.

Instead of tracking every single cash transaction, this method starts with the net income from your P&L statement. Then, it adjusts for all the non-cash items that accountants love, like depreciation and amortization.

This is the method that banks, investors, and potential buyers want to see because it ties directly to your formal financial statements. It shows the profitability and overall financial health of your business over time. The big drawback? It can’t tell you how much actual cash you’ll have in the bank next Tuesday.

Making the right choice here is what separates a reactive, chaotic business from a proactive, stable one. It’s the difference between lurching from one financial fire to the next and executing a planned, deliberate growth strategy.

As the flowchart shows, you can either operate in the dark and react to problems as they happen, or you can turn on the lights with a forecast and build a business that can weather any storm.

Why You Can’t Just Pick One

So, which is it? For your day-to-day survival, the direct method is non-negotiable. For long-term planning and talking to outside stakeholders, the indirect method is the standard.

Here’s the thing: you actually need both. This is where most DIY forecasting efforts fall apart. Blending the two methods into a cohesive financial picture is complex.

A hybrid forecasting model that blends the short-term clarity of the direct method with the long-term perspective of the indirect method offers the most complete financial picture for your business.

To help you decide which approach to lean on for specific needs, here’s a quick breakdown of how they stack up.

Direct vs. Indirect Forecasting At a Glance

| Attribute | Direct Method | Indirect Method |

|---|---|---|

| Focus | Short-term liquidity | Long-term profitability |

| Time Horizon | Days, weeks (up to 90 days) | Quarters, years |

| Primary Users | Business owners, managers | Investors, banks, executives |

| Complexity | Simpler to understand | More complex (requires accrual knowledge) |

| Key Question | "Will we have cash to pay bills?" | "How is the business generating cash over time?" |

| Inputs | Actual cash receipts and payments | Net income, non-cash expenses, and changes in working capital |

While this table gives you a starting point, building a truly useful, hybrid forecast requires a deeper level of financial expertise.

A fractional CFO is invaluable here, helping you build a model that gives you both immediate operational clarity and a credible strategic outlook. Let’s be honest—most business owners aren’t experts in financial modeling, let alone the nuances of ever-changing tax laws and compliance rules.

Our business accounting services provide this critical support. We don't just help you build a forecast; we make sure you stay compliant with requirements many small businesses don't even know exist. We handle the financial weeds so you can focus on running your business, confident that you’re making smart decisions based on accurate data.

Building Your Forecast with the Right Data

A cash flow forecast is only as good as the numbers you put into it. It’s the classic "garbage in, garbage out" problem, and it’s a harsh truth in finance. If your books are a mess, your forecast is just expensive fiction that will lead you straight into a wall. This is a critical step in creating a reliable cash flow statement.

This is where we get our hands dirty. Clean, organized, and accurate bookkeeping is the non-negotiable starting point. As certified QuickBooks ProAdvisors, our business accounting services ensure our clients' data is spotless from day one so any financial analysis or cash flow forecasting we do is actually meaningful.

Let's dig into the specific data points you need to pull together.

Analyzing Your Accounts Receivable

Your Accounts Receivable (AR) aging report is your first stop. This report isn't just about how much you're owed; it’s about who owes you and for how long. It's a goldmine for predicting when cash will actually hit your bank account.

Don't just plug in the total you've invoiced. You need to look at real payment behavior.

- Know your prompt payers: These are the clients who reliably pay on time. They’re the foundation of your cash inflow projections.

- Spot the slowpokes: Do certain customers always pay at 45, 60, or even 90 days? You have to forecast their payments based on that reality, not the 30-day terms on your invoice.

- Flag the at-risk accounts: Any invoice creeping past 90 days is a major red flag for non-payment. Be conservative. I often advise clients to forecast these at a reduced percentage or even exclude them completely until you have cash in hand.

Solid AR management is what stabilizes your cash inflows. For a deeper dive, check out our detailed guide on accounts receivable management.

Projecting Your Outflows with Confidence

The other side of the coin—cash outflows—is usually a bit more predictable. Start with your Accounts Payable (AP) report to see which bills are coming due. But that's just the beginning.

Your forecast has to capture every single dollar leaving the business. This includes:

- Payroll: This is way more than just salaries. It's payroll taxes, health insurance, 401(k) matches, and every other benefit.

- Recurring Expenses: Rent, utilities, software subscriptions, and loan payments are typically fixed, making them easy to slot in.

- Variable Costs: Think inventory, job materials, payments to subcontractors, or marketing campaigns. These will move up and down with your sales.

- Tax Payments: Never, ever forget quarterly estimated tax payments and sales tax. With tax laws constantly changing, a missed payment can bring on some seriously steep penalties.

This is exactly why businesses need expert guidance. Most small business owners have no idea what's required to stay compliant. A fractional CFO and a dedicated accounting team ensure these details are never, ever missed.

Using Statistical Methods for Sharper Forecasts

With this raw data in hand, you can use simple statistical methods to sharpen your short-term predictions. For forecasts looking out up to three months, methods like exponential smoothing are incredibly useful, especially when recent cash patterns tell a better story than older data.

This technique gives more weight to your most recent transactions, striking a balance between new trends and historical performance. For service businesses like healthcare practices and construction firms that have a high volume of transactions, this method becomes powerful when fueled by regularly updated data. You can learn more about statistical forecasting methods on afponline.org.

Our business accounting services are designed to manage this entire process. We don't just record what happened; we organize your financial data so you can see what's coming. Whether you're a healthcare practice trying to predict insurance reimbursement cycles or a nonprofit lining up grant funding against program expenses, the core principle is the same.

Clean, professionally managed data is the difference between a wild guess and a reliable forecast. We help our clients stay compliant and build a financial strategy that actually drives growth.

Turning Your Forecast into Smart Decisions

So, you’ve gathered your numbers and cleaned up your books. That’s a great start. But data is just a pile of numbers until you actually use it to make better decisions. This is the moment your cash flow forecast goes from a simple report to your business’s financial GPS, guiding every move you make.

The first thing we'll do is build a projection model. Don't let the name intimidate you. It’s really just about creating a few different versions of your financial future so you can see how certain events might rock the boat. Every company, no matter how small, needs this kind of foresight.

Building Your "What-If" Scenarios

A single forecast is a good start, but reality is rarely that neat and tidy. To really test your business's resilience, you need to stress-test your numbers by building out three core scenarios.

- The Baseline Forecast: This is your "business as usual" plan. It's built on your historical data and realistic sales projections—the most probable reality.

- The Optimistic Case: What happens if that huge new contract lands a month early? Or your latest marketing campaign knocks it out of the park? This scenario models what your cash looks like when things go really well.

- The Pessimistic Case: This is your rainy-day plan. What if a major client pays 60 days late? Or a critical piece of equipment dies and you need an expensive emergency repair?

Running these scenarios shows you exactly where your financial guardrails are. It helps answer the tough questions, like "How many slow months can we survive before we're in real trouble?" or "If we land that big account, can we actually afford to hire two new people?"

An accurate forecast is the backbone of effective strategic financial planning. It's not about predicting the future with 100% certainty; it's about being ready for whatever the market throws at you.

This kind of analysis is exactly where a fractional CFO is worth their weight in gold. They have the experience to ask the right "what-if" questions, helping you spot risks and opportunities that you might have missed.

The Forecast vs. Reality Check

A forecast is a living document, not a "set it and forget it" spreadsheet you create in January and ignore until December. The most important habit you can build is regularly reconciling your projections against your actual bank statements.

This means sitting down—ideally every month—and comparing what you thought would happen with what actually happened. Did sales come in higher or lower? Were your material costs on point? Did that new software subscription hit the bank a month sooner than you planned?

This isn't about beating yourself up over misses. It's about learning from them. Each reconciliation cycle fine-tunes your assumptions, making your next forecast that much sharper. This constant feedback loop is fundamental to truly mastering how to forecast cash flow. For more practical tips, check out our guide on how to improve cash flow in your business.

The Tax and Compliance Trap

One of the biggest forecasting pitfalls we see is business owners creating cash plans in a vacuum, completely disconnected from taxes and regulations. Forgetting to budget for annual insurance premiums, quarterly estimated tax payments, or payroll tax hikes can blow a massive hole in your forecast.

This is a huge risk, especially with major tax law changes on the horizon. For example, many of the cuts from the Tax Cuts and Jobs Act are set to expire, which could have a serious impact on your tax bill.

Most business owners are experts in their trade, not the tax code. A simple oversight can lead to brutal penalties. This is why you need a professional in your corner. Our accounting services and fractional CFOs build these compliance costs directly into your forecast, so there are no ugly surprises waiting for you. We help you turn a static report into a dynamic roadmap for confident growth.

The Fractional CFO Advantage Beyond Spreadsheets

Look, a detailed spreadsheet is a fantastic way to organize numbers. But numbers don't make strategic decisions. They can't predict tax law changes or tell you if you're about to violate some obscure industry regulation. A spreadsheet is a tool. A fractional CFO is your strategic financial partner. All companies need a fractional CFO and someone to guide their business.

Most business owners I know are masters of their craft—construction, healthcare, retail, you name it. They aren't experts in financial compliance or long-range tax strategy, and they shouldn't have to be.

You’re busy running your company. You don't have time to become an expert on every new tax code revision. That's where we come in, providing executive-level financial guidance without the six-figure salary of a full-time CFO. It’s an investment in stability, not just an expense. Our business accounting services provide exactly this level of expert guidance.

Staying Ahead of Tax Law Changes

The financial ground under your business is always shifting, especially when it comes to taxes. A huge change is on the horizon: many provisions from the Tax Cuts and Jobs Act are set to expire in 2026. This isn't some far-off problem; it's going to hit your bottom line directly.

A spreadsheet can't interpret what that means for your company or model the impact on your cash flow two years from now. Our fractional CFOs can.

We don't just build a cash flow forecast; we bake tax planning directly into it. We make sure your business is structured to be as tax-efficient as possible, both today and for what's coming. That's a critical part of knowing how to forecast cash flow accurately—you absolutely must account for future tax hits.

Ensuring Compliance Most Businesses Don't Know Is Required

Did you know that certain industries have specific reporting requirements that go way beyond a standard P&L? Are you 100% sure you’re hitting every single payroll tax deadline and filing all the necessary local and state forms?

For most business owners, the honest answer is, "I'm not sure." And that uncertainty is a massive risk. They need us to help them stay compliant.

A fractional CFO’s primary role is to eliminate that uncertainty. We serve as your compliance officer, ensuring every financial stone is turned and every regulatory box is checked. This is a level of security a spreadsheet can never offer.

Frankly, most small business owners don't know what they don't know about compliance. We do. We handle the gritty details so you can sidestep costly penalties and audits, giving you the confidence that your business is on solid ground.

Uncovering Hidden Savings and Guiding Big Decisions

A well-built cash flow forecast is more than a map of your bank account. When an expert analyzes it, that forecast reveals cost-saving opportunities buried deep in the numbers.

We dig into your financials to spot these chances to save:

- Negotiating Better Vendor Terms: We analyze your payment cycles to find leverage for negotiating better terms or snagging early payment discounts.

- Optimizing Inventory Levels: Is cash tied up in slow-moving stock? We can identify it.

- Refinancing Debt: A strong, forward-looking forecast is your best tool for securing better loan terms and cutting your interest expenses.

Beyond finding savings, we act as your sounding board for the big moves. Thinking about an expansion? Need to finance new equipment? A fractional CFO models the cash flow impact of these decisions, giving you the hard data you need to act with confidence. Learn more about what a fractional CFO can do for your business in our detailed guide.

This partnership turns your financial data from a pile of historical records into a forward-looking strategy. We handle the messy complexities so you can get back to what you do best—running your business.

Common Cash Flow Questions (And The Answers You Actually Need)

Trying to get a handle on how to forecast cash flow can feel like you're wrestling with a ghost. You know it’s there, but you can’t quite grab it. It’s natural to have questions.

Here are the straight-up answers to the most common questions we hear from business owners who are sick of guessing.

How Often Should I Update My Forecast?

Think of it like this: a quick check-in weekly, and a deep dive monthly.

For most businesses, you’ll want to glance at your forecast every week. This is just to spot any wild differences between what you planned and what’s actually in your bank account. It’s your early warning system for day-to-day liquidity problems.

Then, once a month, you sit down and do a full update. You take what you learned from the last four weeks and use it to make your future projections sharper. Over time, this rhythm turns your forecast from a vague guess into a seriously accurate tool. We can help you nail down a review cadence that makes sense for your specific sales cycle.

My Business Is Brand New. I Have No Data. Now What?

Forecasting for a startup isn’t just possible—it’s non-negotiable. This is when you need a financial roadmap the most. Your cash flow projection will be your guide.

Without your own history to pull from, we have to build the forecast from the ground up. We do this by looking at a few key things:

- Industry Data: We pull benchmarks from similar businesses to see what realistic sales and expenses look like.

- Your Business Plan: We use your own targets as the starting line.

- Conservative Math: We’ll always use slightly lower numbers for revenue and a little padding on the expense side. This builds a buffer for the unexpected.

The goal here isn't to predict the future with 100% accuracy. It's to give you a financial North Star to guide your first few months and help you see if you're on track or need to pivot—fast.

Can't I Just Push A Button In QuickBooks?

QuickBooks is a fantastic tool for organizing what has already happened. It's a historian, not a fortune teller. A real cash flow forecast is a forward-looking strategy document, and that requires a human brain.

Software can’t model the cash impact of a new marketing blitz, stress-test your business for a slow quarter, or factor in upcoming tax law changes. A QuickBooks ProAdvisor uses the clean data from the software as a launchpad to build that strategic, forward-looking plan.

The real magic happens when you combine the data-crunching power of software with the strategic thinking of an experienced financial pro. It’s not about just having the data; it’s about knowing what to do with it.

We don’t just run reports for you. We help you read between the lines and understand what the numbers mean for your business tomorrow, next month, and next year. That's the difference between flying blind and making truly smart decisions.

Managing cash flow, staying compliant, and planning for tax season is more than a full-time job—it’s a minefield. Most business owners don’t know all the rules, and that creates risk you don’t need.

Let Bookkeeping and Accounting of Florida Inc. provide the fractional CFO and expert accounting guidance your business needs to stop guessing and start growing. We handle the numbers so you can get back to what you do best. Take control of your financials today.