You're probably here because the workers' comp bill landed on your desk, you stared at it for a minute, and then you asked the same question every Florida owner asks: what is workers comp exemption, and can it save me money without blowing up my business?

Fair question. Also a dangerous one.

I've seen owners treat a workers' comp exemption like a clever shortcut. It isn't. It's a narrow legal status for specific people in specific situations. Used correctly, it can reduce premium costs for an eligible owner or officer. Used carelessly, it can leave you uninsured where you thought you were covered, scramble payroll, and create a compliance mess that follows you into audits, contract reviews, and injury claims.

That's why this topic belongs in the same conversation as payroll, tax law changes, bookkeeping, job costing, and risk management. Workers' comp doesn't live in a silo. It hits your insurance costs, your payroll setup, your officer pay, your hiring model, and your ability to prove you're compliant when someone asks.

Why Business Owners Gamble on Workers Comp Exemptions

A Jacksonville contractor hires a few workers, lands decent jobs, and then starts watching overhead creep up. Insurance, payroll taxes, materials, fuel, subs, software. Every line item gets a hard look. Workers' comp jumps off the page because it feels expensive and annoyingly required.

So the owner hears about an exemption and thinks, “Good. I'll file a form, get out of the policy, and move on.”

That's the gamble.

The problem isn't that exemptions are illegal. They're not. The problem is that owners often assume exemption means the business is off the hook. In reality, a workers' comp exemption is a compliance tool with very specific limits. It can help in the right structure, but it can also create a false sense of safety. That's how people end up underinsured while thinking they've “handled it.”

Why the idea is so tempting

Business owners usually chase exemptions for one of three reasons:

- Premium pressure: Workers' comp costs can feel like dead weight when margins are already tight.

- Owner mindset: Many owners think, “I'd never file a claim on myself anyway.”

- Bad advice from the field: A friend, sub, or payroll clerk says, “Everybody does it.”

That last one is where trouble starts. “Everybody does it” is not a compliance strategy. It's how small businesses end up paying professionals to clean up avoidable mistakes.

Practical rule: If a cost-saving idea sounds simple but touches payroll, ownership, and insurance, it's usually not simple.

Why this issue keeps getting worse

Hiring has changed. More businesses use part-time help, seasonal labor, project crews, and contractor-heavy staffing. Tax law changes and labor rule updates also force owners to revisit how they classify pay, report compensation, and document roles. That means your workers' comp position can't sit in a dusty folder while your business evolves.

An exemption that made sense when you had no staff may become a liability once you add employees, switch entity structure, or bid larger jobs.

If you want the blunt CPA answer, here it is. An exemption is not a savings hack. It's a risk allocation decision. If you don't understand exactly whose risk you're taking on, don't file anything yet.

Understanding Workers Comp Exemption vs Non-Compliance

Let's clear up the biggest misunderstanding first.

A workers' compensation exemption is a formal legal carve-out. It is not the same thing as operating without required coverage. Those are two very different situations, and the state won't confuse them just because you do.

What an exemption actually means

In major U.S. markets, a workers' comp exemption is usually a state-controlled carve-out for specific owner or officer classes, not a blanket opt-out for the whole company. Florida is one example. As noted by Tennessee's exemption registry guidance, Florida issues exemptions to corporate officers or LLC members, and once granted, the exempt person isn't treated as an employee for workers' comp purposes and may not recover workers' comp benefits. It reduces premium exposure for that named individual, but it does not remove the employer's duty to cover non-exempt employees under state rules, as explained in the Tennessee exemption registry overview.

That's the distinction most owners miss.

Think of it this way. Taking one owner off the policy is like taking one player off the field. Running a business with required employees uninsured is forfeiting the game and hoping the referee doesn't notice.

What non-compliance looks like

Non-compliance is simpler, and uglier. It means your business should have coverage but doesn't. Sometimes owners get there by accident. More often, they get there by making bad assumptions:

- Assuming owner exemption covers everyone: It doesn't.

- Treating all workers like contractors: That won't hold up if the facts say otherwise.

- Using stale payroll records: Old classifications create current problems.

- Thinking a certificate solves everything: It only solves the problem it applies to.

If your payroll records are messy, fix that first. A clean setup matters because exempt owner pay and employee wages should not be dumped into the same bucket. If your payroll process needs work, this guide on how to set up payroll for small business is a useful starting point.

If the business has non-exempt employees, the business still has an insurance obligation. The owner's exemption doesn't erase it.

You should also understand the insurance side before making a filing decision. A practical primer on commercial workers' compensation insurance can help you compare the role of coverage versus exemption in practice.

Florida's Exemption Rules for Business Owners

Florida owners love simple answers. This topic doesn't provide them.

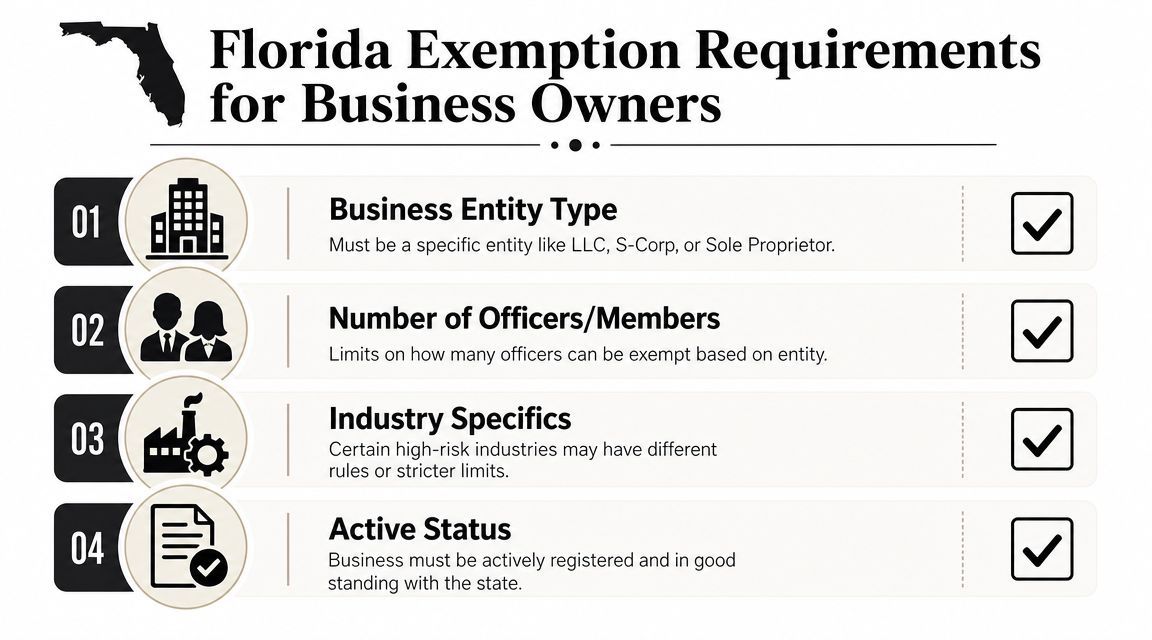

Your eligibility for exemption turns on details, and details are where DIY filings usually fall apart. Entity type, ownership, role, and industry all matter. “I own the company” is not a legal analysis. It's a sentence people say right before discovering the state wanted more paperwork than confidence.

Owner status alone isn't enough

Across states, exemption rules are highly specific and often depend on ownership percentage, entity type, and role. Massachusetts, for example, allows certain corporate officers and directors who own at least 25% to request exemption through Form 153, while Utah may require documents such as business licenses, tax returns, bank records, ads, and proof of liability insurance, according to the Massachusetts exemption guidance. The takeaway is simple. “Owner” is not a magic word. Eligibility has to be documented.

That same logic applies in Florida. If you're a corporate officer, LLC member, or sole owner, your title alone doesn't settle the matter. Your ownership records, entity filings, and active status all have to line up with what you're claiming.

The two Florida questions that matter most

Start with these:

What type of entity do you have?

A corporation and an LLC don't always get treated the same way in workers' comp administration. Officer records, member records, and state registrations need to match the exemption request.What industry are you in?

Construction tends to get more scrutiny than lower-risk office operations. That's not a moral judgment. It's because injury exposure and worker classification issues are more common.

Here's the practical breakdown:

| Issue | Why it matters |

|---|---|

| Entity records | Your exemption request has to match how the business is actually formed and registered. |

| Ownership proof | The state wants documented eligibility, not verbal explanations. |

| Role in the business | Officer, member, partner, and employee are not interchangeable labels. |

| Industry risk | Construction and similar fields draw tighter review because mixed workforces create more classification disputes. |

Construction owners need to be extra careful

If you operate in construction, don't wing this.

Construction companies often use a rotating mix of laborers, crew leads, subcontractors, and owner-operators. That makes exemption decisions more fragile because the line between exempt owner and working employee gets blurry fast. The moment your records stop matching reality, your savings strategy becomes a liability strategy.

That matters even more when injuries happen. If a worker gets hurt and classification becomes part of the dispute, you're no longer talking about paperwork. You're talking about exposure, claims, and legal arguments. If you want to understand the claims side of that equation, this overview of workers compensation claims adds useful context.

Good compliance records do two jobs. They support the exemption when it's valid, and they protect the business when someone questions it later.

The cleanest approach is to verify your entity status, officer or member records, payroll treatment, and hiring model before you file. If any of those are fuzzy, the exemption is not your first problem.

How to File for a Workers Comp Exemption in Florida

Filing for exemption in Florida is administrative work, not casual paperwork. That matters because owners tend to treat it like a one-time online task. It isn't.

Florida's Division of Workers' Compensation is the sole authority for processing exemptions. The state generally reviews a Notice of Election to be Exempt within 30 days, and approved exemptions are valid for two years. Renewal should be filed no more than 90 days before expiration, based on the process details summarized in New York's discussion of purpose-limited exemption documents and Florida's procedural framework in the CE-200 certificate guidance.

That means you're dealing with a time-bound compliance document. Not a forever status.

The filing process in plain English

Most owners should think about it in four stages:

- Confirm eligibility first: Check that your ownership, entity records, and role support the exemption you're requesting.

- Prepare matching records: Your state registrations, officer or member details, and related business information should all match.

- Submit the election through the state process: Owners often rush at this stage. Don't.

- Track the expiration date immediately: Waiting until the last minute is how exemptions lapse.

If you already have an exemption and need the renewal side handled correctly, this resource on Florida workers comp exemption renewal lays out what to review before you submit.

What owners usually get wrong

The filing itself isn't the only risk. The bigger issue is what happens around the filing.

Some owners apply before checking payroll classification. Others submit the form but never update internal records. Some renew late. Some keep using old certificates long after the facts have changed. None of that is harmless.

Here's the mindset you want:

An exemption should be managed like a license. It has a purpose, a term, and a paper trail.

A short checklist before you click submit

- Business status: Is the entity active and in good standing?

- Ownership records: Do they match what you're claiming?

- Payroll treatment: Is owner compensation separated cleanly from employee wages?

- Hiring model: Have you added anyone who changes your coverage obligations?

- Calendar controls: Does someone own the renewal deadline?

If nobody in your business can confidently answer those questions, you don't have an exemption process. You have a future cleanup project.

The Financial Risks of Managing Exemptions Yourself

Consequently, the cheap option gets expensive.

Business owners often focus on the premium they might save. They ignore the cost of getting the classification wrong, the filing wrong, or the recordkeeping wrong. That's backwards. Insurance cost is visible. Compliance failure shows up later, usually at the worst possible moment.

Risk one is personal exposure

States evaluate actual job control, not just titles, and exemptions can be denied if someone is really functioning as an employee. Exempt workers may also have to pay out of pocket for medical bills and lost wages. The classification risk is especially serious in industries like construction and healthcare, where mixed employee and contractor workforces are common, as explained in this overview of workers' comp exemption risks.

In plain terms, if you exempt yourself and then get hurt, you may have traded premium savings for uncovered loss. That trade can look clever in a spreadsheet and awful in real life.

Risk two is the contractor trap

Owners love to say, “They're all 1099s.”

Auditors and claims reviewers love to ask, “Are they?”

If you control the schedule, provide the tools, direct the work, and pay like an employee relationship exists, the label won't save you. That's why construction businesses need more than a certificate. They need a full insurance and classification strategy. If you work in the trades, this overview of business insurance for contractors is a practical companion to the exemption discussion.

Risk three is accounting chaos

This is the part owners underestimate because it looks boring.

A workers' comp exemption affects payroll coding, officer compensation tracking, onboarding documents, and sometimes contract compliance. If your bookkeeping is loose, you won't know whether wages were coded properly. If payroll is inconsistent, you won't know whether someone was treated like exempt ownership in one file and like an employee in another. That inconsistency is exactly what creates audit headaches.

Here's what clean administration usually requires:

- Separate compensation treatment: Owner or officer pay shouldn't be mixed carelessly with employee wage records.

- Current supporting documents: Entity filings, ownership records, and exemption status should agree.

- Consistent worker onboarding: Contractor versus employee decisions need documentation, not vibes.

- Review after business changes: New hires, new roles, and entity changes can break an old assumption.

Most exemption problems don't start with fraud. They start with sloppy records, assumptions, and a deadline someone forgot.

This is why I'm opinionated about DIY compliance. Owners should run the business. Your CPA, payroll specialist, and fractional CFO should stress over how wages are coded, how labor is classified, how tax law changes affect reporting, and whether the paper trail will survive scrutiny. That division of labor is cheaper than cleaning up after a bad filing.

When to Call a CPA Instead of Filing for Exemption

If your business is simple, has no employees, and your records are clean, an exemption question may stay narrow.

That is not most businesses.

Once you have mixed labor, officer pay, seasonal staffing, contract requirements, healthcare payroll complexity, or projects across jurisdictions, the primary question stops being “how do I file?” and becomes “how do I avoid making an expensive mistake?” That's when you call a CPA.

The trigger points that mean you need help

You should stop DIYing this if any of the following are true:

- You operate in more than one state: Workers' comp rules are rooted in state labor laws, and the thresholds vary. For example, South Carolina requires coverage for employers with 4 or more employees and payroll above $3,000, while Georgia requires coverage for employers regularly employing 3 or more persons, according to the Pennsylvania compliance summary covering state examples. If you work near state lines or across multiple markets, assumptions will hurt you.

- Your payroll setup is messy: Exemption questions become accounting questions fast.

- You're changing entity structure or ownership: That can change eligibility and documentation requirements.

- You bid jobs that require proof of compliance: Sloppy files can cost contracts.

- You use contractors heavily: Classification risk rises when labor models get flexible.

Why a fractional CFO is the smarter move

A solid fractional CFO doesn't just ask whether you can cut an insurance line. They ask whether the savings are real after you factor in exposure, payroll treatment, tax planning, job costing, and contract requirements.

That's the part small businesses miss. A workers' comp exemption might save money in one narrow lane while creating bigger problems in five others. A good advisor looks across the whole system.

One practical option is working with a firm that handles both the accounting side and the compliance side, such as the services outlined by Bookkeeping and Accounting of Florida Inc. for CPA and bookkeeping support. The point isn't to buy a buzzword. The point is to have someone own the numbers, deadlines, records, and risk logic before the state or an insurer asks awkward questions.

If an exemption decision touches payroll, insurance, tax treatment, and hiring, it belongs on a CPA's desk before it reaches the state's desk.

The safest path is boring. Verify eligibility. Clean up the books. Fix payroll. Review classification. Track renewals. Document everything. That's not flashy, but it's how stable companies stay compliant and protect cash.

If you're asking what is workers comp exemption because you want to lower overhead without stepping into an audit or uncovered liability, talk to Bookkeeping and Accounting of Florida Inc.. A good CPA and fractional CFO can review your entity setup, payroll, worker classification, compliance deadlines, and reporting process so you make a decision that saves money instead of creating a bigger bill later.