Your receipts are in a drawer. Your bank feed is half-categorized. QuickBooks has that one account you're scared to click. Tax time is coming, and you're hoping your books are “close enough.”

That's not a system. That's a liability.

A proper bookkeeping format for small business isn't busywork. It's how you know whether you're making money, whether payroll is safe, whether sales tax and tax filings are headed for trouble, and whether your numbers can support a loan, a line of credit, or a smart hiring decision. Around Jacksonville, I see the same problem over and over. Owners work hard, sell well, and still fly blind because the books were built like an afterthought.

Bad books don't just create cleanup. They create bad decisions. If your reports are wrong, you'll trust the wrong margins, the wrong cash position, and the wrong tax picture. That's how good businesses get squeezed.

Beyond the Spreadsheet Why Your Bookkeeping Format Defines Your Success

A lot of owners think the format doesn't matter as long as income and expenses land somewhere. That's how you end up with a spreadsheet that made sense three months ago and now looks like a fishing net full of half-labeled transactions.

The bigger issue is fit. Most bookkeeping advice gives you generic steps, but it skips the central question: what format fits your business model? Guidance discussed by Wave's overview of small-business bookkeeping points out that most guides cover categorizing transactions and reconciling accounts, yet rarely address which format works for service firms, inventory-heavy retailers, or project-based construction. That matters because the SBA treats accounts receivable, accounts payable, cash, bank reconciliation, and payroll as separate functions someone has to manage. In plain English, your books need to match how your business operates.

Generic templates create specific problems

If you're a contractor, you need job costing logic. If you run a clinic, you need clean handling for payroll and vendor bills. If you sell products, inventory can't be an afterthought. A one-size-fits-all spreadsheet won't hold that together for long.

Here's what usually goes wrong:

- Revenue gets lumped together. You can't tell which service line or job type is carrying the business.

- Expenses are too broad. “Miscellaneous” becomes the largest account in the file. That's never a good sign.

- Payroll and contractor costs get mixed. That creates compliance risk and muddies your reporting.

- Reconciliations get skipped. Then nobody knows whether the numbers are real.

Practical rule: If your bookkeeping format can't answer basic questions fast, it's not a bookkeeping format. It's storage.

DIY is fine until it isn't

I'm not anti-spreadsheet. For a very small operation with low transaction volume, a simple system can work. But DIY bookkeeping has a shelf life. Once you add payroll, sales tax, recurring vendor bills, financing, or industry-specific reporting, “I'll clean it up later” turns into a year-end mess.

And that mess always costs more to fix than it would've cost to set up properly in the first place.

A clean format gives you control. A sloppy one gives you anxiety. That's the difference.

The Core Components of a Bulletproof Bookkeeping System

A solid bookkeeping system rests on three things. A chart of accounts that fits the business. The right accounting method. Clean separation between business and personal money. Miss any one of them, and the rest gets shaky fast.

Start with the chart of accounts

Your chart of accounts is the filing cabinet for your financial life. If the folders are wrong, every report that comes out of the system is wrong too.

For owners building or cleaning up a file, our walkthrough on how to set up a chart of accounts in QuickBooks is a useful starting point. If you also want a clearer sense of how reports roll up from those categories, this guide to balance sheet makers for SMBs is worth reviewing.

Here's a simple model for a service business.

Sample Chart of Accounts for a Small Service Business

| Account Type | Account Name | Example |

|---|---|---|

| Asset | Business Checking | Primary operating bank account |

| Asset | Accounts Receivable | Unpaid customer invoices |

| Asset | Equipment | Computers, tools, office equipment |

| Liability | Accounts Payable | Unpaid vendor bills |

| Liability | Credit Card Payable | Business card balance |

| Liability | Payroll Liabilities | Taxes and withholdings due |

| Equity | Owner's Equity | Owner investment and draws |

| Revenue | Service Income | Client service revenue |

| Revenue | Other Income | Interest or non-operating income |

| Expense | Payroll Expense | Employee wages |

| Expense | Contractor Expense | Payments to independent contractors |

| Expense | Rent | Office or facility rent |

| Expense | Software Subscriptions | QuickBooks, scheduling, industry tools |

| Expense | Marketing | Ads, website, promotions |

| Expense | Office Supplies | Small operating purchases |

That's simple on purpose. The right chart of accounts should be detailed enough to support decisions, but not so cluttered that nobody uses it correctly.

Choose cash or accrual on purpose

The technical fork in the road is cash vs. accrual accounting. Pilot's bookkeeping basics guide explains it plainly. Cash basis records income when received and expenses when paid. Accrual records them when earned or incurred, which is more useful for multi-period revenue and inventory analysis. The same guide notes that small-business guidance consistently recommends accrual once transactions become more complex, because it produces more decision-useful financial statements. It also mentions a common rule of thumb to set aside about 25% of income for estimated taxes.

My opinion is simple. If you have inventory, project billing, deferred revenue, or work that crosses periods, you probably need accrual or at least accrual-ready books. Cash basis is easier. Easier is not the same as better.

Clean books don't start with software. They start with the decision to classify transactions correctly from day one.

Separate the money

Never run business activity through your personal account if you can avoid it. Open a dedicated business bank account and business credit card. Use them consistently.

That separation does three jobs at once:

- It protects reporting quality. Fewer mixed transactions. Fewer guesses.

- It supports compliance. Tax prep gets cleaner when personal noise stays out.

- It saves time. Cleanup work drops when the source data isn't a mess.

If you're still paying business expenses from a personal debit card because it's “just easier,” stop. That habit creates confusion that shows up everywhere else.

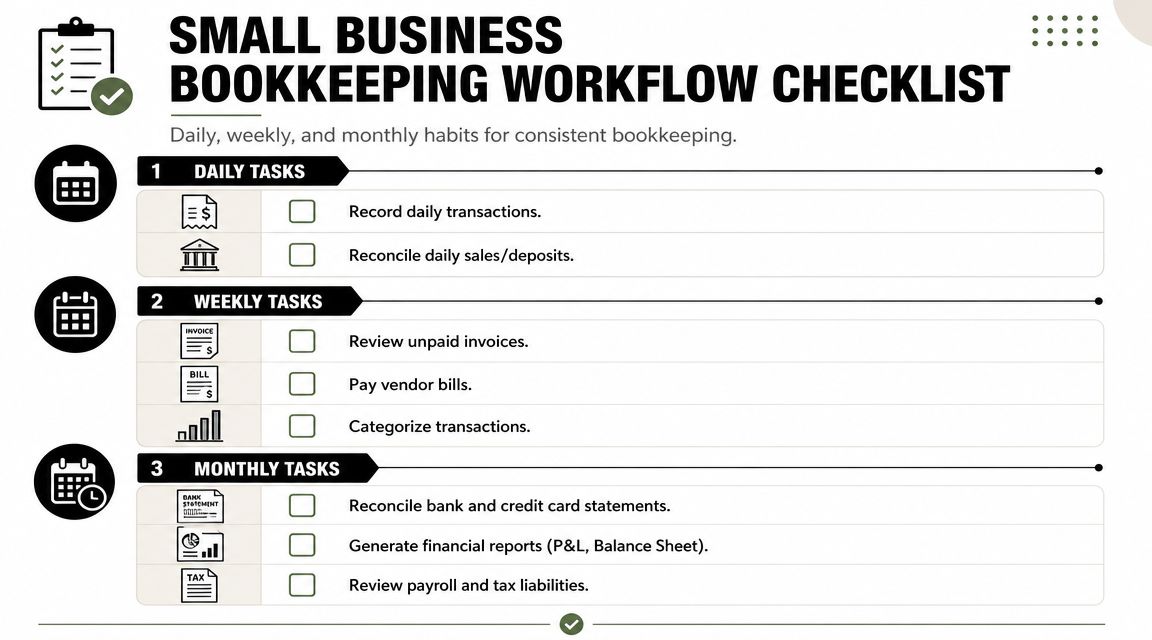

Your Daily Weekly and Monthly Bookkeeping Workflow

Bookkeeping falls apart when owners treat it like a seasonal chore. It works when it has rhythm.

A reliable bookkeeping format for small business usually follows a simple cadence. Coursera's small-business bookkeeping article notes that the double-entry system remains a foundational format, often paired with recording transactions weekly, reconciling regularly, and reviewing financial statements monthly. The same article explains that a small-business ledger often includes date, description, amount, and category, and that this structure supports the income statement, balance sheet, and cash flow statement.

That's the framework. Here's how to use it in actual situations.

Daily habits that prevent monthly pain

Most daily bookkeeping isn't glamorous. Good. It should be boring.

Use a simple routine:

- Capture receipts and invoices. Save them digitally the same day.

- Record sales and deposits. Make sure what hit the bank matches what happened in the business.

- Flag odd transactions. If you don't recognize a charge now, you definitely won't recognize it later.

If you want a practical view of how this cadence works in practice, our page on bookkeeping by day shows the kind of day-to-day discipline that keeps month-end sane.

Weekly review keeps the file honest

Weekly work is where most owners either stay in control or start drifting.

A good weekly session usually includes:

- Categorize transactions. Don't leave bank feed items hanging forever.

- Review unpaid invoices. If customers owe you money, your books should say so clearly.

- Pay vendor bills intentionally. Not late by accident. Not early without a cash plan.

- Check for duplicates or omissions. Both happen more than owners think.

This is also where the format itself gets tested. If your categories are confusing, weekly posting turns into guesswork. If your structure is clean, weekly bookkeeping is fast.

A week is short enough to remember what happened and long enough to keep the workload manageable.

Monthly close is where the numbers earn trust

Month-end is not just pressing “run report.” It's a short close process.

Use a checklist:

- Reconcile bank accounts

- Reconcile credit cards

- Review uncategorized or unusual entries

- Confirm accounts receivable and accounts payable

- Review payroll and tax-related balances

- Run reports and read them

The reports matter only if the data under them is clean. You want a monthly income statement that makes sense, a balance sheet that isn't stuffed with mystery balances, and a cash flow view that tells you whether operations are supporting the business or draining it.

A disciplined monthly close also makes quarterly tax work and year-end reporting far less painful. That's not exciting. It is profitable.

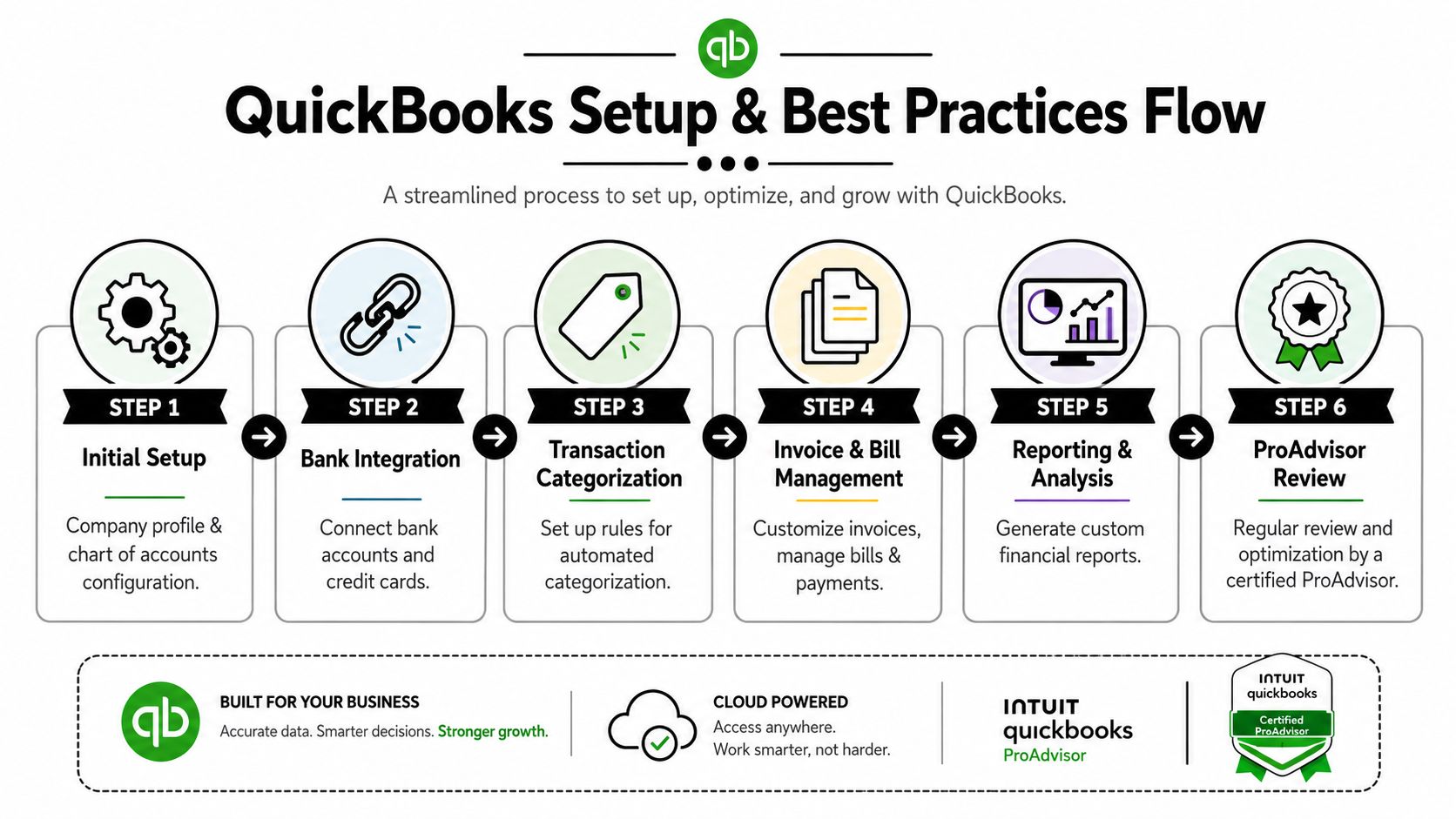

Leveraging Software QuickBooks Setup and Best Practices

QuickBooks is powerful. It is also very good at helping people make confident mistakes.

Most software problems aren't software problems. They're setup problems. The owner connects the bank, accepts default categories, never cleans up the chart of accounts, and assumes the dashboard is telling the truth. Then the books drift for months.

A sturdier workflow starts with the basics that QuickBooks' bookkeeping basics guide emphasizes: use a dedicated business bank account, customize the chart of accounts, record transactions weekly, reconcile statements monthly, and generate monthly reports. The same guidance flags missed entries, duplicate entries, and poor separation of payroll, contractor, and operating expenses as common bookkeeping errors. Those aren't minor glitches. They wreck reporting.

Right at the front end, this visual helps owners understand the flow.

Set up the file before you trust the reports

When I review a QuickBooks file, I look for a few things first:

- Bank and credit card connections that import cleanly

- A chart of accounts that matches the business instead of the software default

- Rules and automation that save time without misclassifying transactions

- Payroll mapping that doesn't dump everything into one bucket

- Contractor payments tracked separately from employee wages

If you want practical setup ideas, our page on QuickBooks tips and tricks covers common habits that keep the system usable.

Use automation carefully

Automation is great when the logic is right. It's dangerous when the logic is lazy.

For example, recurring bank rules can speed up coding for rent, software subscriptions, and regular vendor payments. But if a rule catches the wrong transaction, bad data spreads fast. The owner usually doesn't notice until a reconciliation fails or a report looks odd.

That's why review still matters. Software can help with speed. It can't replace judgment.

Here's a useful video resource for seeing bookkeeping software concepts in action.

Where a ProAdvisor or outside accountant saves real trouble

A certified ProAdvisor doesn't just click buttons for you. They set up the file so the reports mean something. That includes handling bank feeds correctly, building a chart of accounts that reflects your operation, and making sure payroll, contractors, loans, and owner activity are posted in the right places.

For Jacksonville businesses that need ongoing support, Bookkeeping and Accounting of Florida Inc. provides bookkeeping, accounting, payroll, tax support, and fractional CFO services, along with QuickBooks setup and maintenance. That kind of support is practical when the owner wants clean books without becoming the in-house bookkeeper by accident.

Software is a tool. If the setup is wrong, the reports are polished nonsense.

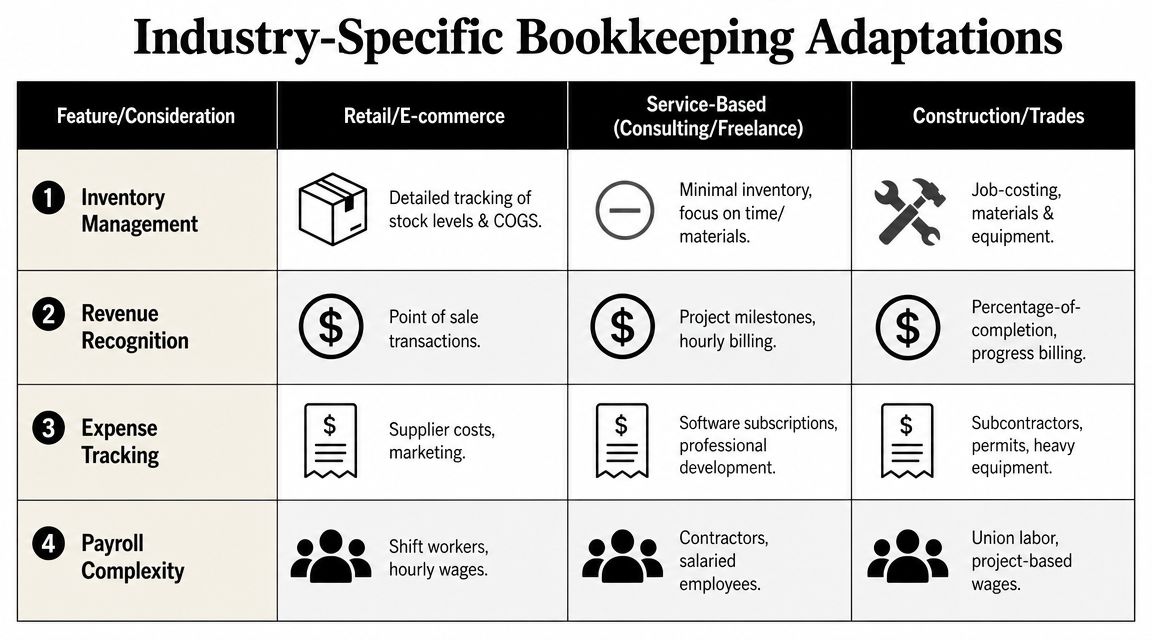

Adapting Your Bookkeeping Format for Your Industry

Generic bookkeeping advice usually runs out of gas. Instead, your format should match your operating model, not someone else's template.

Modern bookkeeping moved from manual recordkeeping to standardized digital systems, and that shift matters because bookkeeping now supports cash-flow visibility, tax readiness, and performance review through reports that can also handle payroll, sales tax, vendor bills, and reconciliations, as explained in Finaloop's small-business bookkeeping guide. That's useful because different industries need different reporting logic built into the same core system.

Construction and trades need job visibility

For contractors, the biggest issue is usually job costing. If materials, subcontractors, permits, equipment, and labor all land in broad expense accounts, you won't know which jobs made money and which ones just kept the trucks busy.

A construction-friendly format should do these things:

- Track income by project or contract

- Separate direct job costs from overhead

- Split payroll by job when possible

- Keep subcontractor costs distinct from employee wages

If the books can't show job-level profitability, the owner is estimating success from the checking account balance. That's a dangerous sport.

Retail and e-commerce need inventory discipline

Retail businesses have a different trap. Sales may look healthy while margins gradually erode because inventory tracking is sloppy.

The format has to reflect:

- Inventory movement

- Cost of goods sold

- Sales tax tracking

- Vendor bills and payment timing

Retail books break when owners treat product purchases like ordinary expenses and ignore the relationship between stock, margin, and cash. Good bookkeeping makes those connections visible.

Service businesses need clean revenue and labor reporting

Consulting firms, agencies, medical practices, and many local service companies don't need heavy inventory accounting, but they do need clarity around labor, collections, and recurring overhead.

A service-based format should focus on:

- Revenue by service line

- Accounts receivable

- Payroll and contractor separation

- Software and operating overhead categories

For healthcare in particular, clean bookkeeping supports better review of payroll, vendor costs, and cash flow. You don't want a provider making staffing decisions off books that blur everything together.

Nonprofits need accountability, not just categorization

Nonprofits carry a different burden. The issue isn't just whether the books balance. It's whether the format supports clear reporting, restricted activity handling, payroll oversight, and audit readiness where needed.

That means the bookkeeping structure should reflect the organization's reporting obligations and internal oversight needs, not just a standard small-business template.

The common theme is simple. The core bookkeeping logic stays recognizable, but the format has to adapt to what management needs to see. If your industry has operational complexity, your books should acknowledge it instead of pretending every business is the same.

Why Your Bookkeeper Is Your Most Valuable Advisor

A good bookkeeper doesn't just enter transactions. They protect the quality of every decision that follows.

Clean books are the raw material for tax planning, cash-flow management, budgeting, financing conversations, and owner compensation decisions. If the bookkeeping is weak, every downstream conversation gets weaker too. That's why I push owners to stop thinking of bookkeeping as clerical work and start seeing it as financial infrastructure.

Compliance is getting more complicated, not less

You asked for tax law changes, and here's the honest answer. Rules change. Filing requirements shift. State and federal obligations rarely get simpler. I'm not going to invent specifics that don't belong in this article, but I will tell you this: owners who rely on generic templates usually miss the operational details that keep them compliant.

That's where an experienced accountant and a fractional CFO earn their keep. One keeps the books clean and current. The other helps you use those books to make decisions before problems get expensive.

You don't hire financial help because things are easy. You hire it because mistakes in this area cost more than most owners realize.

Guidance beats guesswork

A lot of businesses don't need a full-time CFO. They do need someone who can read the numbers, spot weak points, help plan for taxes, and make sure the bookkeeping format supports growth instead of fighting it.

If you're evaluating support systems around your firm, even operational tools matter. For example, Eden's guide for accounting firms is a useful look at how accounting practices think about responsiveness and client communication. That matters because owners need answers quickly when payroll, taxes, or cash flow get messy.

The true value is peace of mind. Not fake peace of mind. Real peace of mind. The kind that comes from knowing the books are organized, reconciled, and reviewed by people who know what they're doing.

If your books are scattered, late, or built on guesswork, it's time to fix the foundation. Bookkeeping and Accounting of Florida Inc. helps Jacksonville and Northeast Florida businesses organize their bookkeeping, stay compliant, clean up QuickBooks, manage payroll, and get the strategic support of a fractional CFO without full-time overhead.