A Jacksonville business owner takes a payment in Bitcoin, feels pretty pleased for about ten minutes, then the accounting questions start. What was it worth when you received it? What happens if you held it before converting it to cash? What if you used part of it to pay a vendor, swapped it for another token, or parked it in a wallet and forgot about it until tax season?

That’s where the trouble starts. Most small businesses don't set out to become crypto businesses. A clinic might accept digital assets from a patient. A contractor might get paid that way by an out-of-state client. A nonprofit might receive a crypto donation. Suddenly, a routine bookkeeping job turns into a tax reporting problem with blockchain fingerprints all over it.

If that sounds familiar, you don't need a generalist. You need a crypto tax accountant who understands both business accounting and digital asset compliance.

The Crypto Tax Problem Every Florida Business Owner Faces

A lot of Florida business owners still think of crypto like cash with a shinier logo. The IRS does not. The IRS treats cryptocurrency as property, which means selling it, trading it, or spending it can create a taxable event. That one rule is the source of most of the confusion.

For a traditional business, this gets messy fast. A Jacksonville construction company accepts crypto for a large project deposit. The owner thinks, "We'll book it like any other payment." Not quite. The company now has to track the value when received, what happens while it's held, and whether a later sale or trade created gain or loss. If that same business uses the crypto to pay for equipment or converts it through an exchange, the recordkeeping multiplies.

Traditional businesses are the ones getting blindsided

Crypto-native companies expect complexity. Your average medical practice, subcontractor, retailer, or nonprofit doesn't. That's why so many owners get into trouble without realizing it.

According to a 2025 PwC survey, 18% of U.S. SMBs in non-tech sectors accepted crypto payments, a 40% increase from 2024, while only 12% felt confident in their tax reporting capabilities due to traditional CPA unfamiliarity with on-chain data, as summarized by OnChain Accounting. That's the gap in plain English. Adoption moved faster than compliance.

Why a regular accountant often isn't enough

A standard tax preparer is usually fine when your books are clean, your payment methods are boring, and your transactions fit neatly into known categories. Crypto doesn't behave that way.

A crypto tax accountant has to reconcile wallet activity, exchange records, basis history, and business books without guessing. If your company accepted crypto for services, held it, then used it later, each step matters. Miss one piece and your tax return can be wrong even if your bank account looks fine.

Practical rule: If your business touched crypto at any point, assume your books need review before your tax return gets filed.

That’s not fear talking. That’s experience.

What a Crypto Tax Accountant Actually Does All Day

A real crypto tax accountant doesn't spend the day plugging numbers into tax software and hoping for the best. The job is closer to forensic accounting with a blockchain trail.

Most of the work starts with reconstruction. We identify where the crypto came from, where it went, what the transaction was, and how it should be classified for tax reporting. On paper, a wallet transfer and a taxable disposition can look annoyingly similar until you trace the details.

The job is part detective work

Specialized crypto tax accountants use blockchain analytics tools such as TRM Labs to trace complex activity across wallets and protocols. That matters because over 80% of crypto audits in 2023 were triggered by unreported DeFi and staking income, and these tools can reduce reporting errors by up to 90% while helping produce an audit-ready Form 8949, according to TRM Labs training and certification materials.

That’s not a bookkeeping side quest. That’s technical tax work.

Here’s what a crypto tax accountant often has to sort out in practice:

- Wallet tracing: Following assets across personal wallets, business wallets, exchanges, and payment processors.

- Transaction classification: Deciding whether something was income, a sale, a trade, a transfer, staking revenue, or something else entirely.

- Basis tracking: Matching acquisition history to dispositions so gain or loss isn't guessed.

- Business book integration: Tying crypto activity back into QuickBooks and financial statements so your tax return matches your accounting records.

- Audit support: Preparing records that can stand up if the IRS asks questions later.

Classification is where most mistakes happen

Amateurs get cooked in such situations.

If your business receives staking rewards, those are generally treated as income when received. If you sold an NFT, that can create capital gain or loss and requires basis tracking. If a hard fork created a new asset and you gained control over it, that needs separate treatment from an airdrop. If your team participated in DeFi yield farming, you can't just toss the export into a spreadsheet and call it a day.

A good crypto tax accountant knows the difference between these categories and documents the logic behind each one. That's what keeps your return defensible.

If you can't explain what each wallet did, you can't file with confidence.

It's also systems work, not just tax work

The smartest accountants don't wait until March to untangle a year's worth of crypto chaos. They build a reporting system.

That can include crypto ledger software, exchange exports, wallet mapping, and integration with your bookkeeping platform so gains, losses, and income don't live in separate universes. If your business runs payroll, job costing, accounts payable, and monthly reporting, crypto can't sit off to the side like a weird hobby account. It has to be part of the financial system.

That’s why businesses that dabble in crypto usually wind up needing more than tax prep. They need accounting structure.

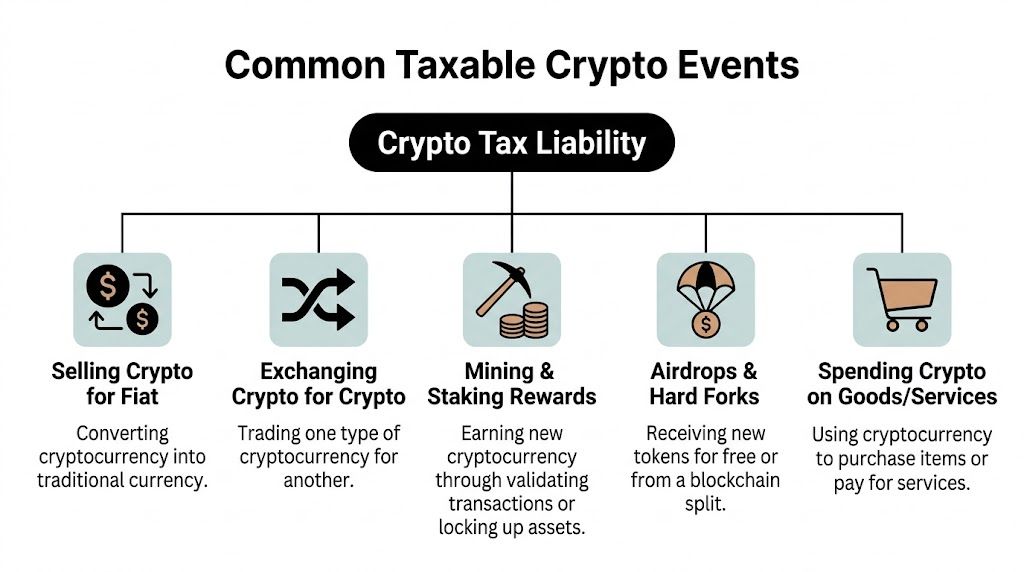

Your Guide to Common Taxable Crypto Events

The easiest way to think about crypto taxes is this: if your business did something with digital assets other than only move them between wallets it owns, there’s a good chance a tax event happened.

That doesn't mean every transaction is taxed the same way. It means you need to know which bucket it falls into. The buckets are where good reporting starts.

Selling and trading crypto

Selling crypto for dollars is the obvious one. You acquired property, later disposed of it, and now you measure gain or loss based on your basis and the value at sale.

Trading one token for another catches people off guard. Business owners say, "I didn't cash out, so I didn't realize anything." Wrong. Swapping Bitcoin for Ethereum is still a disposition, much like trading one piece of property for another. You gave something up, so tax reporting follows.

Here’s a simple table that helps:

| Activity | Tax issue to track | Why it matters |

|---|---|---|

| Sell crypto for cash | Gain or loss | Disposal of property |

| Swap one token for another | Gain or loss on the asset given up | Trade is still a taxable event |

| Use crypto to buy goods or services | Gain or loss on crypto spent | Spending property triggers tax consequences |

Spending crypto in the business

Using crypto to buy software, materials, travel, or contractor services feels like paying with money. Tax law treats it more like bartering with appreciated or depreciated property.

If your company received crypto at one value and later spent it when the value changed, that difference matters. So now you have the underlying business expense and a separate tax consequence tied to the crypto itself. That’s why "we just used it to pay a bill" isn't a real tax answer.

Income events that owners miss

Some crypto comes in through business activity instead of purchase. That often means income treatment upfront, before any later gain or loss enters the picture.

Common examples include:

- Staking rewards: Generally treated as income when received.

- Yield farming rewards: Also generally treated as income at fair market value upon receipt.

- Airdrops: If your business receives tokens and controls them, that can create income at receipt.

- Hard forks: New assets created by a blockchain split require separate analysis when control is established.

Records matter more than optimism. If your team doesn't track the date and value when assets hit your wallet, cleanup later gets ugly.

Owner advice: The phrase "free tokens" is usually followed by "tax problem" if nobody documented the receipt.

NFTs, mining, and oddball transactions

NFT activity has its own flavor of confusion. If your business bought an NFT, basis matters. If it sold one, gain or loss matters. If it accepted one in exchange for work or property, now you've got valuation and classification questions too.

Mining creates another layer. If your business earns crypto through mining activity, that can create income when received, and a later disposition creates a second tax event. One coin can trigger more than one tax consequence over its life. That's normal in crypto. Annoying, but normal.

A few other items deserve attention:

- Transfers between your own wallets usually aren't taxable by themselves, but they must be identified correctly so they aren't mistaken for sales.

- Exchange fees and transaction costs can affect reporting depending on the transaction.

- Mixed business and personal use is a mess. Separate wallets and records are not optional if you want clean books.

Why this overwhelms normal bookkeeping

Most bookkeeping systems were built around bank feeds, invoices, checks, and merchant processors. They were not built to interpret on-chain events.

That’s why business owners who are perfectly capable in every other area get stuck here. The problem isn't intelligence. The problem is that crypto creates layers of tax treatment that standard accounting workflows don't catch on their own.

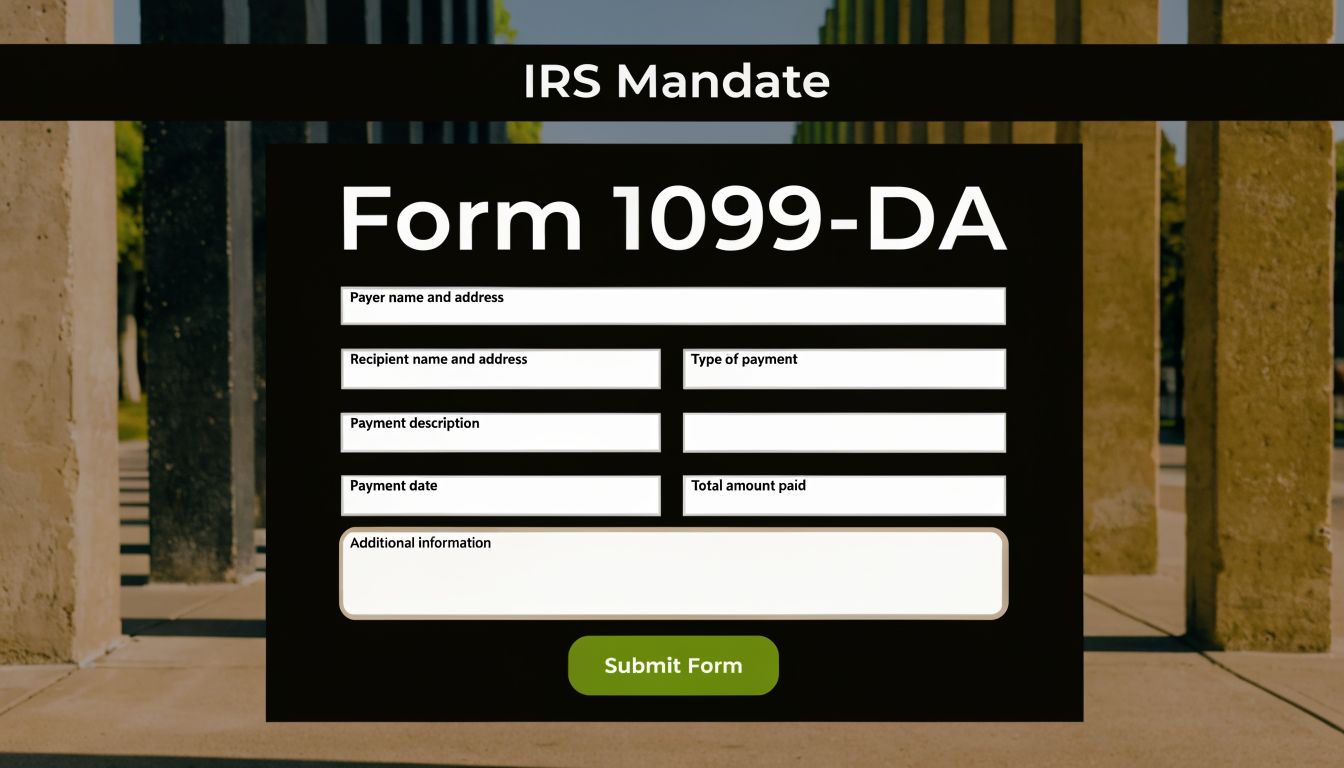

New IRS Rules for 2026 You Cannot Ignore

The loosey-goosey era of crypto reporting is ending. The IRS is getting more visibility, and business owners who are still winging it are going to have a bad time.

Starting with the 2025 tax year, brokers must issue Form 1099-DA reporting gross proceeds from digital asset sales, which gives the IRS much clearer visibility into crypto activity, according to Public's summary of U.S. crypto tax rules.

What Form 1099-DA changes for your business

For years, many taxpayers operated as if crypto was invisible unless they volunteered the information. That was never a smart assumption. Now it’s even worse.

Form 1099-DA puts digital asset reporting closer to the stock brokerage world. The IRS gets data it can compare against your return. If your business reports one thing and broker reporting shows another, you've handed the agency a reason to ask questions.

For the transition year, cost basis reporting is optional for brokers. After that, basis reporting becomes more important for assets bought after the start of 2026. Translation: if your records are sloppy now, they won't magically improve later.

A plain-English overview of crypto tax reporting requirements is helpful if you want a broader refresher before sitting down with your accountant.

This is where bad records turn expensive

Businesses don't get in trouble only because they intended to hide something. Plenty get in trouble because the books were incomplete, wallet records were scattered, and nobody reconciled the crypto activity to the tax return.

That can affect more than Form 1099-DA. Businesses may also need accurate reporting for other tax forms connected to dispositions and income recognition. If your books don't support the numbers, you're exposed.

Here’s the practical problem:

- Broker data isn't the whole story: A 1099-DA may show proceeds, but your business still needs basis and classification.

- Wallet activity can sit outside broker reports: Internal records still matter.

- One bad assumption spreads: If accounting, tax prep, and crypto reports don't align, the return becomes harder to defend.

For a quick walkthrough of the reporting environment, this video gives useful background before you start gathering records:

The tax rates are not trivial

If your business or its owners are dealing with gains, the rates aren't something to shrug off. The source above notes that short-term crypto gains are taxed at ordinary income rates, ranging from 10% to 37%, while long-term gains are taxed at 0%, 15%, or 20% depending on income thresholds. That spread is one reason holding period and basis tracking matter so much.

The serious part is simple. The IRS has increased enforcement around crypto noncompliance, and underreporting can lead to penalties, interest, audits, and in severe cases even criminal investigation. You don't need drama. You need records.

How to Choose the Right Crypto Tax Accountant in Jacksonville

A business owner in Jacksonville doesn't need an accountant who says, "Sure, I can probably handle crypto." You need one who has already dealt with ugly records, missing basis, multi-wallet activity, and business bookkeeping that has to tie back to the tax return.

Most firms can prepare a return. Fewer can defend the numbers on it.

Start with one hard question

Ask this first: How do you handle missing cost basis?

That question distinguishes the specialists from the tourists. A 2025 CoinTracker report found that 65% of SMBs with pre-2023 crypto have incomplete records, creating risk of overpaying capital gains tax and penalties up to $250,000, as discussed by Count On Sheep. If the accountant's answer is basically "we'll use what you have," keep walking.

A qualified crypto CPA should be able to explain how they reconstruct transaction history, identify wallet ownership, and document assumptions for audit defense.

The checklist that actually matters

Use this when you're interviewing a crypto tax accountant:

- CPA credentials: If the work affects your business return, financial statements, and audit exposure, don't hand it to a hobbyist.

- Forensic ability: Ask how they rebuild records from old exchanges, wallet transfers, and incomplete exports.

- Business accounting knowledge: Crypto is only part of the picture. Your accountant should understand payroll, job costing, vendor payments, and financial reporting.

- Software fluency: They should be comfortable with crypto ledger platforms and with integrating results into QuickBooks.

- Entity awareness: A business isn't taxed like an individual investor. The accountant should speak clearly about business reporting, not just personal gains.

- Documentation habits: Ask what workpapers they keep if the IRS questions the filing later.

Here’s a blunt comparison:

| Weak hire | Strong hire |

|---|---|

| Says crypto is "basically like stock" | Explains where crypto treatment differs in practice |

| Relies only on exchange CSVs | Reconciles exchanges, wallets, and books together |

| Prepares returns once a year | Builds a process for year-round tracking |

| Doesn't ask about internal controls | Wants to know who approves wallets, transfers, and entries |

Local experience matters more than people admit

Jacksonville businesses have normal business problems plus crypto problems. Construction companies need job costing. Healthcare groups need clean books and reliable reporting. Nonprofits need compliant records. If your accountant only understands tokens and doesn't understand operating businesses, you'll still have a mess. Just a more expensive one.

If you want a useful framework for evaluating a professional more broadly, this guide on how to find a good accountant is worth reading before you sign an engagement letter.

The right accountant should make your records clearer, not your explanations longer.

Ask about the engagement model

Some businesses need a one-time cleanup because crypto activity was limited. Others need ongoing monthly oversight because they continue accepting or holding digital assets.

The accountant should be able to offer more than return preparation. Ask whether they can help with:

- monthly reconciliation,

- QuickBooks integration,

- tax planning before year-end,

- policy setup for wallet use,

- and support if an IRS notice arrives.

If they only want the data two weeks before the deadline, they aren't solving the problem. They're just postponing it.

Why Your Business Needs a Financial Guide Not Just a Tax Preparer

A tax preparer looks backward. A financial guide looks forward. That's the difference.

If your business has crypto in the mix, even occasionally, the problem isn't just filing the return correctly. The problem is building a system so the return is correct because the books, controls, and decisions were right all year.

Tax prep is reactive, guidance is proactive

A reactive preparer asks for reports after the year is over. A strategic advisor asks better questions much earlier.

What happens if your business accepts crypto and the value drops before payroll is due? How are you recording receipts in the books? Who approves wallet transfers? Are you converting to dollars immediately or holding digital assets on purpose? If you're doing any of that without a policy, you're not managing risk. You're improvising.

That’s why many businesses need broader financial leadership, not just tax compliance. A good overview of fractional CFO services helps explain how this kind of support works for companies that need senior guidance without adding a full-time executive.

A fractional CFO sees the whole field

Crypto shouldn't be a side spreadsheet maintained by whoever had free time on Friday. It should fit into cash flow planning, internal controls, month-end close, and management reporting.

A fractional CFO helps a business decide things like:

- When to convert crypto receipts: To protect liquidity and avoid surprise volatility in operating cash.

- How to structure bookkeeping: So receipts, gains, losses, and expenses flow into the right accounts.

- Who controls access: Because bad wallet controls create accounting issues and operational risk.

- What to review monthly: So tax problems don't pile up until year-end.

Bottom line: If you only hire someone to file forms, you’ll keep paying to clean up preventable mistakes.

Most owners don't know what they don't know

That’s not an insult. It’s reality.

Owners already have enough on their plate. They’re running crews, seeing patients, handling vendors, chasing receivables, and trying to grow. Expecting them to also understand digital asset basis tracking, income classification, and reporting workflows is unrealistic. Smart owners get help before the mess hardens into a penalty letter.

The best financial support doesn't just keep you compliant. It helps you make cleaner decisions.

Crypto Tax FAQs for Florida Business Owners

Florida business owners ask good questions about crypto. The problem is they usually ask them after the transactions already happened. Here are the ones that come up most often.

We accepted crypto once. Do we really need special accounting

Yes, if you still have the records and want the reporting done properly.

One crypto payment can create multiple accounting entries depending on what happened next. Receipt of the asset, later sale, later spending, or a transfer through another platform can all affect the reporting trail. If the amount was minor and the activity ended there, the cleanup may be manageable. But "it was only one payment" has started many unpleasant reconciliations.

What if our records are incomplete

Then reconstruction comes first. Filing comes second.

Start by gathering exchange exports, wallet addresses, internal invoices, payment processor records, and any emails or contracts tied to the transaction. A crypto tax accountant can use those pieces to rebuild what happened. Guessing is a terrible policy. The IRS is not known for rewarding creative memory.

Are transfers between our own wallets taxable

Usually, moving assets between wallets you own isn't itself a taxable event. The problem is proving that the transfer was internal and not a sale, payment, or exchange.

That’s why wallet mapping matters. If your records don't show ownership and transaction purpose, innocent transfers can look taxable during cleanup.

What about Florida taxes

Florida business owners need to think beyond federal return preparation. State-level compliance, sales tax issues in the right context, and general bookkeeping accuracy still matter. Crypto doesn't replace normal accounting obligations. It adds a new layer on top of them.

For businesses already juggling online transactions, multichannel sales, and digital payments, crypto often joins a broader compliance stack rather than standing alone.

Should we keep crypto on the books or convert it right away

That depends on your cash flow, risk tolerance, and internal controls.

Some businesses convert quickly because they want predictable liquidity and simpler reporting. Others hold certain amounts as part of a treasury strategy. The wrong move is having no policy at all. If your team handles crypto differently every time, your books and tax reporting will drift.

Can QuickBooks handle crypto by itself

No, not by itself in the way most owners hope.

QuickBooks is excellent for core bookkeeping, but crypto classification and basis tracking usually require supporting tools, clean imports, and professional review. The accounting system is part of the answer, not the whole answer.

What should we do before year-end

Do these five things:

- List every wallet and exchange your business used.

- Separate business and personal activity if anyone blurred the lines.

- Export transaction data before platforms change access or formatting.

- Match crypto activity to invoices and payments so the books tell the same story.

- Get a review before filing season instead of dumping it all on your preparer at the last minute.

Clean records in December cost less than reconstruction in March.

Secure Your Business Your Next Step Toward Crypto Compliance

Crypto tax isn't a niche issue anymore. Traditional Florida businesses are running into it through payments, holdings, donations, and side ventures. The tax treatment is technical, the reporting burden is growing, and the cost of sloppy records is real.

If your company touched crypto, don't treat it like an afterthought. Treat it like what it is: a business accounting and compliance issue that needs proper controls, clear records, and informed judgment.

That matters even more when crypto sits alongside the rest of your obligations. If you're also dealing with ecommerce or multistate selling, resources on internet sales tax compliance can help you understand how digital transactions create overlapping responsibilities. And if your paper trail is part of the problem, this guide on how to organize receipts for taxes is a smart place to tighten up your records.

The simple recommendation is this. Don't wait for an IRS notice to force you into getting organized. Get the books cleaned up, get the crypto classified correctly, and get a real advisor involved before the next filing deadline.

If your Jacksonville or Northeast Florida business needs help sorting out crypto transactions, cleaning up the books, or getting higher-level financial guidance, talk to Bookkeeping and Accounting of Florida Inc.. The team helps business owners get compliant, stay organized, and make decisions with numbers they can trust.