You’re good at what you do. You build homes, run crews, see patients, process claims, manage donors, keep shelves stocked, and solve problems all day. Then you open QuickBooks, stare at payroll tax notices, wonder why revenue looks fine but cash feels tight, and realize your “financial plan” is basically checking the bank balance and hoping nothing catches fire.

That’s not a plan. That’s a stress response.

For Jacksonville business owners, real financial planning jacksonville advice should help you run a company, not just prepare for retirement. If your accountant only shows up at tax time, if your reports are late, or if nobody can tell you what next quarter looks like, you don’t have financial leadership. You have paperwork.

Why Your Jacksonville Business Needs a Real Financial Plan

If you own a construction company, medical practice, trade business, or nonprofit in Northeast Florida, you’ve probably already noticed something annoying. Search for financial planning jacksonville and you’ll get a parade of retirement talk, wealth management pages, and polished advice for high-net-worth households. That’s fine for retirees. It’s useless when you’re trying to make payroll, price jobs, manage reimbursements, and stay compliant.

That gap is real. Existing content on “financial planning Jacksonville” largely targets high-net-worth individuals and retirees, while SMBs make up 99.8% of businesses in the area and often need help with job-costing, payroll compliance, and cash-flow volatility, as noted by JL Smith Group’s Jacksonville financial planning page.

Growth creates financial mess faster than most owners expect

A lot of Jacksonville owners hit the same wall. Sales are up. Work is coming in. The team is bigger than it was a year ago. But nobody tightened the accounting process as the business grew. So estimates live in one system, payroll in another, receipts in glove compartments, and tax deadlines on somebody’s memory. That works right up until it doesn’t.

A real financial plan does four things:

- Shows where profit comes from. Not where you think it comes from.

- Protects cash so growth doesn’t strangle the business.

- Keeps you compliant with payroll, sales tax, reporting, and filing requirements.

- Helps you decide faster because your numbers stop lying to you.

Tax planning is part of operating, not a year-end scramble

A lot of owners still treat taxes like a once-a-year cleanup project. That’s how you get ugly surprises, missed deductions, late filings, and avoidable penalties. Tax law changes, filing thresholds, payroll obligations, and reporting requirements don’t wait for you to “get organized later.”

Practical rule: If your business decisions don’t show up in your accounting system correctly and on time, you’re running blind.

Jacksonville’s economy rewards businesses that can scale cleanly. The winners aren’t always the biggest operators. They’re the ones with current books, reliable forecasting, and somebody watching compliance before it becomes expensive.

Your expertise isn’t the issue

Most owners don’t struggle because they’re careless. They struggle because they built a business around operations, not around finance. That’s normal. A roofer should know roofing. A clinic owner should know patient care. A nonprofit director should know programs and funding.

But every one of them still needs a real financial plan. Not generic advice. Not retirement brochures. Actual operating guidance for a Jacksonville business that wants to grow without getting buried in tax notices, cash crunches, and preventable chaos.

Assess Your Financial Health Beyond the Bank Balance

If the only number you check is what’s in the bank, you’re making decisions with a blindfold on. The bank balance tells you one thing. It does not tell you whether the business is profitable, whether bills are stacking up, or whether next month’s payroll is already spoken for.

Plenty of owners feel “fine” because cash is sitting in the account today. Then a sales tax payment clears, payroll hits, a vendor invoice lands, and suddenly the month looks a lot less charming.

The three reports that actually matter

Think of your financials as three different camera angles on the same business.

Profit and loss

Your profit and loss statement, or P&L, shows income and expenses over a period of time. It answers a basic question. Did the business generate profit from operations?

That sounds simple, but owners misuse this report constantly. They glance at revenue, skim expenses, and call it done. A useful P&L shows trends by month, expense categories that are drifting, gross margin pressure, and whether rising sales are turning into profit. If you want a plain-English breakdown, this guide on understanding profit and loss statements does a good job of showing what owners should look for.

Balance sheet

The balance sheet tells you what the business owns, what it owes, and what’s left over. Sloppiness often lurks in its figures. Old receivables stay on the books too long. Loans get misclassified. Equipment sits there with no one reviewing how it’s being tracked. Payroll liabilities pile up if nobody reconciles them properly.

A messy balance sheet creates fake confidence. It can make the company look stronger than it is, or weaker than it is. Neither helps.

Cash flow statement

The cash flow statement answers the question owners care about most. Where did the cash go?

This report is the reality check. A retailer can show a profit on the P&L and still struggle to pay suppliers because cash is tied up in inventory or receivables. A clinic can look healthy on paper while waiting on reimbursements. A contractor can land profitable jobs and still feel squeezed because labor and materials hit before collections arrive.

Profit is not cash. Owners who forget that usually relearn it on a bad Tuesday.

Clean books are not optional

Reports are only as good as the bookkeeping underneath them. If transactions are coded wrong, bank accounts aren’t reconciled, payroll entries are incomplete, or loans are sitting in random categories, your reports are decoration. They might look official. They won’t help you decide anything.

Here’s what solid bookkeeping should produce every month:

- Current reconciliations so your bank and credit card balances match reality

- Accurate expense coding that supports tax prep and management decisions

- Timely loan and liability tracking so obligations don’t get buried

- Reliable reporting you can use before the month is ancient history

Expertise has obvious value in Jacksonville

The Jacksonville market puts a high premium on financial expertise. In the Jacksonville metro area, financial advisors earn an average salary of $120,130, which is over 131% higher than the median for all workers, according to SmartAsset’s analysis of BLS data. That doesn’t mean every business needs a personal wealth manager. It means serious financial guidance has clear value in this market.

Owners who resist professional bookkeeping usually say the same thing. “We’re saving money.” Usually they’re saving pennies and losing dollars. Bad data leads to bad pricing, bad hiring, bad tax planning, and bad timing. That’s not frugality. That’s expensive confusion wearing a discount name tag.

A quick self-check

If you answer “no” to any of these, your financial health needs attention:

| Question | What it reveals |

|---|---|

| Do you get monthly financials on time? | Whether you’re managing proactively or looking in the rearview mirror |

| Can you explain why cash changed this month? | Whether cash flow is under control |

| Do you trust your receivables and payables reports? | Whether your balance sheet is usable |

| Can you see profit by job, service line, or program? | Whether pricing and operations are grounded in facts |

The bank balance is a symptom. Your reporting system is the diagnosis. If you want smart financial planning jacksonville businesses can use, start with the numbers underneath the decisions.

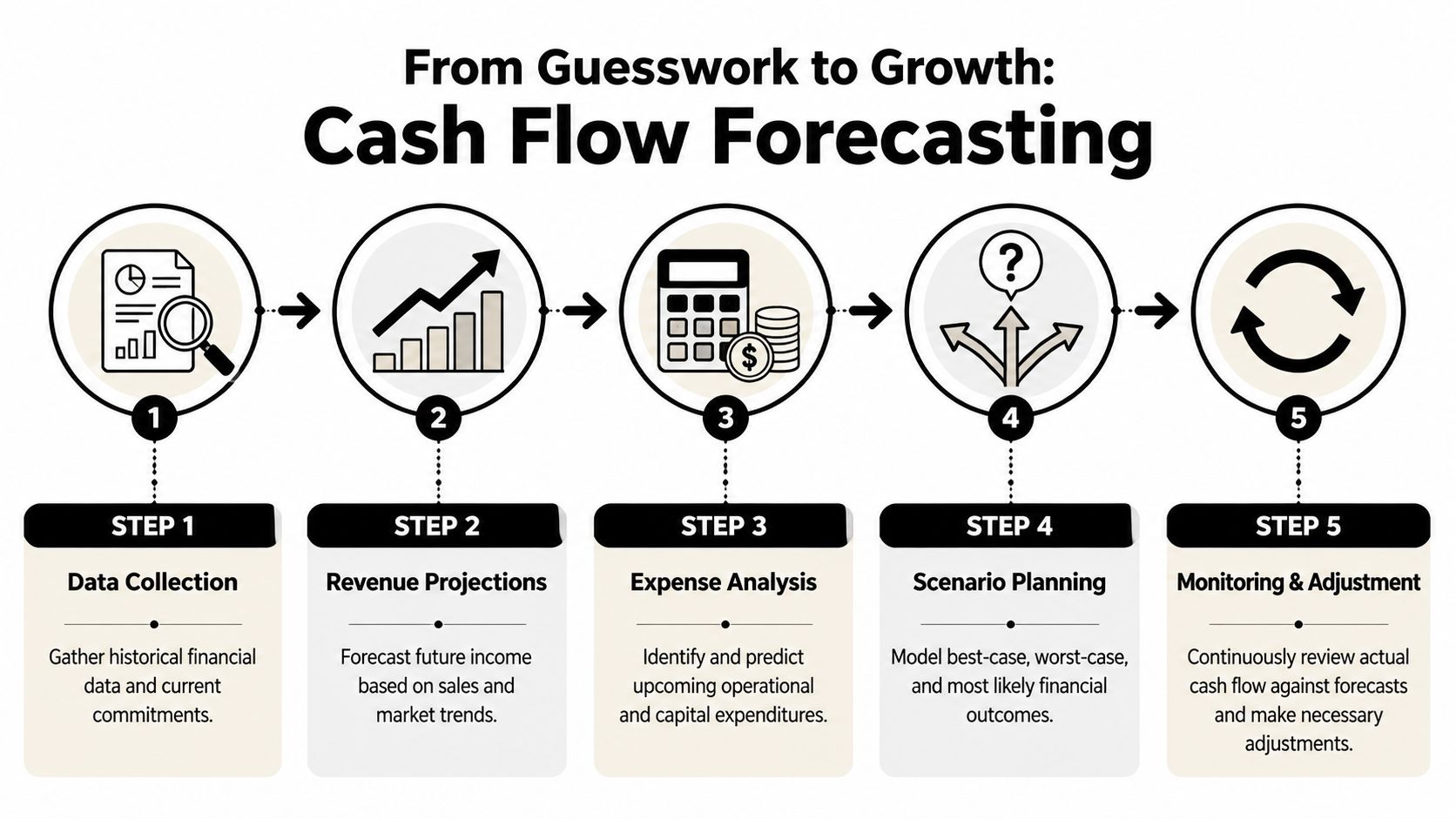

From Guesswork to Growth A Guide to Cash Flow Forecasting

Most budgets are dead on arrival. They get built once, saved somewhere, ignored for months, and dragged back out when the owner wants to know why cash is disappearing. That’s not forecasting. That’s archaeology.

A useful cash flow forecast is alive. It changes as collections shift, costs rise, jobs start late, reimbursements drag, or owners decide to buy equipment at exactly the wrong moment.

Stop budgeting like last year still matters

A static annual budget can be helpful, but it won’t save you when reality changes in April. A 12-month rolling cash flow forecast is better because you keep updating it. Every month, you add a new month at the end and compare actual results to what you expected.

That’s how you spot trouble early. It’s also how you spot opportunity before the bank account fools you.

Build a forecast you’ll actually use

Start with history

Pull prior months from QuickBooks or your accounting system. Look at revenue timing, payroll runs, recurring subscriptions, debt payments, rent, taxes, and owner draws. If the data is a mess, fix that first. Garbage in, garbage out still applies.

Forecast collections, not just sales

Revenue on an invoice doesn’t pay payroll. Collections do.

A Jacksonville medical clinic may bill today and wait through a long reimbursement cycle. A construction company may front labor and material costs before receiving progress payments. A retailer may have strong sales during one season and feel the slowdown right after. Model when cash arrives, not when a sale is booked.

Map every major outflow

List fixed costs first, then variable costs, then irregular expenses. Insurance renewals, annual software fees, equipment purchases, permit costs, payroll tax deposits, and debt payments should all be visible. If they “surprise” you every year, that’s not a surprise. That’s poor process.

Run scenarios

Build three views:

- Base case based on current expectations

- Tight case if collections slow or expenses hit early

- Strong case if work closes faster than expected

Forecasting thereby transforms into management rather than mere bookkeeping. If hurricane season drives extra prep costs for a contractor, model that. If a clinic expects reimbursement delays, model that too. If a nonprofit is waiting on grant funding, don’t pretend the cash already exists.

Review and update monthly

A forecast is only useful if someone compares forecast to actual results and adjusts. If labor costs are drifting, update future months. If receivables are slower, move collections out. If inventory is higher than planned, show the impact on cash.

For a practical companion resource, Resolut on cash flow management offers a good overview of why forecasting matters operationally, not just financially.

Use guardrails so emotion stops driving decisions

Many owners make cash decisions emotionally. They feel rich after a good month and spend too fast. Then a slow month arrives and everybody panics. That’s amateur hour.

A better system uses thresholds. The Guardrails Approach can push success rates to over 95% compared with static rules by setting triggers for spending changes. Applied to a business, that means cutting costs by 10% if cash reserves fall 20% below target, or increasing strategic investment when reserves rise 20% above target, based on Wealthtender’s explanation of the guardrails approach.

Set cash rules before you need them. Owners make better decisions when they’re calm than when they’re cornered.

Here’s what business guardrails can look like:

| Cash reserve status | Action |

|---|---|

| Below target range | Freeze discretionary spending and review payroll, purchasing, and owner draws |

| Within target range | Keep operations steady and monitor forecast variance |

| Above target range | Consider debt reduction, equipment investment, hiring, or strategic marketing |

Forecasting works best when it’s tied to operations

A forecast shouldn’t live in accounting alone. It should connect to what’s happening in the field, in the clinic, in purchasing, and in hiring. If your estimator closes a large job, your forecast changes. If a doctor adds a provider, your forecast changes. If a major donor payment is delayed, your forecast changes.

For owners who want a deeper how-to, this walkthrough on forecasting cash flow is a solid next step.

The whole point of financial planning jacksonville businesses need isn’t to produce pretty spreadsheets. It’s to stop guessing. Guessing is expensive. Forecasting is how you keep control.

Financial Planning for Jacksonville's Key Industries

Generic advice is easy to write and useless to apply. Jacksonville businesses don’t all run the same way, and the companies that get into trouble usually do so in industry-specific ways. Construction companies bleed profit through weak job costing. Healthcare practices get squeezed by reimbursement timing and equipment decisions. Nonprofits can look stable until restricted funds and reporting obligations collide.

That’s why financial planning jacksonville businesses need has to fit the work being done.

Construction and trades need job-level visibility

A Jacksonville contractor can stay busy all year and still not know which jobs are profitable. That happens when labor gets lumped together, materials aren’t tracked carefully, subcontractor costs drift, and change orders don’t get tied back to project profitability. The owner thinks the company is growing. In reality, one or two bad jobs are eating the margin.

A better setup starts with disciplined job costing. Every major cost should be tied to the right project and reviewed while the work is still underway. Waiting until year-end to figure out whether a job made money is like checking your parachute after landing.

Mini case example for a contractor

A trades company takes on more work after a busy rebuilding period. Revenue looks healthy. The owner assumes the business is doing great. Then payroll pressure rises, vendor balances creep up, and one “good” job turns out to be much less profitable than expected because labor hours ran over and materials were underpriced.

The fix isn’t glamorous:

- Track labor by job so overtime and crew allocation are visible

- Separate materials and subcontractor costs instead of dumping them into broad categories

- Review work in progress regularly so retainage and billing timing don’t distort the picture

- Tie estimates to actuals so future pricing gets smarter

For companies that need help at the estimating stage, Exayard construction estimating software is one example of a tool that can support tighter front-end controls. Software alone won’t save a bad process, but the right system makes disciplined pricing easier.

A contractor doesn’t go broke because they were busy. They go broke because they were busy on work they didn’t price, track, or bill well.

Construction also creates payroll headaches fast. Different crews, overtime, prevailing requirements on some work, reimbursements, owner draws, and timing gaps between project costs and customer payments can turn payroll into a compliance minefield. If payroll entries and job coding aren’t clean, the reports become fiction.

Healthcare practices need patience and precision

Healthcare accounting has its own flavor of chaos. A clinic can show production, appointments, and patient demand, then still feel cash pressure because collections don’t arrive in the same pattern as expenses. Insurance reimbursement cycles don’t care when payroll is due.

That means a healthcare practice needs tighter coordination between billing, bookkeeping, and planning than many other businesses.

Mini case example for a clinic

A growing clinic adds staff and equipment because patient demand supports expansion. On paper, the move makes sense. But reimbursement timing stretches, old receivables stay unresolved, and the practice starts relying on current cash to cover decisions made months earlier.

The right response looks different from construction:

- Watch aging receivables closely so old claims don’t sit there pretending to be assets

- Plan capital purchases carefully because equipment affects both cash and reporting

- Coordinate payroll and reimbursement cycles instead of hoping they line up

- Keep financial systems organized and access-controlled so sensitive operations stay orderly

Healthcare owners also need cleaner chart-of-accounts design than they usually get. If provider compensation, supplies, equipment costs, and billing adjustments all land in vague categories, the owner can’t see what’s happening by service line or provider group. Then they make staffing and purchasing decisions based on instinct.

Nonprofits need reporting that respects restrictions

Nonprofits in Jacksonville face a different trap. Leadership often focuses heavily on mission, which is right, but sometimes neglects the structure needed to support the mission. Restricted funds, grant reporting, board reporting, payroll, and audit readiness can get messy fast if nobody sets up the accounting system properly.

A nonprofit doesn’t need flashy financial theory. It needs clean reporting, timely reconciliations, and somebody who understands that compliance is part of credibility. If reporting falls apart, donor confidence usually follows.

One-size-fits-all accounting is where trouble starts

The reason so many owners feel frustrated with financial planning jacksonville searches is simple. They’re getting broad household advice when they need operating guidance tied to their industry.

Construction needs job costing. Healthcare needs reimbursement-aware cash planning. Nonprofits need disciplined reporting and compliance. Retail needs inventory awareness and seasonal planning. Startups need runway clarity and clean books before they try to borrow or raise capital.

A generic accountant may still file a return. That’s not the same as helping the business run better.

Staying Compliant A Jacksonville Business Tax Calendar

Most small businesses don’t get in trouble because they meant to ignore compliance. They get in trouble because nobody owned it clearly. One filing gets missed. A payroll deposit is late. Sales tax is handled inconsistently. Local registrations expire. Then the owner gets a notice and acts shocked, as if the government is known for its sense of humor.

Compliance is part of cash flow management. Missed deadlines create penalties, penalties strain cash, and strained cash creates even worse decisions.

Why this matters more than owners think

A U.S. Bank study found that 68% of small businesses fail due to poor cash flow management, and a proactive roadmap with a CPA can improve cash reserves by 25%, according to the summary provided by HCP Wealth Planning. That’s a blunt reminder that tax mistakes are not isolated admin issues. They hit the same cash reserves your business needs to survive.

The calendar every owner should maintain

You need one master compliance calendar that covers federal, state, and local obligations. Not three calendars. Not sticky notes. Not “my office manager usually handles that.” One system.

Here’s a practical framework for Key 2026 Tax & Compliance Deadlines for Jacksonville SMBs.

| Deadline | Task | Governing Body |

|---|---|---|

| Monthly or assigned filing frequency | File and remit Florida sales and use tax if applicable | Florida Department of Revenue |

| Quarterly | File federal estimated tax payments if required by entity and owner structure | Internal Revenue Service |

| Quarterly | File federal payroll tax returns and remit related obligations | Internal Revenue Service |

| Quarterly | File Florida reemployment tax reports | Florida Department of Revenue |

| Annually | Issue wage and contractor information forms as required | Internal Revenue Service and Social Security Administration |

| Annually | Renew local business tax receipt if required for your operation | Local city or county authority |

| Annually | File federal business income tax return by applicable entity deadline or extension date | Internal Revenue Service |

What owners commonly miss

Sales tax isn’t optional just because it’s confusing

If your business has taxable sales, somebody must determine what’s taxable, collect correctly, and file on time. “We thought our system handled it” is not a defense. It’s an admission.

Payroll compliance goes beyond cutting checks

Running payroll means withholding, depositing, reporting, and reconciling. If those pieces don’t tie together, notices follow. And if officer compensation, contractor classification, or benefit treatment is sloppy, the cleanup gets ugly.

Local requirements still count

A surprising number of business owners focus only on federal taxes and ignore local registrations and renewals. That’s how avoidable problems start. A business tax receipt sounds boring until you need one and don’t have it.

Compliance works best when it’s scheduled, assigned, and reviewed before deadlines arrive.

Tax law changes require actual monitoring

Tax law changes don’t announce themselves politely. Rules shift, forms change, thresholds move, and filing obligations can change with the business itself. If your company has grown, added staff, opened another location, changed entity structure, or expanded services, your tax process may need to change with it.

That’s why owners need a current compliance calendar and someone watching it. Not after the notice arrives. Before.

Why Every Growing Business Needs a Fractional CFO

At some point, bookkeeping alone stops being enough. A bookkeeper records what happened. That matters. But growing companies also need someone who helps decide what should happen next. That’s the difference between reporting history and managing the future.

That’s where a fractional CFO comes in.

Strategic guidance isn’t a luxury in Jacksonville

Jacksonville has a serious financial ecosystem. Mercer Advisors held $928 million in local assets as of March 31, 2026, based on its Jacksonville expansion announcement. The takeaway for business owners is simple. Strategic financial guidance is standard practice for people and organizations that take growth seriously.

SMBs shouldn’t assume high-level financial leadership is only for large companies. That thinking keeps owners stuck too long in operator mode. You can be excellent at sales, service, and operations and still need someone who sees the financial whole.

What a fractional CFO actually does

A good fractional CFO doesn’t just send reports. They help you use them.

Typical responsibilities include:

- Building forecasts that tie to hiring, pricing, capital spending, and debt

- Translating financial statements into decisions an owner can act on

- Improving cash planning so timing issues stop dictating strategy

- Preparing for financing with cleaner reporting and stronger lender conversations

- Helping owners plan ahead for expansion, succession, or an eventual sale

If you want a straightforward explanation of the role, this overview of fractional CFO services lays out the difference between routine accounting support and strategic finance.

Signs you’ve already outgrown basic accounting

You probably need fractional CFO support if any of these feel familiar:

- Sales are rising but profit feels weaker

- You’re applying for a loan and your reports need work

- You want to add staff, locations, or equipment

- You can’t explain cash swings clearly

- You’re making decisions based on instinct because reporting arrives too late

That last one is the killer. Plenty of owners think they’re being decisive. They’re really improvising.

If the owner is the only person translating numbers into action, the business will eventually bottleneck around that owner.

A short video can help frame what this level of guidance looks like in practice.

Why fractional beats waiting for a full-time CFO

Most SMBs don’t need a full-time CFO right away. They do need CFO-level thinking. That’s the sweet spot.

A fractional model gives the business access to higher-level planning without building an executive role before the company is ready. The owner gets guidance on pricing, cash reserves, debt decisions, forecasting, tax planning coordination, and reporting discipline. The company keeps flexibility.

Here’s the blunt version. A lot of businesses wait too long because they think hiring strategic financial help means they must “go big” and bring on a full-time executive. Meanwhile they lose margin, miss planning opportunities, and keep discovering problems after the fact.

Every growing company needs a financial adult in the room

That sounds harsh, but it’s true. As a company grows, somebody has to challenge assumptions, pressure-test plans, and translate numbers into operating decisions. Not in theory. In real time.

That’s why every growing business needs a fractional CFO. Not because it sounds impressive. Because growth without financial leadership gets sloppy fast, and sloppy businesses eventually pay for it.

Your Partner in Jacksonville Business Growth

Good financial planning jacksonville business owners can rely on isn’t a retirement brochure and it isn’t a tax return dropped off once a year. It’s an operating system. You assess the health of the business with real reports, forecast cash before problems hit, manage industry-specific issues correctly, and stay ahead of compliance instead of reacting to notices.

That’s the work that creates durable companies.

If your books are behind, your reports are unreliable, your tax calendar lives in somebody’s head, or you know the business has outgrown basic bookkeeping, fix it now. Waiting usually makes the cleanup larger, the tax issues messier, and the cash pressure worse.

Bookkeeping and Accounting of Florida Inc. helps Jacksonville businesses turn messy records into useful financial systems. If you need bookkeeping, payroll, tax preparation, audits, QuickBooks support, industry-specific accounting, or fractional CFO guidance, schedule a conversation with Bookkeeping and Accounting of Florida Inc.. It’s the fastest way to get compliant, understand your numbers, and build a business that runs with less guesswork and more control.