You've got a business to run. Customers to serve, staff to manage, vendors to chase, and about fifteen things on fire before lunch. So the receipts go in a shoebox, the bank feed piles up, payroll gets handled when it's urgent, and taxes become a future-you problem.

That works right up until it doesn't.

If you're searching for how to accounting for small business, you probably don't need another fluffy checklist. You need a practical system that keeps you compliant, tells you where the cash is going, and helps you make better decisions before a mistake gets expensive. That's what accounting is supposed to do. It's not just tax prep with extra steps. It's the operating system for your business.

Your Business Needs More Than a Shoebox

The shoebox method is familiar for a reason. It starts innocently. A few receipts from Home Depot. A restaurant charge you meant to label. A payroll note scribbled on an envelope. Then six months pass, and now your “books” are a scavenger hunt.

I see this all the time with owners who are smart, hardworking, and completely buried. A contractor in Jacksonville knows every job in progress but can't say which one is profitable. A clinic owner knows collections feel slow but can't see which payers are dragging cash flow down. A retailer is selling plenty and still feels broke at the end of the month.

That's not a hustle problem. It's an accounting problem.

What disorganized books really cost you

Messy records don't just make tax season annoying. They block decisions you should be making every week.

- Hiring gets harder because you can't tell whether payroll fits your margin.

- Pricing stays fuzzy because expenses aren't categorized properly.

- Cash flow surprises you because nobody's watching receivables, payables, and upcoming obligations in one place.

- Tax prep costs more because cleanup work always costs more than maintaining clean books.

Good accounting gives you a dashboard. Bad accounting gives you anxiety.

Small businesses matter too much to run this way. The U.S. small-business sector makes up 99.9% of all U.S. businesses, employs about 60 million people or roughly 47.1% of the private workforce, and accounts for 44% of U.S. economic activity, according to small-business economic data summarized by Salesgenie. If your business is part of that engine, your numbers need to be more than a pile of receipts and crossed fingers.

The real goal is control

Proper accounting gives you three things owners care about:

- Clarity on what you earned, what you owe, and what's left.

- Control over payroll, taxes, vendor payments, and owner draws.

- Confidence when you decide whether to hire, expand, borrow, or cut costs.

If you're not sure who you need as you grow, this breakdown of finance roles for growing businesses is worth reading. A lot of owners wait too long to add the right financial support, then wonder why growth feels chaotic.

Shoeboxes belong in closets. Your accounting belongs in a system.

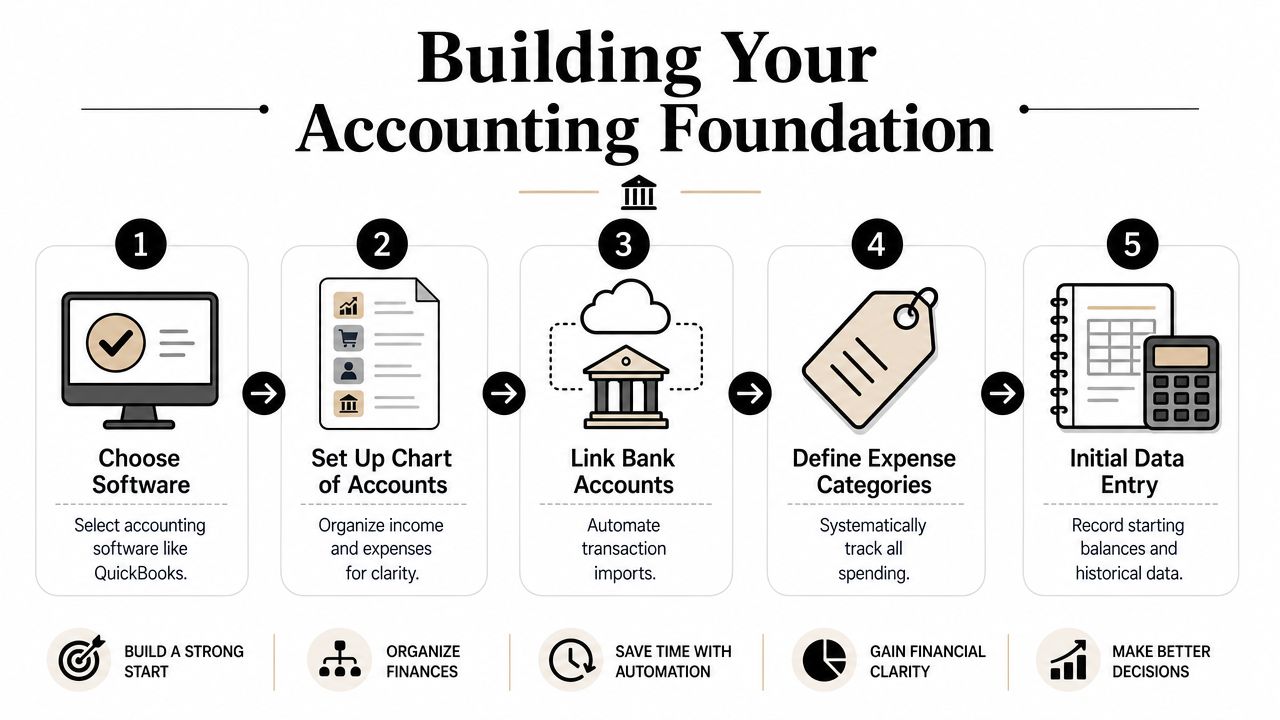

Building Your Accounting Foundation

If your setup is shaky, everything after it gets harder. Cleanup, tax filing, job costing, cash flow planning, lender reporting, all of it. Start with the basics and get them right the first time.

Here's the visual version of the process.

Choose software you'll actually use

For most small businesses, QuickBooks is the practical choice. It's widely used, flexible, and it handles the core jobs most owners need: bank feeds, invoicing, accounts payable, payroll integration, reporting, and cleanup when things drift.

Don't overcomplicate this. If you're running a small or midsize company, you probably don't need an enterprise accounting platform. You need clean setup, consistent use, and someone who knows how to structure it properly. As certified QuickBooks ProAdvisors, Bookkeeping and Accounting of Florida Inc. sets up and maintains QuickBooks for businesses that need reliable books and cleaner reporting.

Your chart of accounts is your filing cabinet

A chart of accounts is just the master list of categories your books use. It's comparable to folders in a filing cabinet. If the folders are sloppy, everything you file into them becomes useless later.

A good chart of accounts should separate:

- Income by meaningful revenue type

- Cost of goods sold where applicable

- Operating expenses such as rent, payroll, software, supplies, and marketing

- Assets like cash, receivables, and equipment

- Liabilities like loans, credit cards, payroll taxes, and sales tax payable

- Equity for owner contributions and draws

Don't create fifty tiny categories because it feels thorough. That's not sophistication. That's clutter.

A short walkthrough helps if you're visual:

Pick cash or accrual and stop guessing

A lot of owners get bad advice. A proper accounting workflow begins with choosing cash or accrual basis, creating a chart of accounts, and using double-entry bookkeeping. Cash basis is simpler, but accrual basis records revenue when earned and gives a more accurate view of performance, especially for businesses that invoice clients or hold inventory, as explained in this small-business accounting workflow guide from Finally.

Practical rule: If you invoice after the work, carry inventory, manage projects over time, or need real visibility into margins, accrual usually tells the truth better than cash basis.

Here's the plain-English version:

| Method | What it records | Best fit |

|---|---|---|

| Cash basis | Money when it's received or paid | Very simple operations with minimal timing issues |

| Accrual basis | Revenue when earned, expenses when incurred | Growing businesses, inventory businesses, project-based work, healthcare, construction |

The mistake isn't picking one. The mistake is picking one without understanding the tradeoff, then making business decisions from distorted numbers.

Mastering Your Bookkeeping Rhythms

Accounting setup is the foundation. Bookkeeping rhythm is the habit that keeps the place from falling apart.

A business doesn't usually get in trouble because one transaction was miscoded. It gets in trouble because nobody stayed on top of the routine. Weeks pass. Then months. Receivables age. Bills sit. Bank balances look healthy until payroll hits. That's how owners end up saying, “We're busy, so why does cash feel tight?”

The daily and weekly work that keeps cash visible

Take a small construction company in Northeast Florida. The owner has crews in the field, fuel charges hitting cards daily, vendor invoices coming in from multiple suppliers, and customer draws tied to project milestones. If those transactions aren't coded quickly and consistently, job profitability gets blurry fast.

The same thing happens in healthcare. A clinic may be busy every day and still struggle because collections lag, payroll is fixed, and recurring expenses keep drafting. Without disciplined bookkeeping, production and cash don't line up.

Your weekly rhythm should include:

- Categorizing transactions so expenses land in the right buckets the first time

- Reviewing accounts receivable so overdue invoices don't age in silence

- Reviewing accounts payable so you can control timing and avoid late fees or strained vendor relationships

- Capturing receipts and support while the details are still fresh

- Flagging unusual charges before they turn into cleanup headaches

Monthly reconciliation is non-negotiable

If you skip reconciliation, you're not doing accounting. You're collecting guesses.

Every month, your bank accounts, credit cards, loan balances, and key liability accounts should match your books. That's how you catch duplicate entries, missing deposits, uncategorized charges, old checks, and payroll issues before they spill into tax filings and financial reports.

Reconciliation is where bad assumptions go to die.

One useful reference for owners who want the basics laid out cleanly is this page on bookkeeping for small business. It covers the ongoing work most businesses need to keep records current instead of reconstructing them later.

Keep the rhythm simple

You don't need a heroic system. You need a repeatable one.

Try this operating cadence:

- Daily. Review imported transactions and attach documentation where needed.

- Weekly. Check receivables, unpaid bills, and cash commitments.

- Monthly. Reconcile all balance sheet accounts and review financial statements.

- Quarterly. Clean up edge cases, owner transactions, and tax-sensitive items before they snowball.

The common mistakes that wreck the rhythm

A few habits create most of the mess:

- Mixing personal and business spending. This destroys clean reporting and makes tax prep miserable.

- Letting uncategorized transactions pile up. A small delay becomes a large cleanup.

- Ignoring old receivables. Revenue on paper doesn't pay payroll.

- Treating bookkeeping as a year-end task. By then, the damage is already baked in.

If you want to learn how to accounting for small business properly, don't obsess over fancy reports first. Nail the rhythm. Clean books come from boring discipline, not last-minute panic.

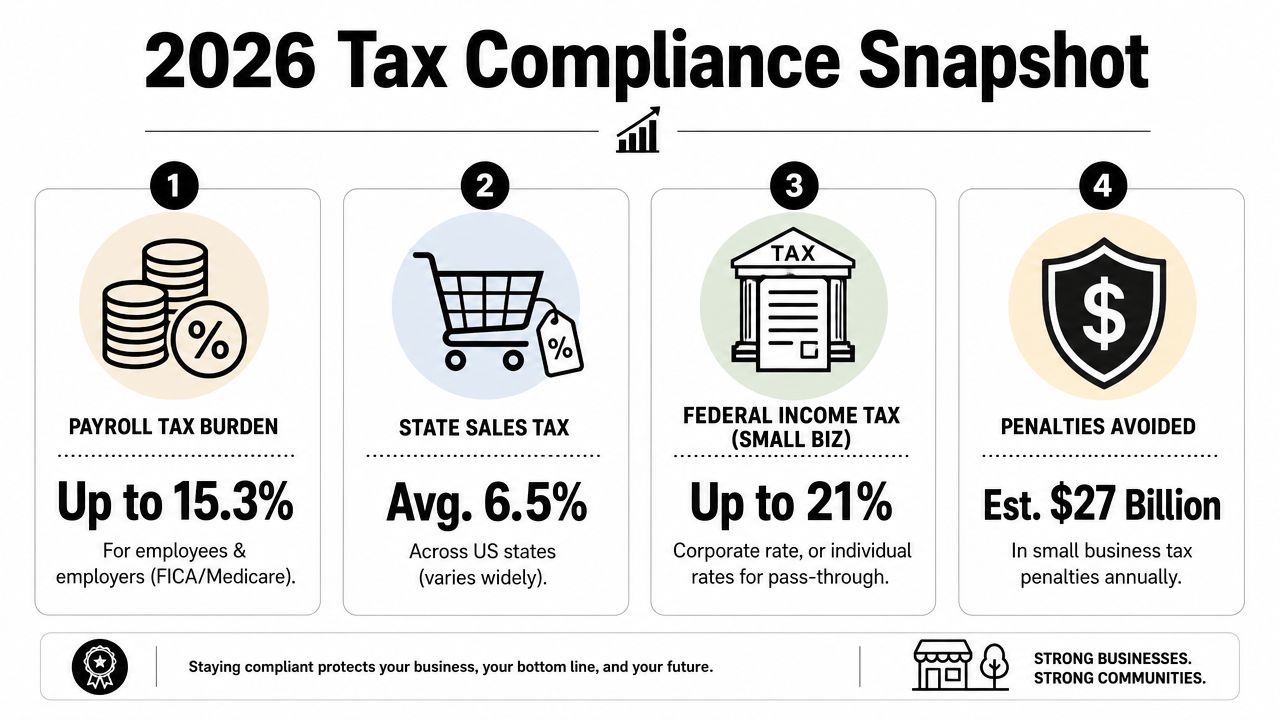

Navigating Payroll and Tax Compliance in 2026

Payroll and taxes are where a lot of confident owners suddenly get very quiet.

They should. This area is unforgiving. Miss a filing, classify something wrong, forget a payroll item, or fail to track sales tax properly, and the government does not respond with warm encouragement. It responds with notices, penalties, and wasted time.

Here's the section where I'll be blunt. If you're trying to stay current on 2026 tax law changes, payroll requirements, entity-specific filing rules, and state obligations by skimming headlines between meetings, you're gambling.

Most owners are less confident than they look

Only 48% of small business owners say they're confident they're paying taxes correctly, according to QuickBooks financial literacy statistics. That should tell you something important. Plenty of owners are operating with uncertainty and hoping they're close enough.

Hope is not a compliance strategy.

If you have employees, payroll alone creates a stack of responsibilities. Gross wages, withholdings, employer taxes, benefit deductions, reporting deadlines, and year-end forms all have to line up. If you sell taxable goods or services, sales tax adds another layer. If you operate through an LLC, S corporation, partnership, or corporation, filing requirements and owner payment treatment differ. None of this gets simpler because your business is busy.

Florida businesses still need structure

Florida owners sometimes assume “no state income tax” means lighter compliance overall. That's a dangerous shortcut. You still need to manage payroll correctly, maintain accurate books, track deductible expenses, and handle the tax obligations that apply to your entity and operations.

For businesses with multiple revenue streams, contractors, property income, or specialized deductions, the rules get more nuanced. If part of your income comes from rentals, this guide to understanding rental property taxes is a useful example of how quickly “simple” tax situations stop being simple.

What professional tax support actually does

Professional accounting support isn't just someone typing numbers into forms. Done right, it gives you:

- Deadline control so payroll and tax filings happen on time

- Clean records that support deductions and reduce rework

- Entity-specific guidance so you're not mixing business and owner tax treatment

- Issue spotting before notices arrive

- Current interpretation when rules shift and forms change

If payroll is one of your pain points, this page on how to set up payroll for small business is a practical starting point.

The cheapest way to handle taxes is rarely the least expensive. Cleanup, penalties, and bad decisions cost more than good guidance.

DIY can work for a very simple business. But once you have staff, growth, multiple accounts, inventory, projects, or irregular tax issues, professional help stops being a luxury. It becomes part of staying compliant and sane.

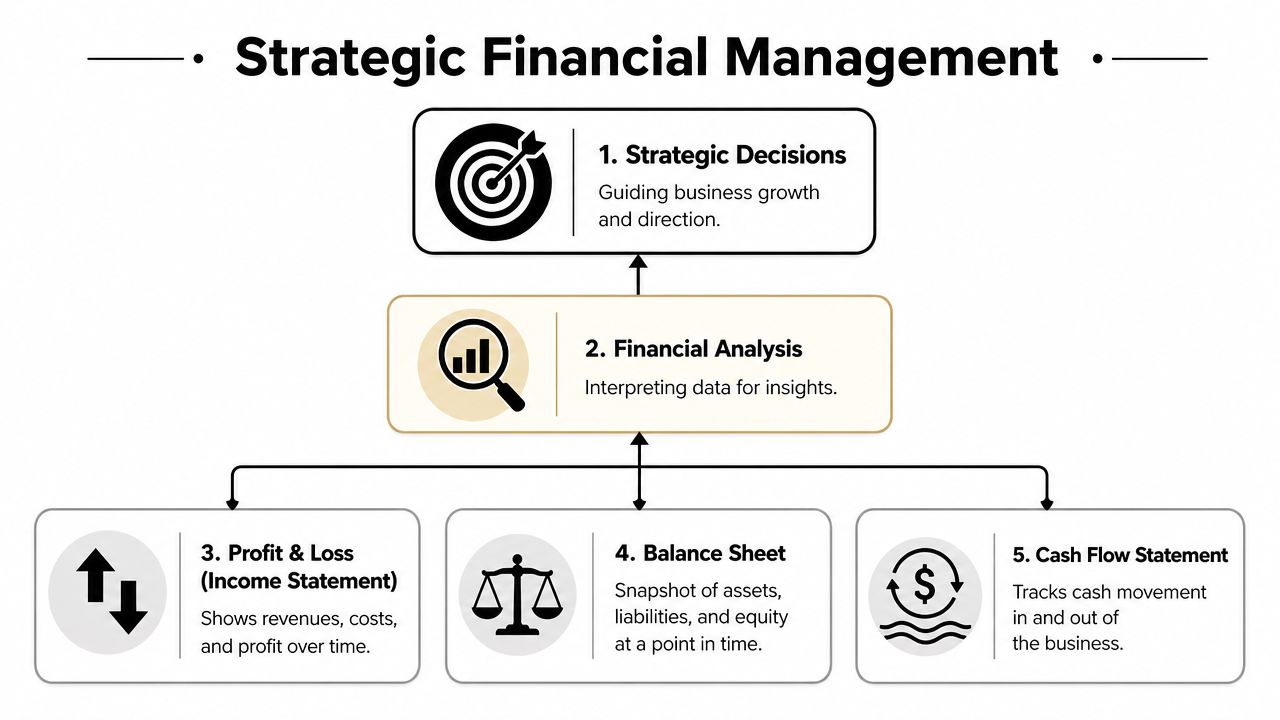

Turning Data into Decisions with Reports and Controls

Bookkeeping records the activity. Accounting interprets it. That's the difference between a pile of transactions and an actual management tool.

Too many owners look at their bank balance and call it financial management. That's like judging your health by whether you can still walk up stairs. Useful, maybe. Complete, not even close.

Three reports tell the real story

If your books are clean, three reports should guide your decisions.

| Report | What it tells you | Why it matters |

|---|---|---|

| Profit and Loss | Revenue, costs, and profit over a period | Shows whether operations are actually profitable |

| Balance Sheet | Assets, liabilities, and equity at a point in time | Shows financial position and obligations |

| Cash Flow Statement | How cash moved in and out | Shows whether profit is turning into usable cash |

Each report answers a different question.

The Profit and Loss tells you whether the business model works. The Balance Sheet tells you what the business owns and owes. The Cash Flow Statement tells you whether you can fund payroll, debt, and growth without a surprise.

Controls matter as much as reports

Now the less glamorous part. Internal controls.

Small businesses are especially vulnerable to fraud and weak processes. The U.S. Chamber notes that small businesses need internal processes to reduce fraud and accidental loss, and the Association of Certified Fraud Examiners' latest global survey reported a median loss of $145,000 per occupational fraud case, as summarized in this small-business accounting and controls guide from the U.S. Chamber.

That number gets attention. The fix is usually not fancy. It's discipline.

Controls that punch above their weight

Start with a few basics:

- Separate duties where possible. The same person shouldn't approve vendors, pay bills, and reconcile the account if you can avoid it.

- Review bank and credit card activity monthly. Fast review catches stupid mistakes and deliberate ones.

- Restrict software access. Not everyone needs permission to change vendors, payroll, or account mappings.

- Set approval thresholds. Larger payments should require another set of eyes.

- Review the vendor list. Old, duplicate, or suspicious vendor records deserve attention.

A good control system doesn't slow the business down. It stops dumb losses from draining it quietly.

If you're trying to make reporting more timely, automation can help. This guide on AI and automation for FinOps is useful for thinking through where automation belongs and where human review still matters.

For construction companies, that may mean tighter coding of job costs and purchase approvals. For healthcare practices, it may mean cleaner revenue-cycle visibility and tighter review of payroll and vendor payments. Different industries use different levers, but the principle is the same. Good data plus basic controls gives you a safer, smarter business.

Why Every Growing Business Needs a Fractional CFO

Here's where owners often get stuck. They know they need help, but they hire only for compliance and not for decision-making.

That's backward.

A bookkeeper records transactions. A CPA handles compliance, tax, and reporting standards. A fractional CFO helps you steer the business. Different jobs. All useful. But if your company is growing, the last role is the one that keeps you from making expensive decisions with incomplete information.

What each role actually does

This is the most orderly way to view it:

- Bookkeeper. Keeps records current, reconciles accounts, manages the mechanics.

- CPA. Makes sure filings, financial presentation, and tax treatment are handled correctly.

- Fractional CFO. Builds forecasts, monitors cash flow strategy, helps with pricing, hiring plans, margin analysis, financing decisions, and growth choices.

Most struggling businesses don't fail because nobody entered the credit card transactions. They struggle because nobody translated the numbers into action.

Growth makes simple accounting less reliable

Many guides oversimplify the cash-versus-accrual choice. For growing businesses, especially project-based or inventory-heavy companies, simple cash accounting can become misleading and hide cash flow risks, which is why the SBA's guide to managing business finances frames accounting as a management system, not just a tax-prep task.

That point matters more than owners realize.

A contractor can look profitable while cash is tied up in receivables and work in progress. A medical practice can post strong production but still feel squeezed because collections lag and payroll keeps hitting on schedule. A retailer can sell plenty and carry too much inventory at the same time. None of those problems gets solved by basic bookkeeping alone.

What a fractional CFO changes

A good fractional CFO helps you answer questions like:

- Can we afford to hire before the next busy season?

- Which service lines produce margin after labor and overhead?

- Are we collecting fast enough to support growth?

- Should we finance equipment, delay expansion, or change pricing?

- What does the next quarter look like if revenue softens?

Those are executive questions. They need executive-level financial thinking.

If you want a clearer picture of the role, this overview of fractional CFO services lays out how outsourced CFO support works for growing businesses that need strategy without adding a full-time executive.

When your business reaches the point where yesterday's bookkeeping no longer explains tomorrow's risk, you need CFO thinking.

That's especially true in Florida businesses dealing with seasonal swings, labor pressure, project timing, or industry-specific compliance. A fractional CFO gives you a forward-looking view. Not just what happened, but what happens next if you keep going the same way.

And yes, plenty of companies need one sooner than they think.

Frequently Asked Small Business Accounting Questions

Can I do my own small business accounting?

Yes, if the business is simple and you're disciplined. Simple means limited transactions, no inventory, minimal payroll complexity, and enough time each week to stay current.

The problem is that most businesses stop being simple before the owner admits it.

What's the most common accounting mistake?

Mixing personal and business transactions is high on the list. So is failing to reconcile monthly. Both create messy books, weak reporting, and tax-time pain.

The other big mistake is using accounting only to file taxes instead of using it to run the business.

Is a spreadsheet enough?

Usually not for long. Spreadsheets can track activity, but they're weak at workflow, audit trail, reconciliation, and consistent reporting. Once you've got regular payroll, recurring bills, customer invoices, or multiple bank and credit accounts, a spreadsheet becomes a bandage on a leaky pipe.

What's the difference between bookkeeping and accounting?

Bookkeeping is the recording. Accounting is the interpretation.

One keeps the score. The other helps you call the next play.

When should I hire professional help?

Hire help when one of these becomes true:

- You're behind and can't catch up without sacrificing operations

- You've added payroll and compliance risk just got real

- You don't trust your numbers enough to make hiring or pricing decisions

- You're growing and need forecasting, not just data entry

DIY vs. professional support

| Task | DIY Approach (Spreadsheet/Basic Software) | Professional Service (Bookkeeper/CPA/Fractional CFO) |

|---|---|---|

| Transaction coding | Often delayed or inconsistent | Structured, reviewed, and tied to reporting |

| Reconciliations | Easy to postpone | Performed on schedule with exception review |

| Payroll | Handled reactively | Processed with filings and supporting records |

| Tax readiness | Cleanup near deadlines | Ongoing preparation and documentation |

| Financial reports | Basic or ignored | Reviewed for trends, risks, and planning |

| Cash flow planning | Based on bank balance | Based on forecasts, timing, and obligations |

| Internal controls | Minimal | Approval workflows, access control, review process |

Is professional accounting a cost or an investment?

If you use it only to survive tax season, it feels like a cost. If you use it to improve pricing, manage cash, stay compliant, and avoid bad decisions, it's an investment.

That's the honest answer.

If you've been trying to figure out how to accounting for small business without turning your nights into unpaid bookkeeping shifts, get help. Clean books save time. Smart accounting saves businesses.

If your books are messy, your payroll process feels risky, or you need clearer financial direction, talk to Bookkeeping and Accounting of Florida Inc.. They provide bookkeeping, accounting, payroll, tax support, and fractional CFO guidance for growing Florida businesses that need accurate numbers and practical financial oversight.