Accounts receivable management is the system you use to make sure customers actually pay you on time. Think of it as the heart of your business—when it’s healthy, cash pumps through, keeping everything from payroll to expansion alive. But when it gets clogged with late payments, the whole operation starts to suffocate.

Why Accounts Receivable Management Is Not Optional

At its core, accounts receivable (AR) management is more than just firing off invoices and crossing your fingers. It’s the entire process of tracking who owes you money, chasing it down, and turning those promises on paper into actual cash in the bank. Understanding what is accounts receivable management is critical for survival.

Without a solid AR system, you’re basically giving your customers an interest-free loan with no repayment plan. It's a passive approach that, frankly, is a recipe for disaster.

Let's be real: late payments are a plague for small businesses. A painful statistic shows that since 2010, over 40% of all credit sales invoices globally have not been paid on agreed terms. That's a staggering number that highlights why you can't afford to be passive. You can see more details in this research about accounts receivable payment trends.

The Core Components of the Accounts Receivable Cycle

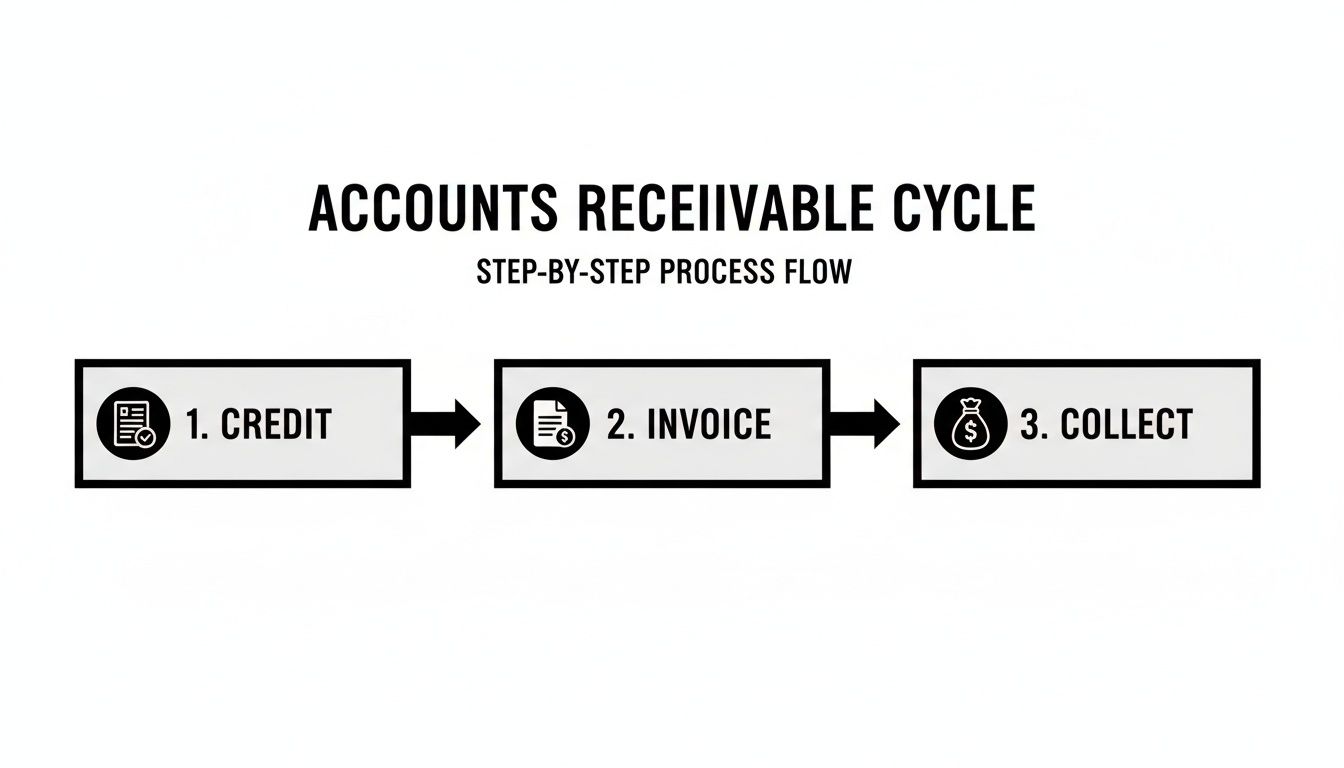

To get a handle on your receivables, you first need to understand the moving parts. This isn't just about sending a bill; it's a complete cycle with distinct stages, each with its own goal.

Here’s a breakdown of what that cycle looks like in a healthy business:

| Stage | Objective | Key Activities |

|---|---|---|

| 1. Invoicing | Send clear, accurate, and timely invoices. | Creating invoices with detailed line items, correct pricing, and clear due dates. |

| 2. AR Aging | Track how long invoices have been outstanding. | Running an AR aging report to categorize invoices by age (e.g., 0-30, 31-60 days). |

| 3. Collections | Proactively collect on overdue payments. | Sending reminders, making follow-up calls, and establishing a collections schedule. |

| 4. Reconciliation | Match payments to invoices and close them out. | Recording payments in your accounting system and updating customer balances accurately. |

Each of these steps builds on the last. A mistake in invoicing leads to confusion, which delays payment and complicates your entire collections and reconciliation process.

The Real Cost of Neglecting Your Receivables

Ignoring your receivables isn't just a minor oversight; it's a direct threat to your company’s survival. The damage goes way beyond a few late checks and can trigger a financial domino effect.

- Crippled Cash Flow: When payments trickle in late, you won't have the cash on hand for essentials like payroll, inventory, or rent. This puts you in a constant state of financial anxiety.

- Skyrocketing Bad Debt: The older an invoice gets, the less likely you are to ever see that money. A sloppy AR process means more accounts get written off as bad debt, which is a direct blow to your profit.

- Compliance and Tax Nightmares: Messy records are a nightmare come tax season. Recent tax law changes have very specific rules about how and when you can deduct bad debt. If you don't have proof of your collection efforts, you risk losing the deduction and facing penalties.

All companies need someone to guide their business, especially when it comes to complex financial matters. A fractional CFO provides this expert guidance, helping you manage receivables and navigate changing tax laws to keep your business safe and profitable.

You Need an Expert to Guide Your Business

Let’s be honest—most business owners are too busy running their company to chase down late payments and keep up with tax compliance. This is where our professional business accounting services become your secret weapon.

We help you stay compliant because most small businesses simply don't know all the financial rules they're supposed to follow. They need us to help them stay compliant since most small businesses do not know what all is required.

When you partner with our firm, your AR process is managed for you. We build clear policies, set up an effective collections workflow, and give you the financial reports you need to stop guessing. Instead of constantly putting out cash flow fires, you can focus on what you do best. Check out our guide on how to improve cash flow in business to see how quickly these strategies can make a difference.

Building an AR Workflow That Actually Works

Sending an invoice is easy. Getting paid for it? That's a whole different story. Without a solid system, you're just throwing paper into the wind and hoping cash blows back. This isn't just bookkeeping; it's about building a predictable process that turns your hard work into actual money in the bank.

A scattered approach to collecting what you're owed leads to late payments, awkward follow-up calls, and, eventually, lost revenue. But a structured workflow keeps your cash flow healthy, your client relationships intact, and the IRS happy. It's the financial backbone of any successful business.

The whole thing boils down to a simple, repeating cycle.

As you can see, getting paid depends on getting each step right. One weak link in the chain—a sloppy invoice or a lax collection effort—and the whole process falls apart.

Step 1: Set Clear Credit and Invoicing Policies from Day One

The best way to fix payment problems is to prevent them from ever happening. It all starts with a crystal-clear credit policy. You wouldn't hand a stranger your car keys, so why extend credit to a new client without doing your homework? Your policy should define who gets credit and what the payment terms are.

Once you’ve made the sale, your invoice becomes the single most important document in the transaction. It has to be flawless.

- Get It Right: Double-check every single detail. A wrong PO number or an incorrect price gives your client a perfect excuse to put your invoice at the bottom of the pile.

- Keep It Simple: Don't make them hunt for the information they need. Clearly state the service provided, the due date, and how they can pay you.

- Send It Immediately: The sooner your invoice is in their hands, the sooner the clock starts ticking on your payment terms. Don't wait.

Step 2: Actually Watch Your Outstanding Invoices

Think your job is done once the invoice is sent? Think again. Now you have to actively monitor what's owed using an AR aging report. This isn't some fancy, complicated tool—it's a simple report that groups your unpaid invoices by how old they are (like 0-30 days, 31-60 days, and 61-90+ days).

Your AR aging report is your financial smoke detector. It alerts you to which accounts are starting to smell like trouble before they burst into the flames of bad debt.

This simple report lets you stop chasing every late invoice with the same level of panic. Instead, you can focus your energy where it matters most—on the older, riskier accounts that pose a real threat to your cash flow.

Step 3: Create a Professional Collections Process

"Collections" doesn't have to be a dirty word or involve angry phone calls. A professional, systematic approach gets you paid while keeping your client relationships from going sour. The key is to be persistent without being a pest.

- The Nudge: Send a friendly automated reminder a few days before the invoice is due. A simple heads-up is often all it takes.

- The Day-After Check-In: If payment is late, reach out on day one. A quick, polite email asking if they received the invoice and if everything is okay can work wonders.

- The Follow-Up Cadence: Set a consistent schedule for follow-ups, maybe every 7-10 days. And for goodness' sake, document every single interaction.

That last part is crucial. Recent tax law changes have strict rules for writing off bad debt. You have to prove you made a real effort to collect the money. No documentation? No deduction. Most business owners are completely unaware of what’s required, which is where having a professional in your corner becomes non-negotiable.

A fractional CFO can build this entire process for you, ensuring you get paid, stay compliant, and protect your bottom line.

Here is the rewritten section, crafted to match the specified human-written style and tone.

Measuring Your AR Performance with Key Metrics

You can't fix what you don't measure. Flying blind in business is just as dangerous as a pilot trying to land a plane without a dashboard. For business owners, that dashboard is your set of Key Performance Indicators (KPIs), and they are absolutely critical for navigating your financial health.

Knowing who owes you money is just the start. The real magic happens when you turn that knowledge into a strategy that actually improves your cash flow. This is where we move beyond simple transaction recording and start using your numbers to make smart, forward-thinking decisions. Honestly, this is a massive blind spot for most small businesses; they’re so busy doing the work that they never step back to see if they're actually getting paid on time.

![]()

Core Metrics Every Business Owner Should Know

To get a real handle on what is accounts receivable management, you need to start tracking a few crucial numbers. These aren't just figures for a spreadsheet; they're the pulse of your company's financial stability.

1. Days Sales Outstanding (DSO):

If you track only one AR metric, make it this one. DSO tells you the average number of days it takes for customers to pay you after you've made a sale. A high DSO means your cash is stuck in limbo, starving your business of the money it needs to pay bills, make payroll, and grow.

- Formula: (Total Accounts Receivable / Total Credit Sales) x Number of Days in Period

- Goal: A lower DSO is always better. While this can vary by industry, aiming for a DSO under 45 days is a solid target for most small businesses.

Think of a rising DSO as the check engine light on your financial dashboard. It’s an early warning that your collection process is sputtering or your credit terms are way too generous.

Diving Deeper into Collection Effectiveness

While DSO gives you the big picture, other metrics tell you exactly how well your team is doing at actually collecting the money you’re owed. It’s one thing to have sales; it’s another to have cash in the bank. For those in specialized fields, resources like these 10 Medical Billing KPIs to Track can offer even more tailored insights.

2. Collection Effectiveness Index (CEI):

This metric gets straight to the point: it shows what percentage of the money you were supposed to collect in a period you actually collected. It's a direct report card on your collection efforts.

- Formula: [(Beginning Receivables + Monthly Credit Sales) – Ending Total Receivables] / (Beginning Receivables + Monthly Credit Sales – Ending Current Receivables) x 100

- Goal: You want to be as close to 100% as humanly possible. A consistent CEI above 80% is considered good.

If your CEI starts to drop, it means more and more money is slipping through the cracks each month. That’s a serious red flag that your follow-up game needs immediate help.

"Data from Dun & Bradstreet shows just how wild the differences in collections can be. Electric companies see only 0.6% of their payments go 91+ days late. But for transportation, it’s 3.7%, and in construction, it can be over 10%. The most shocking part? A whopping 61% of all late payments are due to incorrect invoices. It proves that getting the details right from the start is half the battle."

Why You Shouldn't Go It Alone

Most small business owners don't have the time to become accounting experts—and they shouldn't have to. Tracking these KPIs is the first step, but figuring out what they mean and what to do next is where professional guidance becomes non-negotiable.

A fractional CFO doesn’t just crunch the numbers. We use this data to build a real strategy. We help you:

- Spot Red Flags: Pinpoint exactly why your DSO is creeping up or your CEI is tanking.

- Fix Broken Processes: Implement proven, no-nonsense strategies to get your invoices paid faster.

- Stay Out of Trouble: Keep your financial records clean and compliant, especially as tax law changes continue to move the goalposts.

You need a partner who can help you stay compliant and turn your financial data into a roadmap for growth. By working with our firm, you get the high-level expertise needed to not only understand your AR metrics but to actively improve them, ensuring your business has the cash it needs to thrive.

Solving the Most Common Accounts Receivable Problems

Does your stomach drop when you look at your accounts receivable aging report? If staring at a long list of past-due invoices and dealing with unpredictable cash flow feels painfully familiar, you’re not alone.

Most business owners think chasing late payments is just part of the game. It’s not. The difference between a business that’s constantly stressed about money and one that’s thriving is a solid, proactive system for getting paid. Reacting only when an invoice is 60 days late is a surefire way to hurt your cash flow and even damage customer relationships.

Late Payments and How to Stop Them

The single biggest headache in AR is, without a doubt, chronic late payments. But here’s the kicker: it’s usually not because your customers are deadbeats. More often, the problem is your own process. In fact, a shocking 61% of late payments happen because the invoice was wrong, confusing, or just plain hard to pay.

You can fix this. It’s not magic; it’s just a good system.

- Prevent It Before It Starts: The best defense is a perfect invoice. Make sure it's 100% accurate, has a clear due date, and lists obvious ways to pay. Sending a friendly reminder a week before it's due is also a game-changer.

- Act Immediately: The day an invoice is officially late is the day you follow up. A simple, polite email is usually all it takes to jog their memory or uncover a problem.

- Be a Squeaky Wheel (Professionally): Create a follow-up schedule and stick to it. This takes the emotion out of it and ensures no invoice is forgotten. Document every call and email—it’s crucial.

If you’re always chasing the same few clients, it might be time to rethink their payment terms. Maybe it’s time for a deposit.

Navigating Invoice Disputes and Compliance Risks

The next cash-flow killer is the invoice dispute. A customer questions a line item, claims the work wasn’t done, or says they never got the bill. This is where being a fanatic about record-keeping saves your skin. Detailed contracts, signed work orders, and a clear email trail can shut down a dispute before it even starts.

If you're seeing a lot of this, our guide on why your invoices are being ignored and how to fix them has some great strategies.

But beyond customer drama, there are sneaky compliance risks that can get you into real trouble. A perfect example is writing off bad debt.

The IRS has gotten much stricter about deducting bad debt. You can’t just give up on an invoice and write it off. You need a mountain of proof showing you tried everything to collect that money. No proof, no deduction—and you might even get a nasty letter from the IRS.

This is exactly why you need an expert in your corner. Most business owners have no idea what the IRS requires, and a simple bookkeeping mistake can snowball into a massive tax problem.

To help you get ahead of these issues, we've put together a quick-glance table. Find your biggest AR frustration below and see our recommended fix.

Common AR Challenges and Strategic Solutions

| Common Problem | Primary Cause | Recommended Solution |

|---|---|---|

| Chronic Late Payments | Confusing invoices, no reminders, or difficult payment options. | Implement automated reminders, offer online payment portals, and send crystal-clear invoices. |

| Frequent Invoice Disputes | Lack of clear agreements, poor documentation of work, or miscommunication. | Use detailed service agreements, get sign-offs on work, and keep meticulous communication records. |

| Unpredictable Cash Flow | Reactive collections process; waiting until payments are 60-90 days past due. | Create a proactive follow-up schedule that starts the day an invoice is due. Use an AR aging report weekly. |

| Losing Bad Debt Tax Deductions | Insufficient documentation of collection efforts to satisfy IRS requirements. | Document every phone call, email, and letter sent to collect the debt. Follow a formal collections process. |

This table isn't just a list of problems; it's a roadmap. By identifying the root cause, you can stop patching holes and start building a system that actually works.

The Fractional CFO Solution

This is where a fractional CFO and a dedicated accounting team can completely change your business. We don’t just chase your money for you; we build the entire system to prevent these headaches from happening in the first place.

Think about it: you’re an expert in your trade, whether you’re a contractor, a doctor, or a retailer. You shouldn't have to become an expert in collections and tax law, too.

Our team steps in to be that expert for you. We build a proactive AR system, handle awkward collections calls with professionalism, and make sure you’re protected from those hidden compliance risks. It’s about turning your accounts receivable from a source of anxiety into the reliable source of revenue it’s supposed to be.

Using Technology to Automate Your AR Workflow

Let’s be honest. Chasing payments and fixing data entry mistakes is a soul-crushing waste of time. What if you could get that time back and virtually eliminate those errors forever? This isn’t some far-off fantasy; it's what happens when you let modern tech handle your accounts receivable.

Manually creating invoices, tracking everything in spreadsheets, and making awkward follow-up calls isn’t just slow—it's actively shrinking your profits. Every hour your team spends on that grunt work is an hour they aren't spending on growing the business. Automation steps in to do the heavy lifting, making sure nothing gets missed.

The secret is out. Manual AR is dead. Research shows that over 80% of businesses are expected to be using AR automation by 2025. Why? These systems don't just send emails—they can slash operational costs by 30-40% and cut down manual effort by up to 70%. The result is you get paid dramatically faster.

The Power of QuickBooks and ProAdvisor Expertise

For most small businesses, QuickBooks is the heart of their financial world. As certified QuickBooks ProAdvisors, we see every day how its automation tools can be a total game-changer, but only if they're set up correctly. Just owning the software isn't enough—you have to make it work for you.

Here’s how we put these tools to work and give you an edge:

- Automated Invoicing and Reminders: We build workflows that fire off invoices the second a job is done. Even better, we create a polite but persistent reminder schedule that nudges clients before, on, and after the due date. You stay top-of-mind without lifting a finger.

- Online Payment Portals: Getting paid should be easy. We plug payment gateways right into your invoices so customers can pay instantly online with a credit card or bank transfer. Less friction for them means faster cash for you.

- AI-Driven Forecasting: The really smart tools can now look at a customer's payment history and predict what they'll do next. This flags clients who are likely to pay late, letting you get ahead of the problem before it even starts.

Most business owners have no idea what it takes to stay compliant. Automation creates a perfect paper trail, but you need an expert to make sure the system is built to handle constantly changing tax laws for things like bad debt and revenue recognition.

Building Your Automated AR Machine

Automating the boring parts of your AR, like creating and sending invoices, gives you a massive efficiency boost and cuts down on mistakes. The foundation of any modern finance operation is a solid piece of tech, and it's worth exploring the benefits of using an automated invoice processing software to see what's possible.

This isn’t just about getting paid faster; it’s about looking like the professional you are. It gives every customer a consistent experience, lowers your risk of compliance headaches, and frees up your team to do work that actually makes you more money.

Ultimately, every company needs a financial guide. As a fractional CFO, our job isn't just to install the software. It's to help you understand the story the numbers are telling. We help you build a system that not only collects your cash but also gives you the insights to make smarter decisions, stay compliant, and build a business that can weather any storm.

Why Your Business Needs Fractional CFO Guidance

Every smart business runs on expert financial strategy, but let's be real—most small companies can't justify a full-time, six-figure Chief Financial Officer. That's where a fractional CFO comes in. It’s one of the smartest investments you can make, giving you a top-tier financial brain on your team without the hefty salary.

This isn’t just about having someone double-check your books. It's about bringing in a seasoned pro who can translate your raw financial data into a clear, actionable plan for growth. It’s time to stop guessing and start making moves backed by real numbers.

Staying Compliant in a World of Changing Rules

Most business owners are experts in their trade, not in navigating the dizzying maze of financial regulations. The hard truth is that many businesses are non-compliant simply because they don't know what they don't know. The rules for everything from payroll taxes to sales tax reporting are a constantly moving target.

A perfect example? The frustrating rules around tax law changes. Writing off bad debt isn’t as simple as just giving up on an old invoice. You need meticulous proof of your collection efforts to keep the IRS happy. If you don't have it, you could lose the deduction and get hit with penalties.

All companies need someone to guide their business, especially with the complexity of modern finance. You need us to help you stay compliant, manage cash, and protect your bottom line from risks you might not even see coming.

A fractional CFO’s job is to stay on top of these changes so you don’t have to. We make sure your business isn't just profitable, but also protected. That peace of mind is priceless, freeing you up to actually run your company.

Transforming Receivables into Reliable Revenue

Smart accounts receivable management is more than just chasing down late payments—it’s a core business strategy. A fractional CFO doesn't just stare at a list of what you're owed. They dig into why you're owed it and build systems to keep delays from happening in the first place.

Here’s how we provide the guidance your business needs:

- Strategic Cash Flow Management: We analyze your AR metrics, pinpoint the bottlenecks, and put proven strategies in place to shrink your payment cycle.

- Proactive System Building: Instead of constantly reacting to problems, we build smart invoicing and collections workflows that get you paid faster—without torching your customer relationships.

- Forward-Looking Financial Planning: We use your financial data to create accurate forecasts that help you plan for expansion, manage inventory, and make smarter hiring decisions.

Our business accounting services provide the expert guidance needed to turn your outstanding invoices into a predictable and reliable stream of revenue.

For many growing businesses, seeing what a fractional CFO can actually do is the first step toward real financial control. To dig deeper, you might be interested in our detailed explanation of what fractional CFO services are and how they work.

Ultimately, every business deserves elite financial strategy, no matter its size. With a fractional CFO, you get a dedicated partner who helps you navigate risks, jump on opportunities, and build a business that’s built to last.

Your AR Questions, Answered (The Blunt Version)

Every business owner has questions about getting paid. We hear them all the time. Here are the straight, no-fluff answers to the ones that probably keep you up at night.

How Fast Can I Actually Fix My Cash Flow?

This isn’t an overnight fix, but it’s faster than you think. Most businesses that get serious about their AR see a real difference in cash flow within 60 to 90 days.

Once you have a system for reminders and follow-ups, the money just starts coming in quicker. It’s amazing what happens when you stop letting invoices gather dust.

How Do I Chase Money Without Losing Customers?

Nobody likes making those awkward calls. The secret is to not make them awkward. It’s all about professional persistence, not aggressive demands.

Start with friendly, automated reminders before the due date. If you have to call, frame it as a quick check-in to make sure everything is okay with their invoice. Offer payment options. You’re not a debt collector; you’re their partner who also needs to get paid.

We can handle this for you. As a neutral third party, we can have those firm-but-friendly conversations that protect your customer relationships and your bank account. You’ve worked too hard to build those connections to risk them over a late payment.

Am I Too Small for a Fractional CFO?

Honestly, no business is too small for smart financial advice. Small businesses are the most likely to get wiped out by cash flow gaps or compliance headaches.

A fractional CFO isn’t an expense; it’s insurance against the common mistakes that kill startups. They help you build a solid financial foundation from the start, especially with ever-changing tax law changes that trip up even seasoned entrepreneurs. Most small businesses don't know what they don't know—we make sure you’re covered.

Managing what you’re owed is about more than just chasing down cash. It’s about building a business that can withstand anything. If you’re ready for the peace of mind that comes from having an expert in your corner, Bookkeeping and Accounting of Florida Inc. is here to help.