A lot of Jacksonville contractors live the same story. The crews stayed busy, the project wrapped, the checking account doesn't look terrible, and yet the financials say the job barely made money. Sometimes they say it lost money. That's the moment owners realize they've been steering a bulldozer with a car dashboard.

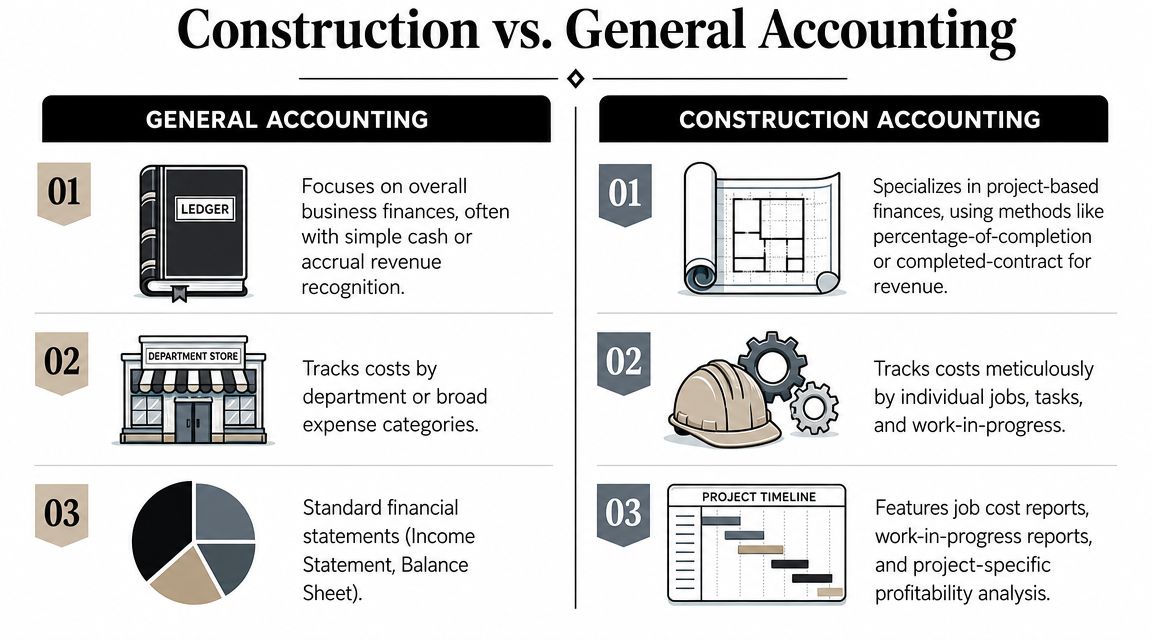

That gap usually isn't a field problem first. It's an accounting problem. Accounting for construction companies is different because the work is project-based, the cash moves in odd patterns, and revenue often has to be recognized across contracts that last months or years, not at a single point of sale, as explained in industry guidance on construction accounting.

Most generic bookkeeping setups can't handle that reality. They lump costs together, miss job-level margin drift, and leave owners blind until the damage is already done.

If you're a contractor in Northeast Florida, this also ties directly to risk. Bad books don't just produce ugly tax returns. They lead to bidding mistakes, payroll issues, bond pressure, insurance headaches, and compliance trouble. That's why I tell owners to look at accounting the same way they look at site safety. If the foundation is weak, everything on top of it gets dangerous. On the risk side, TCDS Agency's advice for contractors is worth reading because insurance mistakes and accounting mistakes usually show up together, and they usually show up late.

Why Your Profits Vanish on Paper

A contractor calls after finishing a solid stretch of work. Revenue looked strong. Crews were moving. Vendors got paid. Then the year-end financials come in, and the profit is thin enough to make you question the whole business.

That doesn't happen because construction is impossible to manage. It happens because too many owners use small-business accounting logic in a project-based industry.

Your bank balance is lying to you

Cash in the bank tells you one thing only. It tells you what cash is sitting there today. It does not tell you which jobs made money, which ones are bleeding, or whether your reported profit lines up with actual project progress.

Construction accounting runs on four hard disciplines: job costing, cost management, revenue recognition, and cash-flow management, with specialized reports such as financial statements, WIP reports, job cost reports, and project budget reports all playing different roles, according to construction accounting guidance. If your bookkeeper treats your company like a retail store, your numbers will mislead you.

Your business can be busy and still be losing control. Busy hides mistakes for a while.

The usual breakdown

Here's what I see most often:

- Costs posted too broadly: Labor, materials, and subcontractors land in general expense buckets instead of the right job.

- Revenue recognized at the wrong time: Owners think a signed contract equals profit. It doesn't.

- No project-level reporting: The company P&L looks acceptable while one or two jobs steadily erode the year.

- Compliance treated like an afterthought: Payroll, tax filings, and contract reporting get handled late and patched together.

If that sounds familiar, you don't need a prettier bookkeeping file. You need a construction-specific accounting system and someone who knows how to read it.

The Core Concepts of Construction Accounting

Construction accounting has a different engine under the hood. If you don't understand the gauges, you'll drive straight into a margin problem and won't know it until the project is almost done.

Job costing is your real profit statement

In construction, each job should act like its own profit center. That means labor, materials, equipment, subcontractors, and indirect job costs must be assigned to the specific contract through job costing and cost coding, not dumped into broad company totals, as outlined in this construction job costing guide.

If you can't pull a job cost report and see where a project stands against budget and estimated cost-to-complete, you're not managing profit. You're guessing.

Revenue recognition decides whether your numbers mean anything

For long-term contracts, percentage-of-completion matters because it recognizes revenue and expenses incrementally. The basic formula is straightforward: costs incurred to date divided by total estimated costs gives the completion percentage, and that percentage is applied to contract value to determine period revenue, as explained in this overview of PCM.

That sounds technical, but the lesson is simple. Bad estimates create bad financial statements. If total estimated costs are too low, profit gets recognized too early and the books tell a fairy tale.

| Feature | Percentage-of-Completion (PCM) | Completed-Contract (CCM) |

|---|---|---|

| Revenue timing | Recognized as the project progresses | Recognized when the project is completed |

| Best fit | Long-term, multi-period work | Simpler jobs where end-of-job recognition is more practical |

| Main strength | Matches revenue to actual progress | Simpler to understand during the job |

| Main risk | Bad estimates distort margin early | Profit can appear late and create volatility |

| Management value | Better ongoing visibility | Less useful for mid-project control |

If you're comparing systems, software matters, but setup matters more. This roundup to compare contractor accounting solutions is useful because features only help if the system can support job costing, billing, and reporting the way contractors work.

WIP and retainage are where reality shows up

A work-in-progress report tells you whether the financial story matches job progress. Retainage tells you some of your earned money is still being held back. Together, they explain why a job can look profitable and still starve your cash.

Practical rule: If you review only the income statement and ignore WIP, you're reading half the story.

Owners who don't track these items monthly usually find out about trouble after the field already felt it.

Building Your Financial Blueprint for Success

A contractor in Jacksonville can stay busy all year and still bleed cash because the books were built for tax prep instead of job control. That setup hides overruns, buries change orders, and turns compliance problems into profit problems. If you want clean margins and fewer surprises, build the accounting system around how construction work runs.

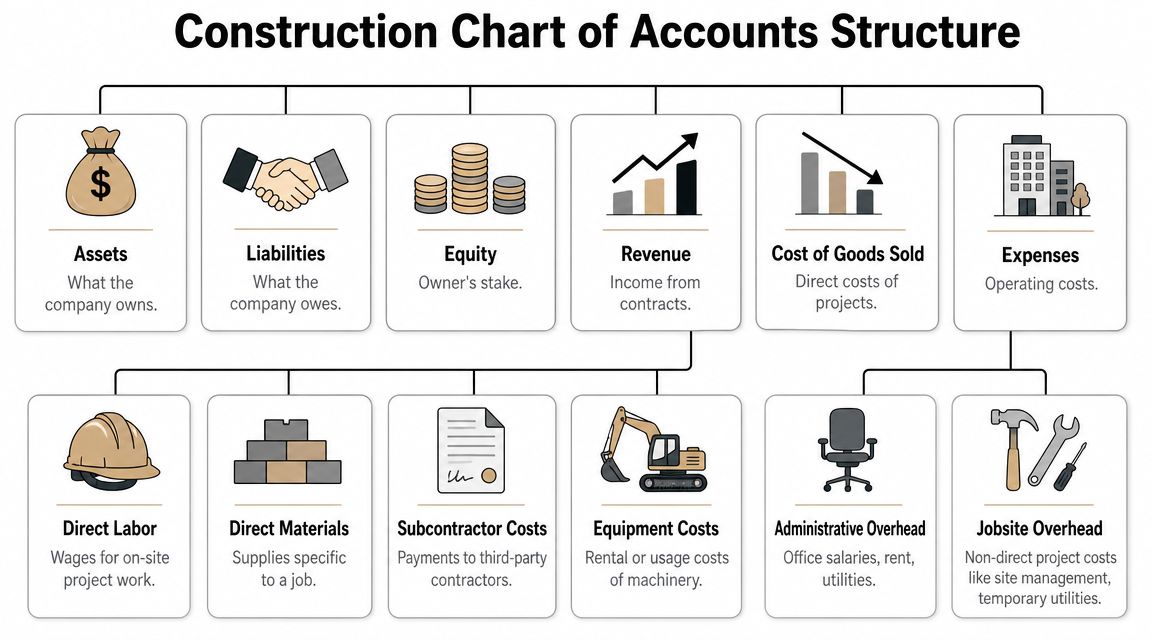

Build the books around jobs, not around tax categories

A generic chart of accounts gives you generic answers. In construction, generic answers get owners in trouble.

Set up the books so every dollar can be tied back to a job, a phase, and a cost type. Direct labor, materials, subcontractors, equipment, and overhead need their own lanes. Then add cost codes that the office and field use the same way every time. If one superintendent codes cleanup to labor, another codes it to miscellaneous, and the office guesses the rest, your reports are fiction.

Each project should stand on its own as a profit center. That is how you catch a job drifting off budget before it eats the company.

What a clean setup actually includes

A construction accounting file should give you control, not just a place to dump transactions. Start with these pieces:

- A job list tied to signed contracts: Every active project needs its own reporting trail.

- Cost codes everyone follows: Estimating, project management, payroll, and bookkeeping must use the same coding structure.

- Separate overhead categories: Office rent and project trailer costs do not belong in the same bucket.

- Billing built to match the contract: Progress billings, retainage, deposits, and change orders should flow through the books without manual workarounds.

Software matters, but setup matters more. QuickBooks can work fine for many contractors. Bad configuration turns it into a filing cabinet with a calculator attached. Before changing systems or migrating data, review practical guidance on accounting software for construction companies.

Equipment and financing hit both profit and cash

Equipment decisions shape job costing, margins, and cash flow at the same time. If you lease a machine, buy one, or shift equipment between jobs without a clear allocation method, job reports lose credibility fast. Then owners start pricing future work off bad history, which is how thin margins get thinner.

Financing decisions need accounting discipline behind them. This guide to equipment leasing benefits is useful because it shows why leasing is not just a payment decision. It affects usage tracking, fixed asset planning, and how you measure job performance.

A bad chart of accounts works like pouring concrete without forms. Money goes everywhere, and cleaning it up costs more than setting it up right the first time.

For contractors in Northeast Florida, this is usually the point where a specialized fractional CFO or construction CPA stops being a luxury and starts being a guardrail. Bookkeeping and Accounting of Florida Inc. provides construction-focused bookkeeping, payroll, tax, reporting support, and QuickBooks ProAdvisor setup for local businesses that need tighter control.

Navigating Payroll and Compliance Landmines

Friday afternoon. Payroll is due. One crew worked a private remodel, another spent two days on a public job, and your office manager ran everyone through the same process to keep things moving. That shortcut is how contractors in Northeast Florida end up with back wages, workers' comp surprises, tax notices, and profit fade that never showed up in the original estimate.

Payroll in construction controls far more than paychecks. It affects job costing, contract compliance, insurance audits, and whether your books can stand up when a state agency, surety, or prime contractor asks questions. If your payroll process is sloppy, your financial statements are sloppy too.

Certified payroll is not ordinary payroll

Public work adds rules fast. Wage classifications, hourly rates, fringe calculations, apprentice status, and job-level support all have to match. One bad code or missing record can turn payroll into a contract problem, and contract problems get expensive.

A payroll processor does not solve that for you. The processor runs checks and direct deposits. Your company still has to keep clean labor classifications, job coding, time records, and supporting documentation. Contractors handling public projects should review these certified payroll reporting requirements before the next filing deadline, not after a notice lands on the desk.

Many owners lose money without seeing it. They underbill change work, miscode labor, or miss prevailing wage details, then spend months cleaning up records for someone else's review. A specialized construction CPA or fractional CFO fixes the process upstream, before payroll errors start bleeding margin and creating compliance exposure.

The hidden risks of workers' comp and labor classification

Misclassified labor is one of the fastest ways to turn a decent year into a painful one. If field labor, supervisors, subcontractors, and office payroll are not documented and coded correctly, workers' comp audits can hit like a roof collapse. The bill shows up late, but the mistake started months earlier.

Watch for these warning signs:

- Crew members coded inconsistently: The same work lands in different classifications from one pay period to the next.

- Subcontractor records missing support: Payments go out, but the file does not support independent contractor treatment or the proper class code.

- Job payroll not tied to work performed: Hours are recorded, but the backup does not show who did what, where, and under which classification.

- Compliance handled at year-end: By then, the bad habits are baked in and the corrections are expensive.

Later in the process, this video gives a useful overview of the reporting mindset contractors need:

If payroll records can't survive scrutiny, neither can your margin.

Tax Strategies and New Laws for Contractors

Most contractors treat taxes like storm cleanup. They wait until the weather hits, then scramble. That's backward. Tax planning in construction should happen during the year, while you still have time to change the outcome.

Revenue method decisions affect tax timing

Your accounting method doesn't just shape financial reporting. It affects when income shows up and how predictable your tax burden feels. For long-term contracts, revenue recognition choices can change the timing of reported profit, which is why contractors need tax planning tied directly to their contract mix, billing patterns, and estimate quality.

Owners often encounter issues when following “my buddy's contractor does it this way” advice. Tax strategy has to fit your contracts, your entity structure, your books, and your reporting obligations. One-size-fits-all tax planning usually turns into expensive amendment work.

Equipment purchases and cash flow planning need a tax lens

Equipment is another area where contractors often leave money and flexibility on the table. The wrong purchase timing can strain cash. The wrong ownership structure can complicate depreciation strategy and project costing. The wrong paperwork can slow down tax prep and audit support.

Good tax planning for contractors usually includes:

- Reviewing major purchases early: Don't wait until year-end to decide how equipment should be handled.

- Aligning tax strategy with financing: A lease, financed purchase, or outright buy decision affects more than monthly cash flow.

- Keeping books clean during the year: Tax strategy built on messy records is just a guess in a tie.

Stay alert to law changes and filing requirements

Tax law changes hit contractors in pieces. Filing thresholds, payroll requirements, reporting rules, and entity-specific issues don't all change at once. That's exactly why owners need active oversight instead of reactive tax prep.

A seasoned CPA should be telling you what changed, what to document, what elections need review, and how to prepare before filing season. If nobody is having those conversations with you during the year, you don't have tax strategy. You have tax compliance at best.

The right advisor also keeps an eye on Florida and local implications that affect contractors with multiple job sites, subcontractor-heavy models, and growing payroll complexity.

Reports and KPIs That Actually Drive Profit

Most contractors already get reports. The problem is they get the wrong ones, too late, or in a format nobody uses. A standard profit and loss statement has value, but in construction it's only one instrument on the panel.

The reports that deserve your attention

Three reports carry the most weight in day-to-day control:

- Job cost report: This shows where labor, materials, equipment, and subcontractor costs are landing by project.

- WIP schedule: This helps reconcile progress, earned revenue, billings, and margin position.

- Project profitability summary: This lets you compare jobs and spot patterns in estimating, execution, and closeout.

If you're not reviewing these consistently, you're managing by rearview mirror.

Benchmarks matter because lenders and sureties care

Financial benchmarks give you context. A healthy construction firm often targets a current ratio of about 1.5–2.0, and sureties often prefer a debt-to-equity ratio below 1.0, according to construction financial benchmark guidance. The same source notes profitability targets of 12–16% gross profit margin for general contractors, 15–25% for specialty contractors, and 8–15% overhead.

Those numbers matter for more than bragging rights. They affect borrowing conversations, bonding confidence, and how much stress your company can absorb when collections slow down.

| KPI or Report | What it tells you | Why it matters |

|---|---|---|

| Current ratio | Short-term liquidity | Helps show whether the company can cover near-term obligations |

| Debt-to-equity | Leverage position | Important for sureties and lenders |

| Gross profit margin by job | Actual project profitability | Shows estimating and production strength |

| Overhead trend | Cost discipline outside direct job costs | Protects margin from office bloat |

| WIP report | Whether billing and earned revenue align | Exposes hidden profit distortion |

Watch trends, not just snapshots. One decent month can hide a bad operating pattern.

A report is only useful if it drives action

If a job's gross margin slips, somebody should ask why. If receivables drag, somebody should tighten billing and collection follow-up. If overhead creeps up, somebody should stop treating every admin expense like a harmless cost of growth.

That “somebody” is often missing in small and mid-sized construction companies. The owner is busy in operations, the office manager is buried, and the outside tax preparer shows up after the damage is done.

Stop Guessing and Hire a Fractional CFO

Friday afternoon. Payroll is due, a project manager swears a job is still profitable, and your bank balance says otherwise. The books are technically current, but nobody can tell you which job is bleeding, whether retainage is choking cash flow, or whether your WIP is reporting fiction. That is how contractors in Jacksonville end up paying taxes on paper profit while fighting for cash in practice.

A bookkeeper records transactions. A tax preparer files returns. Neither role is built to run financial control inside a construction company. You need someone who can read the story behind the numbers, challenge bad assumptions, and force decisions before a small margin leak turns into a claim, a covenant problem, or a payroll crisis.

That is the job of a fractional CFO.

For a small or mid-sized contractor, hiring a full-time CFO usually makes no economic sense. Paying for CFO-level judgment does. A good fractional CFO should own the financial discipline your company is missing and turn scattered reports into operating decisions.

That means:

- Reviewing WIP like a skeptic. If overbillings, underbillings, retainage, and change orders do not tie out, somebody needs to say it.

- Connecting field performance to financial results. Labor overruns, slow billing, and sloppy job costing do not stay in the field. They hit margin, cash, and compliance.

- Running a real monthly close. Owners need usable numbers while a job can still be corrected, not months later when the damage is permanent.

- Keeping lenders, sureties, and tax deadlines from becoming emergencies. Construction companies lose money when reporting is late, weak, or unreliable.

Many firms struggle with the reporting side of project-based accounting because progress billing, retainage, and contract changes distort the picture until someone experienced cleans it up, as discussed in this article on construction accounting challenges.

Owners often make the same bad call. They hire a stronger bookkeeper and expect strategic problems to disappear. That is like hiring a better scorekeeper and expecting the team to win more games. Clean books matter. They do not replace forecasting, margin analysis, cash planning, compliance oversight, or hard conversations about jobs that are going sideways.

If you need a clearer picture of the role, read this explanation of what fractional CFO services are.

In Northeast Florida, contractors face significant financial risks, often more than they admit. Weak reporting can cost you with sureties, lenders, sales tax exposure, payroll issues, and bids priced off bad historical data. Lost profit and non-compliance usually start with the same problem. Nobody is driving the financial side of the business with enough authority or enough skill.

Bookkeeping and Accounting of Florida Inc. provides that level of oversight for Jacksonville and Northeast Florida construction companies that need accurate books, job-cost visibility, payroll support, tax guidance, and CFO-level direction without carrying a full-time executive salary.