You're good at what you do. That's why the business grew.

But plenty of Jacksonville owners hit the same wall. Revenue is coming in, customers keep calling, payroll is now a real thing, and the books are sitting in QuickBooks half-finished, half-guessed, and half-ignored. Receipts are in email, on the truck seat, and in a desk drawer. Bank accounts are connected, but nothing is cleaned up. Tax deadlines feel like surprise attacks.

That's where bookkeeping for small business stops being “admin work” and starts becoming operational control. If your books are wrong, your pricing can be wrong. Your tax filings can be wrong. Your cash forecast can be fiction. A business can look busy and still be drifting.

I've seen this over and over. The owner knows roofing, therapy, home health, contracting, retail, or nonprofit operations cold. Then the financial side gets treated like a side project. That mistake gets expensive fast.

Your Business Is Thriving But Your Books Are A Mess

A lot of owners think messy books are a normal side effect of growth. They're not. They're a warning light.

The pattern usually looks the same. A company starts small. The owner handles estimates, sales, hiring, deliveries, and customer issues. Bookkeeping gets pushed to nights and weekends. Then it turns into catch-up work done from memory. That's when transactions get miscoded, bills get missed, and no one really knows what the business earned last month.

What the mess usually looks like

You might recognize a few of these:

- Receipts everywhere: Some are in a glove box, some are in text threads, some are gone.

- Unclear bank activity: Charges hit the account and nobody remembers what they were for.

- Late reconciliations: The books don't match the bank because nobody's tied them out.

- Tax anxiety: You're not sure what's due, what's already paid, or what your CPA will need.

- Blind decision-making: You hire, buy equipment, or take on debt without solid numbers.

That's not a bookkeeping problem alone. That's a management problem.

Bookkeeping is the control panel of the business. If the panel is dead, you're still flying, just blind.

There's a reason this field isn't some tiny niche. The global accounting services market was projected to reach $735.94 billion by 2025, and the U.S. had nearly 886,000 accounting firms, according to an industry roundup on accounting market size. Those numbers tell you something simple. Businesses don't treat accounting support as optional once things get real.

Busy is not the same as healthy

A packed schedule can fool you. Construction firms can stay slammed and still bleed cash because billing lags. Healthcare practices can look profitable while reimbursements drag and payroll keeps hitting. Nonprofits can have money in the bank that's restricted and not available for ordinary operations. Retailers can sell plenty and still not understand margins by product line.

That's why bookkeeping for small business matters so much. Good books tell you what happened. Clean books tell you what needs attention. Timely books let you act before the damage spreads.

If your current system depends on memory, spare time, and hope, it's already broken.

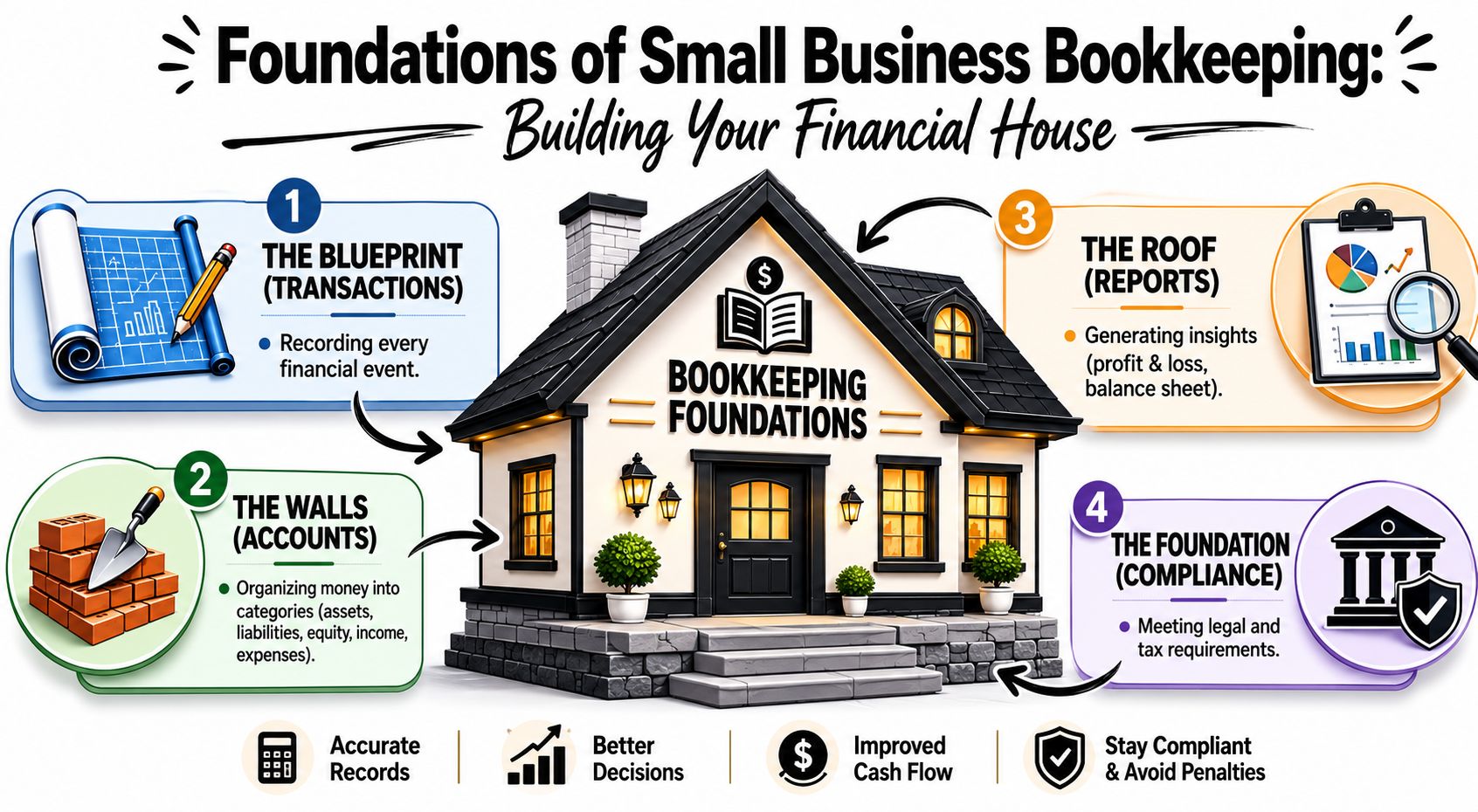

The Foundations of Small Business Bookkeeping

Think of your bookkeeping system like a house. If the slab is crooked, it doesn't matter how nice the kitchen looks. The whole structure will keep giving you trouble.

That's how a lot of small businesses operate. They focus on invoices, tax forms, or software features, but they skip the structural parts that make the numbers reliable.

The house analogy that actually fits

Here's the simple version:

- The blueprint is your transaction flow. Every sale, payment, bill, payroll run, and transfer has to get recorded.

- The walls are your accounts. That's how money gets sorted into assets, liabilities, equity, income, and expenses.

- The roof is your reporting. Your profit and loss and balance sheet protect the business by showing what's happening.

- The foundation is compliance. If the records are weak, tax work, payroll reporting, and lending requests all get shaky.

Why double-entry is the baseline

For any serious company, double-entry bookkeeping is the standard. Every transaction is recorded as both a debit and a credit, which creates a self-balancing system. Xero's guide explains that modern cloud software also automates data capture and reconciliation, which can reduce manual errors by up to 90% when paired with good processes, as noted in this small business bookkeeping guide from Xero.

That matters because mistakes don't stay small. If you record revenue wrong, your profit and loss gets distorted. If you miss a liability, your balance sheet lies. If you post transfers as income, you can convince yourself the business is performing better than it is.

Single-entry systems and homemade spreadsheets can work for the tiniest side hustles. They break down once payroll, loans, inventory, sales tax, or multiple bank accounts enter the picture.

If you want a plain-English refresher on the mechanics, this overview of accounting training by Professional Careers Training does a solid job explaining double-entry without turning it into a textbook.

What the key pieces are for

A lot of owners think they need to “learn accounting.” You don't. You need to understand what each piece is for.

| Part | What it does | Why you care |

|---|---|---|

| Chart of Accounts | Organizes transactions into the right buckets | Bad categories create bad reports |

| Bank reconciliation | Matches your books to the bank | Finds missing, duplicate, or wrong entries |

| Profit and Loss | Shows income and expenses over a period | Helps you spot margin problems |

| Balance Sheet | Shows what you own and owe | Tells you if the business is stable or overleveraged |

Practical rule: If you can't trust the categories, you can't trust the reports. If you can't trust the reports, you shouldn't make decisions from them.

Setting Up Your Bookkeeping System For Success

A bad setup creates cleanup work for years. That's why this part matters more than most owners realize.

I'd rather see a business spend extra time setting up QuickBooks properly than spend months untangling a generic chart of accounts later. Bookkeeping for small business works when the system fits the way the company operates.

Pick software you can grow into

Most businesses outgrow spreadsheets before they admit it. Once you have multiple accounts, recurring bills, payroll, job costs, or a need for clean monthly reporting, move to cloud accounting software.

QuickBooks is the platform I most often recommend for small businesses because it's widely used, flexible, and easier to support as the company grows. The software alone won't save you, though. Plenty of owners buy the tool and then build a messy file inside it.

When you set up the system, make these choices carefully:

- Use the legal business name and correct tax details. Don't guess on entity information.

- Separate business and personal banking. If they're mixed, the books will stay muddy.

- Connect bank and credit card feeds. Automation helps, but only if someone reviews the data.

- Turn on the modules you need. Payroll, classes, locations, projects, and sales tax should match the business model.

Build a chart of accounts that matches reality

Your chart of accounts should help you run the business, not just file a return.

A Jacksonville construction company may need separate categories for materials, subcontractors, equipment rental, and job-related payroll. A healthcare practice may need clean separation for provider compensation, supplies, merchant fees, and administrative overhead. A nonprofit has its own reporting pressures. A one-size-fits-all chart creates one-size-fits-none reporting.

If you need a practical reference, this guide on how to set up a chart of accounts in QuickBooks covers the structure you want before transactions start piling up.

Set up for insight, not just storage

Don't create a giant list of random accounts. Create the few categories that help you answer useful questions.

Use the setup to track things like:

- Revenue by service line: Know which work makes money.

- Direct job costs: Separate labor, materials, and subcontractors when margins matter.

- Recurring overhead: Rent, software, insurance, and admin payroll should be easy to isolate.

- Owner transactions: Keep draws, contributions, and personal charges out of operating expenses.

A clean setup also makes it easier to work with outside help later. If you eventually use a CPA, bookkeeper, payroll specialist, or fractional CFO, they won't have to rebuild the file from scratch.

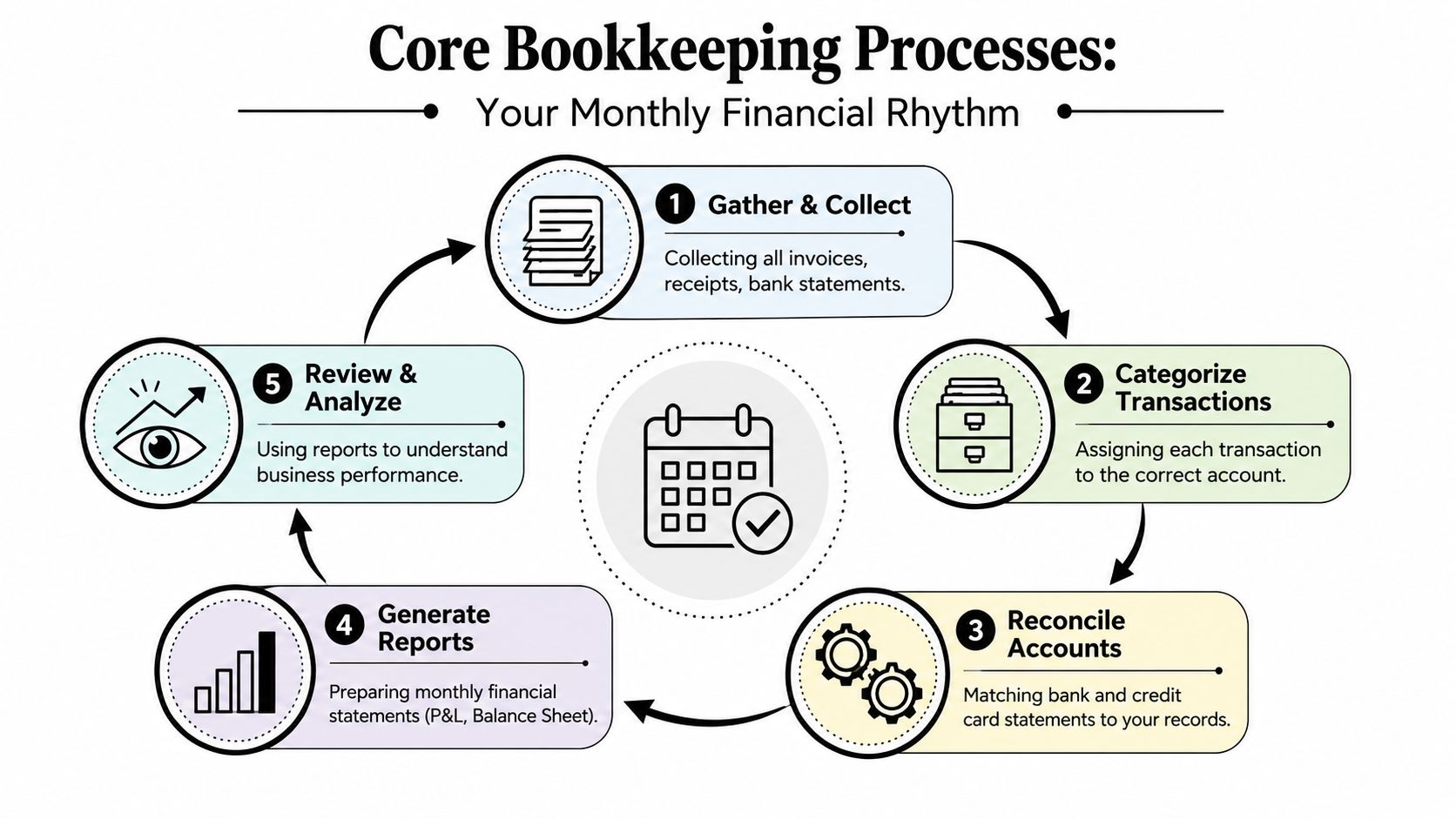

Core Bookkeeping Processes and Monthly Workflows

Good bookkeeping isn't one big annual cleanup. It's a rhythm.

Most problems show up because the rhythm breaks. Transactions pile up. Reconciliations get skipped. Invoices go out late. Bills get paid with no plan. Then the month closes and the reports are either wrong or nonexistent.

A steady monthly workflow keeps the books usable.

The monthly rhythm that keeps a business sane

At the operational level, the monthly cycle usually comes down to five moves:

- Collect the source documents: Invoices, receipts, bank activity, loan statements, merchant reports, payroll data.

- Categorize transactions correctly: Incorrect categorization often causes many books to go astray.

- Reconcile bank and credit card accounts: If the books don't tie to the accounts, stop and fix it.

- Generate reports: Profit and loss, balance sheet, and supporting detail.

- Review the results: Don't just file the reports. Read them.

For a visual walk-through of daily habits that support this cycle, this page on bookkeeping by day is useful.

This short video gives a helpful overview of the basic flow:

What each task is actually protecting

Too many owners think reconciliation is busywork. It isn't. It catches duplicate charges, missing deposits, uncategorized transfers, bank errors, and plain old sloppiness.

Invoicing isn't just about sending bills. It protects cash flow. Accounts receivable management tells you who owes you, how long they've owed you, and whether collections need action. On the payables side, bill tracking helps you avoid late fees, preserve vendor relationships, and time payments intelligently.

Payroll needs the same discipline. If payroll entries are posted late or wrong, job costs get distorted and tax filings become risky. Sales tax needs regular review too. Waiting until filing time to figure it out is how businesses end up scrambling.

A practical monthly checklist

| Task | Why it matters | Common mistake |

|---|---|---|

| Review bank feeds | Keeps transactions current | Letting software auto-post everything unchecked |

| Reconcile accounts | Verifies cash and card balances | Skipping old unreconciled items |

| Send invoices and follow up | Speeds collections | Treating overdue receivables like they'll solve themselves |

| Enter and approve bills | Controls spending and timing | Paying from email without recording the bill first |

| Review reports | Flags margin and cash issues | Looking only at bank balance |

Reconciliation is where bad assumptions meet reality. Reality wins every time.

Using Your Books To Make Smarter Decisions

Friday afternoon. Payroll hits Monday. Your P&L says the month looked fine, but the checking account says otherwise. That gap is where small business owners get blindsided.

Good bookkeeping should help you run the business, not just clean it up for tax time. If your books cannot help you decide when to hire, what to charge, which customers drain cash, and whether a big purchase is smart, then your system is only doing half the job.

A profitable company can still run short on cash

I see this constantly. The owner looks at the income statement, sees a decent month, and assumes everything is under control. Then receivables drag out, payroll clears, vendors want to be paid, and cash gets tight fast.

That is why cash flow needs regular attention. Finaloop makes that point clearly in this bookkeeping guide focused on cash flow. The day-to-day risk for many small businesses is running out of usable cash while waiting on money that has not arrived yet.

For a Jacksonville contractor, the pressure points are usually billing delays, retainage, change orders, and supplier terms. For a medical practice, it is insurance reimbursement lag, provider payroll, and recurring overhead that does not wait. For nonprofits, it is the difference between restricted funds and money you can spend on operations.

The reports that deserve your attention every month

You do not need a bloated dashboard. You need a short list of reports and the discipline to read them like an operator.

Focus on these:

- Profit and Loss: Which services produce healthy margin, and which ones keep everyone busy without enough return?

- Balance Sheet: Is cash getting thinner? Are receivables stacking up? Is debt creeping higher?

- Accounts receivable aging: Who owes you, how old is the balance, and who needs a call this week?

- Accounts payable detail: What needs to be paid now, what can wait, and what should be questioned before approval?

- Cash flow view: What is scheduled to come in, what is scheduled to go out, and where is the squeeze likely to hit?

Used correctly, these reports answer operating questions before they turn into expensive surprises.

Your books should help you make real decisions

Clean books give you a base to work from. Strong management reporting turns that base into action.

A bookkeeper records transactions. A CPA cleans up accounting issues, closes the books correctly, and explains what the numbers mean. A fractional CFO uses those numbers to guide pricing, hiring, financing, forecasting, and timing. That matters once the business has real complexity, especially in Jacksonville industries like construction and healthcare where timing, compliance, and margins can get messy fast.

If your reporting is doing its job, you should be able to answer questions like these without guessing:

- Which service lines are carrying the business?

- Where did margins tighten this quarter, and why?

- Which customers, patients, or payers are slowing down collections?

- Can we afford another hire without squeezing working capital?

- Should we buy equipment now, finance it, or wait six months?

That is the difference between bookkeeping as a tax chore and bookkeeping as part of your operating model.

Good books give you a reliable scorecard. Better advice helps you call the next play.

Software can store transactions. It cannot replace judgment. Once decisions carry real payroll, debt, growth, and compliance consequences, experienced financial oversight pays for itself.

Avoiding Costly Mistakes and Staying Compliant

A lot of business owners say their books are “good enough.” Usually that means the bank feeds are connected and someone has tried to categorize things. That's not compliance. That's hope dressed up as a process.

The problem gets worse as the business grows. More employees, more transactions, more vendors, more reporting, more tax exposure. The operating model that worked when you were small often fails once complexity shows up.

The mistakes that keep hurting small businesses

These problems come up constantly:

- Mixing business and personal spending: It muddies the books and creates cleanup headaches.

- Treating every worker the same: Employee and contractor treatment isn't something to guess on.

- Ignoring sales tax until filing time: That's a dangerous habit.

- Posting loan payments incorrectly: Principal and interest need proper handling.

- Skipping job costing: Construction firms especially end up “profitable” on paper and confused in reality.

- Failing to close the books regularly: If prior periods stay open, reports shift under your feet.

Those aren't minor bookkeeping errors. They affect tax filings, payroll reporting, lender packages, insurance audits, and owner decisions.

Why industry differences matter

Generic online advice falls apart.

A healthcare business has to deal with reimbursement timing, provider compensation, payroll complexity, and careful record handling. A construction company needs strong job costing, subcontractor tracking, equipment costs, progress billing, and change-order discipline. A nonprofit may need clean grant reporting and support for audits or reviews.

That's why the operating model matters. UseHaven's overview points out that the core decision is often between DIY, software, and outsourced bookkeeping, not just which app to buy. It also notes that one-size-fits-all advice misses critical needs in sectors like healthcare, construction, and nonprofits, especially in local markets such as Jacksonville, as discussed in this guide on choosing a bookkeeping model.

Tax law changes and moving rules

Tax compliance is a moving target. Federal rules shift. Florida reporting requirements still need attention. Payroll requirements change. Filing thresholds, documentation standards, and form handling don't stay frozen just because your staff is busy.

I'm not going to pretend every owner should track every tax law change personally. That's not realistic. What is realistic is understanding this: if nobody on your side is actively watching compliance, you're exposed.

Here's the practical standard I'd use for 2026 and beyond:

| Area | What owners should do |

|---|---|

| Payroll taxes | Confirm filings, deposits, and year-end forms are handled on schedule |

| Sales and use tax | Review how taxable sales and exempt items are being treated |

| Contractor payments | Keep records clean and verify year-end reporting support |

| Entity compliance | Make sure the bookkeeping matches how the business is legally structured |

| Industry reporting | Match the books to the reporting needs of healthcare, construction, or nonprofit operations |

If your system only works when nothing changes, it doesn't work.

That's the blunt truth. “Good enough” bookkeeping tends to stay good enough right up until an audit notice, cash squeeze, loan request, or tax issue lands on the desk.

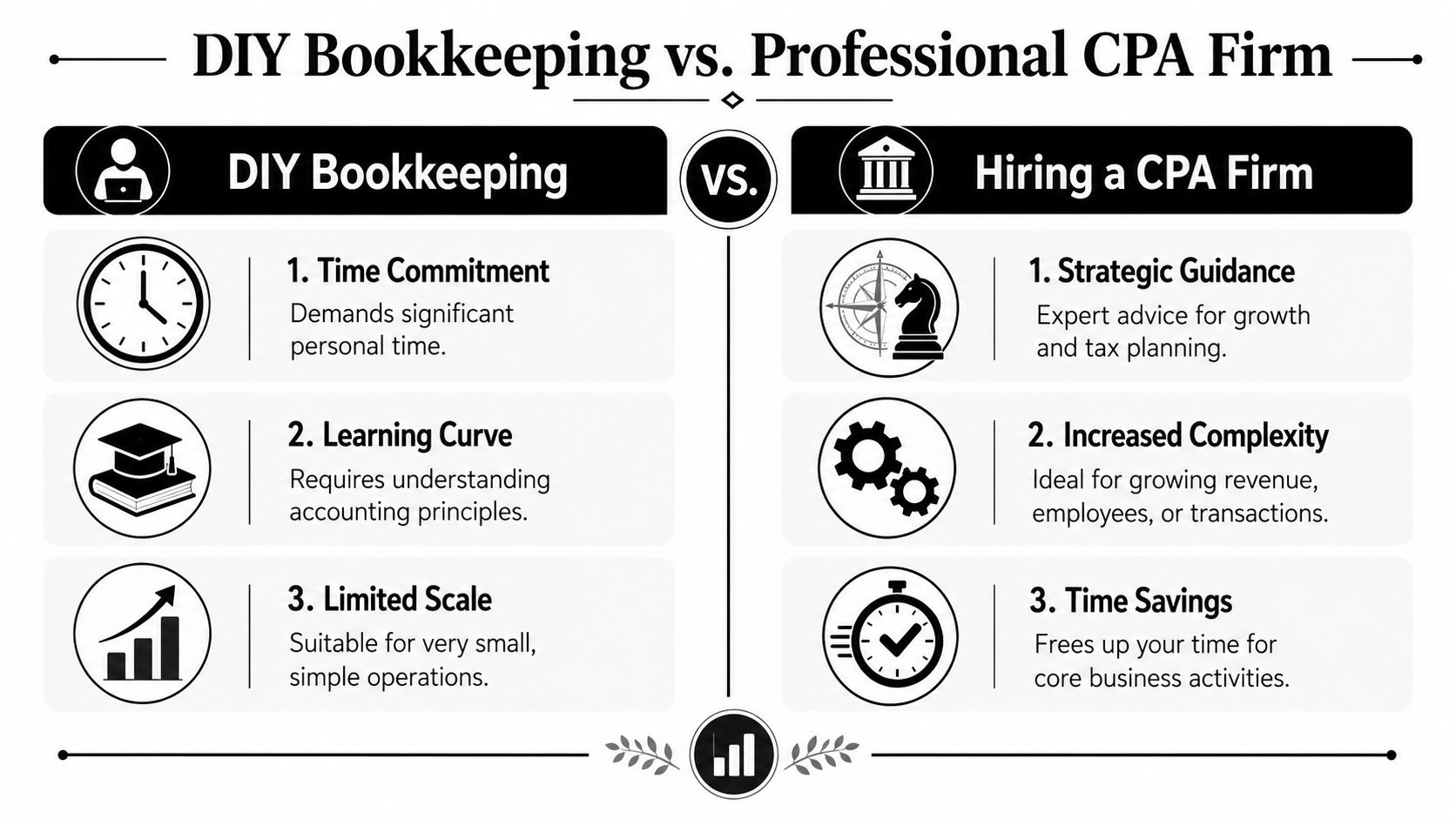

When and How to Hire a Jacksonville CPA Firm

There comes a point when doing it yourself stops saving money and starts costing it.

If the owner is still the bookkeeper, collections manager, payroll reviewer, and tax deadline tracker, the business has a bottleneck. That bottleneck is usually the owner's time and attention. Neither should be spent cleaning up categorization errors at night.

The signs you've outgrown DIY

You probably need outside help if any of this sounds familiar:

- You're always behind: The books are never current.

- You hired employees: Payroll and compliance got more complicated overnight.

- You need financing: Lenders want clean financials, not guesses.

- You can't explain your numbers: Revenue is up, but cash feels tight and you don't know why.

- Your industry has special rules: Construction, healthcare, and nonprofits rarely stay simple.

- You want strategic guidance: You need forecasting, not just transaction entry.

The confidence gap is real. QuickBooks reported that 48% of small business owners were confident they were paying taxes correctly, while confidence rose to 69% among those using a professional accountant, according to these financial literacy statistics from QuickBooks. That gap tells you bookkeeping support isn't just clerical. It changes how owners operate.

Know who does what

A lot of owners use these titles interchangeably. They're not the same.

| Role | Main function | Best use |

|---|---|---|

| Bookkeeper | Records and organizes transactions | Keeps the books clean and current |

| Accountant or CPA | Reviews, adjusts, and interprets financials | Supports reporting, tax, and compliance |

| Fractional CFO | Guides planning and decisions | Helps with forecasting, cash flow, growth, and strategy |

If you're only buying data entry, you'll get data entry. If you need help understanding margins, planning around tax changes, managing cash, or preparing for growth, you need broader support.

For businesses that want bookkeeping, tax support, and higher-level financial guidance under one roof, Bookkeeping and Accounting of Florida Inc. is one local option that provides bookkeeping, accounting, payroll, tax preparation, audits, and fractional CFO services for Jacksonville-area companies. If you're comparing providers, this page on finding the best CPA for small business gives a useful checklist for what to look for.

Why local matters

Jacksonville businesses don't operate in a vacuum. The mix here matters. Healthcare, construction, retail, service businesses, nonprofits, and growing family-owned companies all have different pressure points. A local CPA firm sees those patterns up close.

That matters when you need someone to understand payroll timing, local business realities, reporting expectations, and the way your industry runs in Northeast Florida. It also matters when you want a relationship, not a ticket number.

Outsourcing doesn't mean giving up control. It means getting competent control in place.

If your books are behind, unclear, or built on guesswork, it's time to fix the operating model. Bookkeeping and Accounting of Florida Inc. helps Jacksonville and Northeast Florida businesses keep clean books, stay compliant, and use their numbers for smarter decisions with bookkeeping, CPA support, and fractional CFO guidance.