You bought the gear. You paid for the training. You replaced uniform items your department didn't fully cover. Then tax time rolls around and you assume those costs will help you out.

For a lot of police officers, that's where the bad news hits.

The old playbook for police officer deductions for taxes changed hard. If you're a straight W-2 officer, many expenses you used to think of as write-offs usually don't help you on your federal return anymore. That's not a paperwork glitch. That's tax law.

The good news is there's still a smart way to approach this. You just need to stop thinking like an employee with receipts and start thinking like a business owner when you have off-duty income. That shift is where real planning lives now. It's also where good accounting stops being a nice extra and starts being the thing that keeps you compliant and keeps money from leaking out of your pocket.

Why Your Gear and Uniforms Are Suddenly Not Deductible

You're at the kitchen table in March with a pile of receipts. New boots. Replacement uniform shirts. A vest upgrade. Range gear. Maybe a class you paid for because the department budget was thin. You assume the IRS will at least give you some credit for spending your own money to do your job.

That assumption is out of date.

The rule change that killed the old write-off

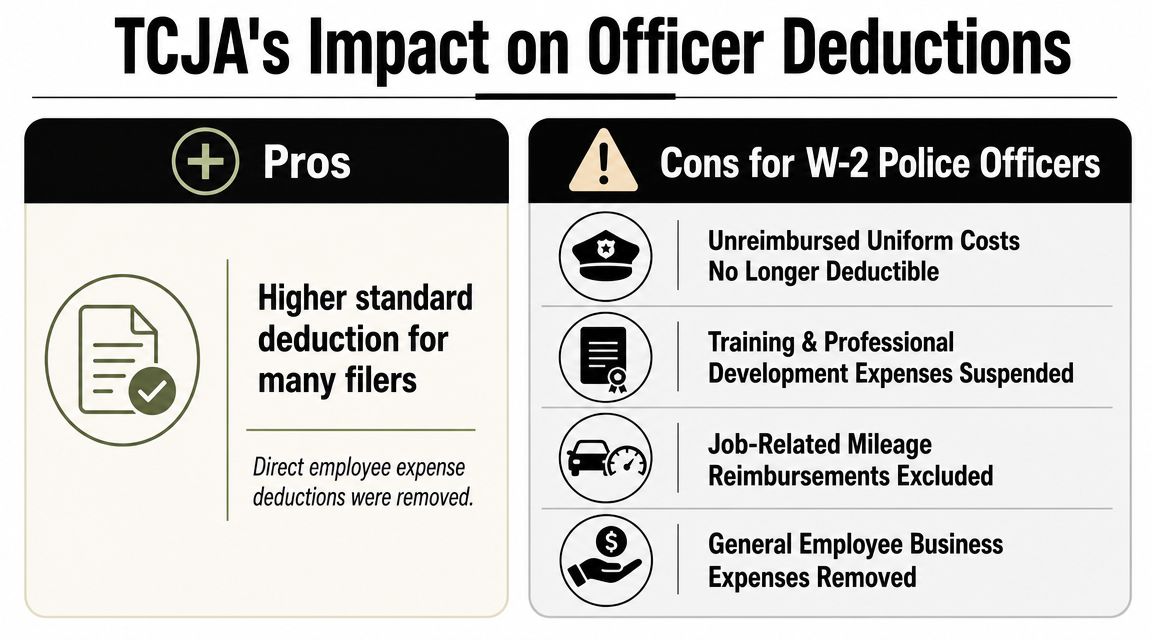

The Tax Cuts and Jobs Act suspended unreimbursed employee business expense deductions for federal tax purposes from 2018 through 2025. For police officers, that shut down the old Schedule A route for many out-of-pocket job costs. IRS Publication 529 explains that miscellaneous itemized deductions subject to the 2% limit, including unreimbursed employee expenses, are suspended during that period.

If you're a W-2 officer, that means the fact that an expense is required for the job does not make it federally deductible. The IRS does not care that the boots were mandatory, the uniform had to match policy, or the gear made you safer. If the department did not reimburse you, the federal deduction is usually still zero.

That is the part officers hate. It is also the part they need to stop arguing with.

Practical rule: Old locker-room tax advice is usually based on pre-TCJA law and usually wrong.

Why officers get tripped up

The confusion is understandable. For years, cops were told to save every receipt because work expenses might help at tax time. Then the law changed and a lot of that advice became stale overnight.

So officers keep doing what used to make sense. They track uniform costs, equipment purchases, training, and mileage tied to their employee job, then expect a federal write-off that never shows up. That wastes time and creates bad planning.

A smarter approach separates expenses by how you earn the income tied to them:

- W-2 officer expenses: generally not deductible on your federal return if unreimbursed

- Reimbursable employee expenses: worth pushing through department policy or an accountable plan if available

- Off-duty 1099 or business income expenses: often deductible when reported properly on Schedule C

That last bucket is where the true strategy starts. Post-TCJA, the biggest tax opportunity for many officers is not squeezing harder on W-2 receipts. It is setting up off-duty work correctly so legitimate business deductions count.

The Post-TCJA Reality for W-2 Employee Officers

You buy replacement boots, pay for a training course, throw gas in the tank for a work errand, and figure tax time will soften the blow. Then your return gets done and the deduction is gone.

That is the post-TCJA reality for W-2 officers.

If your income from the department is reported on a W-2, unreimbursed employee expenses generally do not help you on your federal return right now. The old miscellaneous itemized deduction rules for employee business expenses were suspended for tax years 2018 through 2025 under the Tax Cuts and Jobs Act, as the IRS explains in its page on miscellaneous deductions subject to the 2% limit.

Before and after the tax law change

Before TCJA, some employees could deduct unreimbursed job costs on Schedule A if they itemized and cleared the old limitations. Congress shut that door for most W-2 workers at the federal level.

For officers, that changed the tax answer on a long list of common expenses. Uniform replacements. Duty gear. Work-related training. Union-related costs in some cases. Mileage tied to your employee role, which was already limited and never included normal commuting.

Here is the blunt version. Paying for something out of pocket does not make it deductible.

What that means for your return

A lot of officers still bring in a folder full of receipts from their employee job and expect a write-off. I get why. That advice used to be common. It is also outdated.

If you are only a W-2 officer, your federal deduction for many job expenses is usually zero. The standard deduction is also much higher than it was before TCJA, which made itemizing less useful for many taxpayers in the first place, according to the IRS page on the standard deduction.

Use this checklist as your default rule:

- Uniform and boot replacements: usually no federal deduction as a W-2 employee

- Personally purchased duty gear: usually no federal deduction

- Training you paid for yourself: usually no federal employee deduction

- Employee-job mileage: limited, and commuting is not deductible

Officers do not have a receipt problem. They have an income-classification problem.

That distinction matters more than ever. Expenses tied to your W-2 job are treated one way. Expenses tied to separate self-employed income are treated another way. That is why smart tax planning after TCJA shifted away from hoping employee receipts still work and toward two things that move the needle: proper reimbursement and correctly reporting off-duty 1099 work on Schedule C.

If you want a plain-English explanation of tax deferral as part of a broader planning approach, this quick piece on Fintrack for lowering taxes is worth a read.

Tax-Reducing Strategies Still Available to Employees

If you're a W-2 officer, don't throw your hands up and assume there's nothing left to do. There is. You just need to focus on the right levers.

Push for reimbursement under an accountable plan

An accountable plan is one of the cleanest ways to deal with employee expenses. If your employer reimburses qualifying work expenses under a proper accountable plan, that reimbursement generally isn't treated as taxable income. That's a lot better than paying out of pocket and hoping for a deduction that isn't there.

If your department or agency has any reimbursement process, use it properly. If they don't, ask about it. I've seen too many people shrug off reimbursement paperwork while chasing deductions they can't legally claim.

What matters is clean support:

- Keep the receipt

- Document the business purpose

- Submit it on time

- Follow department policy exactly

That's boring. It's also effective.

Lower taxable income the old-fashioned smart way

If the deduction door is shut, reduce taxable income elsewhere. That usually means making the most of employer-sponsored pre-tax options such as retirement contributions and, when available, an HSA.

A lot of officers focus on what they can write off and ignore what they can shelter before taxes ever hit. That's backward. Pre-tax contributions are still one of the most reliable tools on the board.

If you want a plain-English refresher on the concept, this guide to Fintrack for lowering taxes does a good job explaining why deferral matters.

My recommendation for W-2 officers

Don't spend your energy trying to force old deductions onto a federal return that won't allow them. Do this instead:

- Max out legitimate reimbursement channels through your employer.

- Use pre-tax retirement contributions aggressively if your cash flow allows.

- Use an HSA if you're eligible.

- Separate your employee role from any side work so you don't mix records.

That last point matters more than people realize. Mixed records create messy returns. Messy returns create expensive problems.

The Strategic Shift: Off-Duty Work and Schedule C

You work your regular department job all week, then spend Saturday directing traffic for a church event or working private security at a festival. Same uniform category. Same law-enforcement skill set. Very different tax result.

That difference is where the actual planning starts.

After TCJA, a W-2 officer can buy gear, pay for training, and rack up work-related mileage and still get no federal deduction for unreimbursed employee expenses. But if you earn separate off-duty income as an independent contractor, you may be running a business. That means some of those costs can move into Schedule C territory, where the tax rules are far more useful.

Worker classification drives the deduction

The first question is not whether the expense sounds job-related. The first question is who you were working for when you incurred it.

If the cost belongs to your department job, federal deduction options are usually dead. If the cost belongs to a real off-duty business activity, Schedule C may allow a deduction if the expense is ordinary, necessary, and properly documented under IRS business expense rules.

Here's the practical comparison:

| Expense | W-2 Employee (Federal Deduction) | Schedule C Contractor (Business Deduction) |

|---|---|---|

| Uniform used for employee job | Generally not deductible federally | May be deductible if tied to the side business and qualifies |

| Duty gear for employee role | Generally not deductible federally | May be deductible if ordinary, necessary, and documented |

| Mileage | Employee mileage is heavily restricted | Business mileage for the side gig may be deductible |

| Training | Usually no federal employee deduction | May be deductible if connected to the business activity |

| Licenses and related business costs | Often no employee deduction | May be deductible if properly tied to self-employed work |

That is the harsh post-TCJA reality. The old employee write-off approach is mostly a dead end. Smart officers stop fighting that fight and build their strategy around the income they earn outside the W-2 role.

A simple example

Say you buy a duty-specific item for private security jobs where you are paid as an independent contractor. That expense may belong on Schedule C.

Buy that same item only for your department position, and the federal return usually gives you nothing.

Same receipt. Different tax treatment. The role matters.

Why officers get this wrong

A lot of officers do legitimate side work but handle it like pocket money. They dump the income into a personal account, pay expenses from wherever, save half the receipts, and hope the return gets sorted out in April. That is how good deductions get lost.

If off-duty work is a steady income stream, treat it like a business from day one. Separate records. Separate income tracking. Clean expense support. Real bookkeeping.

That also opens the door to bigger planning opportunities, including the Qualified Business Income deduction rules for Schedule C income. Once you have profitable side work, the conversation is no longer just about boots, belts, and mileage. It becomes business tax planning.

And that is the point. Post-TCJA, the best deduction strategy for many officers is not squeezing harder on disallowed employee expenses. It is correctly structuring and reporting off-duty contractor income so the tax law gives you something back.

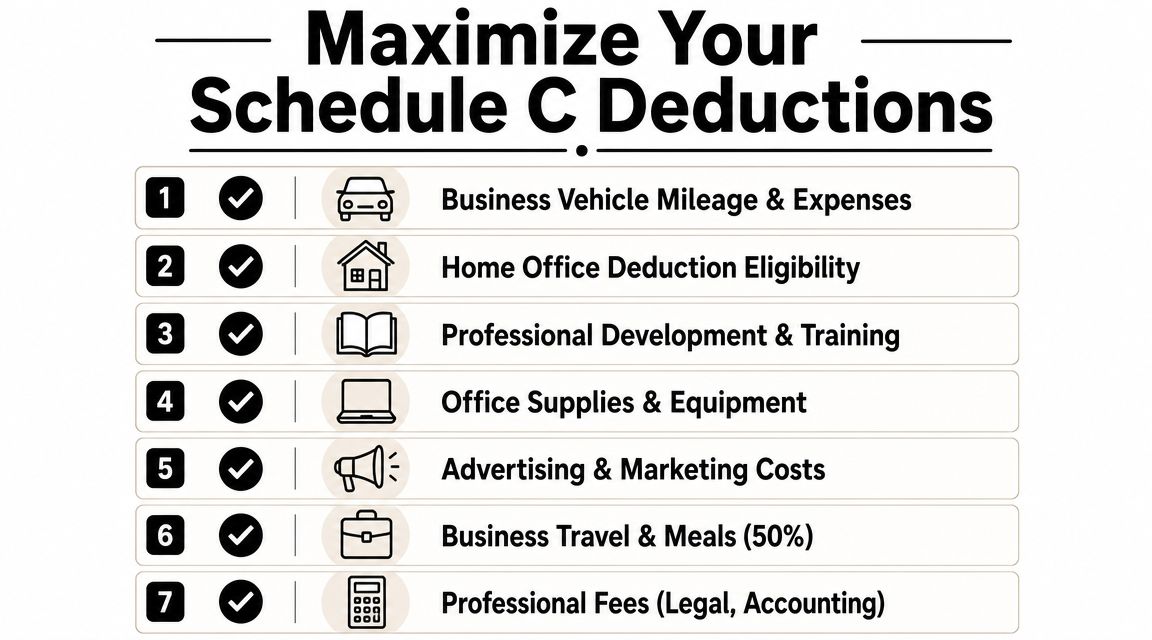

What You Can Deduct on Your Schedule C Side Gig

You worked a Saturday private security detail, bought gear for that job, tracked your miles, paid for liability coverage, and answered client calls on your own phone. That income belongs on Schedule C, and the expenses tied to it can reduce the tax hit. That is the break many officers miss.

Uniforms, gear, and the street-wear trap

Schedule C gives you a real deduction only if the expense belongs to the side business and holds up under scrutiny. For clothing and gear, the IRS draws a hard line. Distinctive uniforms and duty-specific equipment used for the contractor work can qualify. Regular clothes that also work off duty usually do not. The IRS instructions for Schedule C and Publication 535 both follow that ordinary-and-necessary standard, and that is the standard I would use on your return.

Here is the practical version. A plate carrier, duty belt setup, specialty holster, body armor accessories, and equipment repairs tied to paid off-duty assignments may be deductible if you bought them for that work and kept the records. Generic black boots, tactical pants, or polo shirts you would wear anyway are weak deductions. Weak deductions cost people money in an audit.

Mileage follows the same logic. Business miles between assignments, supply runs, or trips to meet a client can count. The drive from home to the job site is usually commuting, and commuting is personal.

Expenses that often qualify when they are tied to the side gig and documented:

- Duty-specific holsters and related equipment

- Protective gear used for private-duty assignments

- Repairs and maintenance for business-use equipment

- Business mileage between work locations or for client-related errands

- Specialty footwear if it is clearly required for the work and not general street wear

Expenses that usually fail or need a tight allocation:

- Generic clothing you could wear anywhere

- Home-to-assignment commuting miles

- Mixed personal and business purchases with no clean breakdown

- Gear bought for the department job but pushed onto Schedule C

If you use part of your home regularly and exclusively for scheduling, billing, record storage, or admin work for the side business, review this home office deduction calculator guide before you claim it. Home office deductions are legitimate. They are also easy to botch.

Other Schedule C categories officers overlook

Gear gets all the attention. The quieter deductions are often just as useful.

Off-duty officers commonly miss expenses for training tied to the private-duty work, business use of a phone, scheduling apps, report software, licensing fees, permits, liability insurance, bookkeeping, and tax prep related to the business. If you pay someone for audit representation for the Schedule C activity, that can also fall into the professional-fees category when it relates to the business.

This short video adds a useful visual explanation of common Schedule C deduction buckets.

The IRS does not care that an expense felt work-related. It cares whether the expense was ordinary, necessary, and proven.

The test that matters

Run every deduction through three questions. Was it ordinary for the side work? Was it necessary to earn that income? Can you prove the amount, date, and business purpose?

If one of those answers is no, leave it off or fix the records before filing. That is how a smart Schedule C saves taxes without creating stupid audit problems.

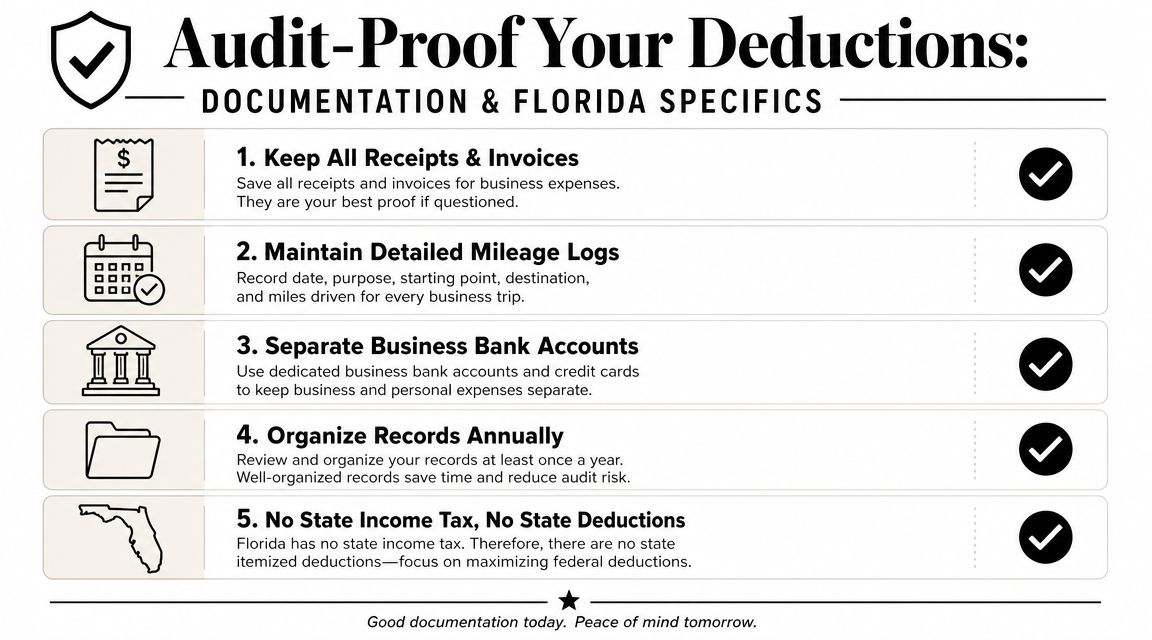

Documentation and Staying Audit-Proof in Florida

You work a paid off-duty detail on Saturday, buy gear for that side work, put miles on your truck, and pay for a scheduling app. By tax time, none of that matters if your records are sloppy. Florida gives you a break on state income tax. The IRS gives you no break on proof.

What the IRS expects from a Schedule C officer

For an officer with legitimate Schedule C income, documentation is what turns expenses into deductions. The rule is simple. If you cannot show what you bought, when you bought it, how much you paid, and how it relates to the side gig, the deduction is weak.

That matters more now because TCJA shut the door on most unreimbursed employee expenses for W-2 officers. So the smart tax strategy is not arguing over old employee write-offs. It is building clean records around off-duty income that belongs on Schedule C and claiming the deductions that still hold up.

A uniform or piece of gear tied to your side work can be deductible there. The same type of expense tied only to your W-2 job usually is not. Same item. Different tax treatment. Documentation is what keeps those categories separate.

My audit-proof checklist

Use a real system from day one. Good records beat good excuses every time.

- Separate bank account: Run side-gig income and expenses through a dedicated business account.

- Mileage log: Keep a contemporaneous log, not a reconstruction six months later. If you need a method that holds up, review this guide on tracking business mileage.

- Receipt capture: Save invoices, digital receipts, and proof of payment in one folder or app.

- Books updated regularly: Use QuickBooks or similar software so the totals on the return match the records behind them.

- Year-end review: Reconcile accounts and clean up support before filing season, while the details are still fresh.

Clean books do more than support deductions. They show whether your off-duty work is producing real profit or just giving you a pile of receipts.

If the IRS asks questions, you want records that answer them fast. If things get messy, audit representation can help you understand what professional support looks like once the IRS starts digging.

Where firms help

Officers are good at spotting nonsense. Apply that same standard to your tax records. A phone gallery full of random receipts is not bookkeeping, and a spreadsheet built the night before filing is not a system.

A good accounting firm helps separate W-2 expenses from Schedule C deductions, code transactions correctly, track mileage, and keep the return consistent with the books. That is where the actual value sits after TCJA. Not in trying to force dead employee deductions back onto the return, but in handling the side-income strategy the right way the first time.

Let Us Handle Your Taxes So You Can Focus on Your Beat

You finish a long shift, open your tax folder, and see the same mess I see every year. Uniform costs that no longer help on a federal return. A side gig that can save you money if it is set up correctly. A pile of receipts that means nothing unless the books match the return.

That is the post-TCJA reality for police officers.

If you are a W-2 officer, stop chasing write-offs that are gone. Put your energy into the areas that still produce results. Reimbursement plans through the department. Pre-tax benefits. And, for many officers, the biggest opportunity left: off-duty work reported the right way on Schedule C.

That strategy saves money only if the records are clean. Off-duty security work is not casual tax territory. It is a business activity, and the IRS expects business-level records. If you need a quick refresher on what to keep, review this guide on essential receipts for maximizing deductions.

A phone full of photos and a half-finished spreadsheet will not cut it.

You need books that separate W-2 life from side-gig expenses, track mileage and supplies correctly, and support the numbers on the return. You also need someone who can tell you when the side work is producing real profit, when estimated taxes need attention, and when sloppy habits are turning into audit risk.

Bookkeeping and Accounting of Florida Inc. handles bookkeeping, tax preparation, payroll, audit support, QuickBooks setup and maintenance, and fractional CFO services. For officers with off-duty income, that matters because the tax return is only as good as the records behind it.

Here is the blunt version. Police officer deductions did not disappear. The savings shifted. Officers who keep fighting for dead employee deductions waste time. Officers who treat off-duty income like a real business usually have far better options.

If you want help sorting W-2 limits, Schedule C deductions, bookkeeping, and compliance for your off-duty business, talk to Bookkeeping and Accounting of Florida Inc.. We'll help you organize the records, file correctly, and build a tax plan that fits the rules you live under now.