You’re probably here because something that felt modern and convenient has now become a tax headache.

A Jacksonville contractor took payment in Bitcoin for a job. A clinic owner parked some excess cash in crypto. A startup founder used digital assets to pay a vendor, then realized tax season doesn’t care how advanced the payment method looked at the time. The minute crypto touches your business, your bookkeeping, tax reporting, and cash-flow planning get more complicated.

That’s why people search crypto tax near me. They don’t want theory. They want a local professional who can look at the mess, tell them what matters, and keep them out of trouble.

Navigating Crypto Taxes A Guide for Jacksonville Businesses

If you run a business in Northeast Florida, crypto can sneak into your books faster than most owners expect. One transaction becomes ten. One wallet becomes three. Then tax time arrives, and suddenly you’re trying to remember whether that ETH payment was income, an investment transfer, or both.

Jacksonville businesses deal with this in very practical ways. A construction company might accept crypto from a client who wants to move fast. A healthcare practice owner might personally understand digital assets and decide to hold some in the business. A nonprofit might receive a donation tied to crypto activity and have no idea how to document it properly. None of that is unusual anymore.

Why local businesses get tripped up

Most business owners think in cash. Money comes in, bills go out, payroll clears, and the books should match the bank. Crypto doesn’t behave that neatly.

The IRS treats crypto as property for federal tax purposes. That means a sale, trade, or spend can create a tax event. If you receive crypto for services, that can also trigger income recognition at fair market value. In plain English, crypto is not a magic side bucket your accountant can “sort out later.”

Practical rule: If crypto touched revenue, treasury, vendor payments, or owner distributions, assume it belongs in the books until a CPA proves otherwise.

A lot of online content misses the local angle. Jacksonville business owners don’t just need generic crypto guidance. They need advice that accounts for how Florida businesses operate, how local industries manage books, and how crypto affects payroll, job costing, financial statements, and owner tax planning.

Why this matters more now

Federal oversight is tightening, and sloppy records are becoming expensive. If you’ve seen news about proposals like the Bitcoin For America Bill, you already know digital assets are moving closer to the mainstream financial system. That doesn’t simplify tax compliance. It raises the stakes.

Here’s the blunt version. If your books are clean, crypto is manageable. If your books are messy, crypto acts like a leaf blower in a dust-filled garage. Everything gets worse, fast.

That’s why the smart move isn’t waiting until filing season. It’s getting your records organized now, before the IRS, your tax preparer, or your lender starts asking questions you can’t answer.

Crypto Tax 101 The Rules Every Florida Business Must Know

A Jacksonville owner takes payment in Bitcoin on Monday, uses some of it to pay a contractor on Thursday, and figures the accountant can sort it out at year-end. That is how a simple week turns into a bookkeeping mess.

Here is the rule that clears the fog. The IRS treats crypto as property, not cash. Once you accept that, the rest starts to make sense. Property rules mean basis, holding period, fair market value, gain, and loss. Cash rules do not.

What counts as taxable

Your business usually triggers tax consequences when it sells crypto, trades one token for another, spends crypto, or receives crypto for goods or services. Each event needs a date, a dollar value, and support in the books. If you cannot prove those three things, you are guessing on a tax return. Guessing is expensive.

Florida gives Jacksonville businesses a real planning advantage. There is no Florida state income tax, so you are not stacking state income tax on top of federal crypto reporting. That point gets missed in national articles, and it matters. It does not erase federal tax. It gives you more room to plan cash flow, owner distributions, and estimated payments with a fractional CFO instead of scrambling at filing time.

The clean way to understand it

Use this framework:

- Receive crypto in the business: usually taxable as income at fair market value when received.

- Sell, swap, or spend that crypto later: usually creates a separate gain or loss.

- Buy and hold only: generally no tax event yet.

That means one coin can create two tax moments. First when it comes in. Second when it goes out.

Receiving crypto for services works like getting paid with a piece of equipment instead of a check. You still have income on day one. If the value changes before you use or sell it, you have another tax issue later. Same coin. Two separate entries. That is where sloppy books start breeding like palmetto bugs.

Common Crypto Taxable vs. Non-Taxable Events

| Activity | Is it a Taxable Event? | Why? |

|---|---|---|

| Buying crypto and holding it | No | Buying and holding by itself generally does not trigger tax |

| Selling crypto for dollars | Yes | Disposal of property can create a gain or loss |

| Trading one crypto for another | Yes | Exchanging property for different property is generally taxable |

| Spending crypto on goods or services | Yes | Using crypto is treated like disposing of it |

| Receiving crypto as payment for services | Yes | It is income at fair market value when received |

| Holding crypto over time | No | Mere holding does not itself create tax |

| Moving crypto between records you own | It depends on facts and documentation | The issue is proving ownership continuity and accurate basis records |

Holding period changes the bill

Owners love to focus on whether they made money. Fine. The IRS also cares how long the business held the asset before it was disposed of.

A short holding period usually means short-term treatment. A longer holding period may qualify for long-term capital gain treatment. That timing difference can change the federal tax result in a meaningful way, which is one more reason Florida’s no-state-income-tax setup is useful but not enough by itself. State tax savings are nice. Federal mistakes still hurt.

If you want a plain-English read on where enforcement pressure is heading, read The Crypto Tax Crackdown. The message is simple. Casual recordkeeping is over.

What Florida businesses should actually do

Jacksonville companies should treat Florida’s tax climate as a planning advantage, not a free pass. The smart play is pairing clean compliance with better decision-making. That is CFO work, not just return prep.

Start here:

- Track receipt dates and times: holding period starts there.

- Record fair market value at receipt: that drives income reporting.

- Separate business wallets from personal wallets: mixed activity wastes billable hours and creates audit risk.

- Document every disposal: selling, swapping, and spending all need support.

- Tie crypto activity to your financial statements: if it affected revenue, expenses, treasury, or owner draws, it belongs in the books.

Florida gives you breathing room because there is no state income tax. Good. Use that room wisely. Clean records, clear policy, and actual planning will save far more money than dumping wallet exports on your CPA in March and hoping for mercy.

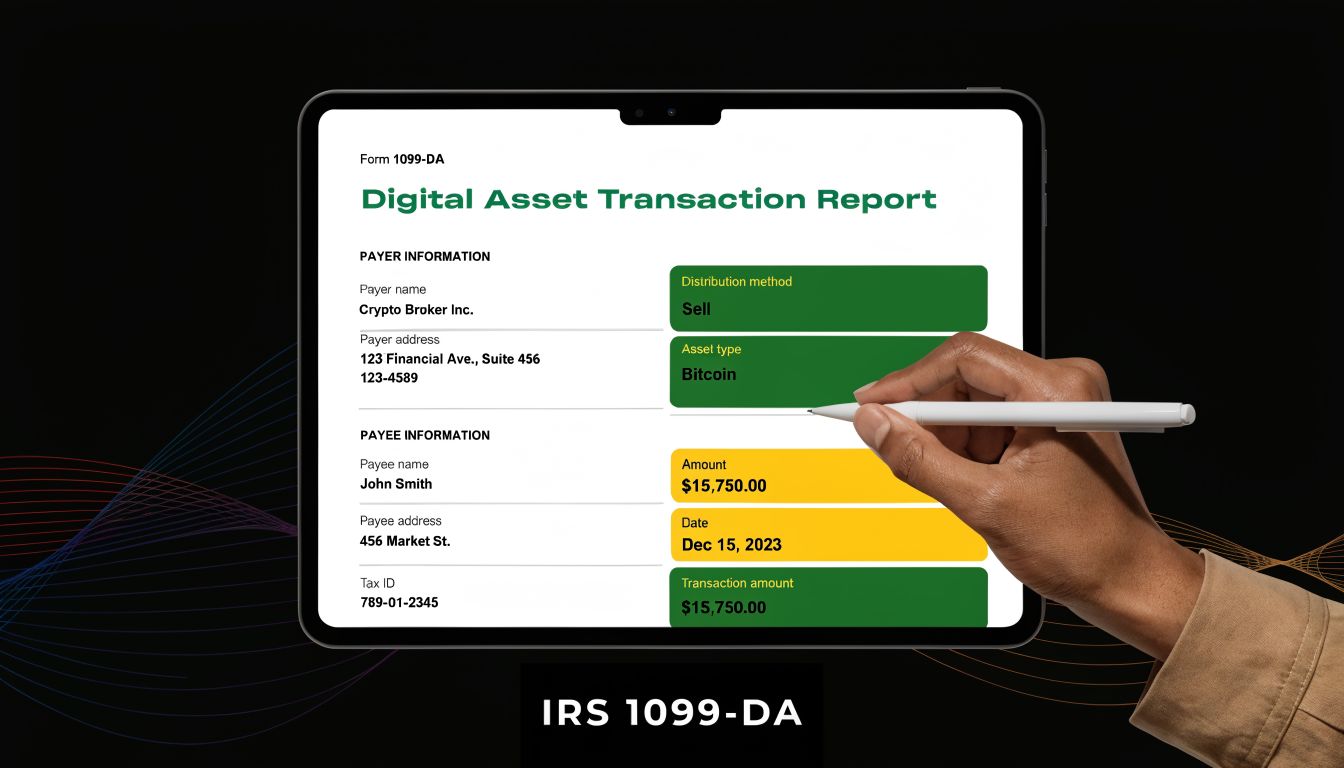

The 2026 IRS Crackdown What Form 1099-DA Means for You

A Jacksonville business owner sells crypto to cover payroll, swaps one token for another, then gets a tax form the next year that shows the IRS a disposal happened. If the books do not clearly show basis, dates, and business purpose, the IRS starts with the form in front of them, not your intentions.

For the 2025 tax year, filed in 2026, Form 1099-DA requires brokers to report digital asset transaction information to the IRS. Plunkett Cooney’s writeup on crypto tax reporting requirements lays out the broad reporting shift and the penalty exposure that comes with getting it wrong.

What changed

The old habit was sloppy but common. Business owners pulled exchange exports, guessed at basis, dropped numbers into software, and hoped nothing bounced. That era is over.

Form 1099-DA matters because brokers will report digital asset sales and other transaction details directly to the IRS. In some cases, cost basis information may be included if the broker has it. In many real-world business situations, they will not have the full story.

That gap is where trouble starts.

An exchange may see that your company sold Bitcoin. It may have no idea what happened before that if the asset came in from another wallet, was used across platforms, or was originally received as customer payment. So the IRS gets one piece of the movie, and your return has to supply the rest.

Why Jacksonville businesses should care now

Florida gives you a real planning advantage because there is no state income tax. Good. That means one less tax layer to manage on crypto gains at the state level.

It does not excuse weak federal reporting. It gives you more room to make smart treasury and tax decisions.

That distinction matters for Jacksonville companies using crypto in operations, not just speculating on the side. If you accept digital assets, hold them, convert them, or use them to pay for business expenses, you need a reporting system and a cash strategy. That is fractional CFO territory. Basic tax prep at filing time is too late and too narrow.

Your exchange is not your bookkeeper. Your wallet is not your general ledger. And your memory is not an audit file.

What will get attention

The IRS will care about whether your return matches the forms it receives and whether your records can support any differences.

Expect pressure around:

- Reported disposals: if a broker reports a sale or exchange, your return needs to address it

- Transaction dates: timing affects gain or loss reporting and holding period treatment

- Asset identification: Bitcoin, Ethereum, stablecoins, and token-to-token swaps cannot be mashed together like a junk drawer

- Basis support: if the broker does not have complete basis data, your records have to carry the load

- Business purpose: owner activity and company activity need clear separation

A practical overview from tax counsel is The Crypto Tax Crackdown, which explains why casual crypto reporting is becoming a very expensive habit.

Here’s a quick explainer for the rule change and why it matters in real life:

What a smart business owner does now

Reconcile throughout the year. Do not wait for a form to arrive and then act surprised.

Your books should tie wallet activity, exchange records, invoices, receipts, and bank activity together in one clean chain. If your company uses QuickBooks, every crypto entry should point to real support. “Crypto thing” is not an accounting policy. It is a confession.

The businesses that handle this well use Florida’s no-state-income-tax advantage as breathing room to make better federal decisions. They set policy, track basis, separate owner transactions from company transactions, and review tax impact before making moves. That is how you stay compliant and keep options open.

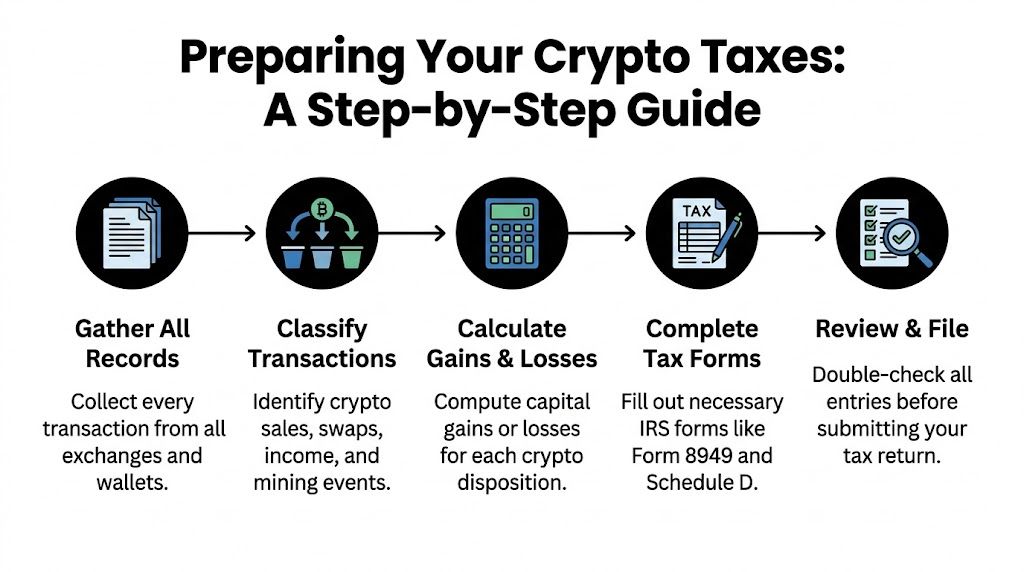

Preparing Your Crypto Taxes A Step-by-Step Guide

Friday afternoon. Your controller is trying to close the books, your exchange CSV looks like it was built by raccoons, and somebody asks whether that USDC payment from March was income, inventory, or a transfer. That is how crypto tax trouble starts.

A clean filing starts with process. Jacksonville businesses already have one advantage national articles usually miss. Florida does not hit you with state income tax, so you have more room to make smart federal moves, set policy early, and use fractional CFO oversight for planning instead of spending every ounce of energy cleaning up a mess in April.

Step 1 Gather every record before you touch the return

Pull records from every exchange, wallet, payment processor, custody platform, and accounting system the business used. Include invoices, receipts, bank activity, and any internal logs tied to customer payments or vendor payouts.

If one wallet is missing, the whole schedule can go crooked. Good preparation starts with a full map of the activity, not a half-remembered story from the owner.

Step 2 Classify each transaction by what it actually was

Crypto bookkeeping falls apart when businesses label everything “investment activity” and move on. That is lazy accounting.

Separate transactions into the right buckets:

- Crypto received from customers: usually business income at fair market value on the receipt date

- Sales for cash: potentially capital gain or loss, depending on the facts

- Token-for-token trades: often taxable disposals

- Staking rewards, airdrops, or similar receipts: may create ordinary income and need clear support

- Wallet-to-wallet transfers: usually not taxable, but they still need to be documented correctly

This step matters because the tax treatment follows the facts, not the nickname someone gave the transaction in QuickBooks.

Step 3 Calculate basis and choose a method you can defend

Once transactions are classified, calculate cost basis and proceeds for each disposal. The IRS addresses digital assets in its Digital Assets page, and accepted accounting treatment depends on records that support the method you use.

FIFO is common. Specific identification can produce better results if the records are clean enough to support it. HIFO may help in the right file, but only if you can prove which units were sold. If you cannot prove it, you do not have a strategy. You have a guess wearing a tie.

If the business received crypto as payment and sold it later, keep both tax layers separate. First comes income when the asset hits your hands. Later comes gain or loss when you dispose of it.

Step 4 Reconcile your records to any broker forms

If a Form 1099-DA or another broker statement shows up, reconcile it line by line to your books. Do not drop the form into tax software and hope for the best.

Check dates, proceeds, asset descriptions, and basis support. Broker reporting may be incomplete, especially when assets moved on and off platform. Your records need to explain the full chain of custody. That discipline also makes audit preparation for financial records much less painful if the IRS comes asking questions.

Step 5 Report disposals on the right forms

For many filers, crypto sales and exchanges flow through Form 8949 and then to Schedule D. The IRS instructions for Form 8949 and Schedule D spell out how capital transactions are reported and summarized.

At the practical level:

- List each taxable disposal with acquisition date, disposal date, proceeds, and basis.

- Apply your supported accounting method consistently.

- Roll totals to the proper summary form instead of leaving detail stranded in a spreadsheet.

- Tie the return back to the books so every reported number has support.

If the business accepted crypto for goods or services, that income also has to hit the correct business return lines. A Jacksonville company benefits from real planning in this regard. Florida’s no-state-income-tax setup gives you room to focus on federal reporting strategy, cash flow, and entity-level decisions, which is exactly where a fractional CFO earns the fee.

Step 6 Review like someone is about to challenge every line

Good review catches the usual wreckage:

- exchange activity missing from the books

- proceeds reported without basis support

- the same income entered twice

- owner transactions mixed with company records

- transfers coded as sales

- balances that do not tie to year-end holdings

A final review should answer one blunt question. If the IRS asks how you got the number, can you show the trail in five minutes?

That is the standard. Meet it before filing, not after the notice arrives.

Common Crypto Tax Mistakes and How to Avoid Costly Audits

A Jacksonville business owner takes payment in Bitcoin, swaps a few tokens during the year, moves coins between wallets, and hands the CPA a spreadsheet in March that looks like it survived a hurricane. Then comes the surprise. Florida has no state income tax, but the IRS still expects clean federal reporting, and sloppy crypto records are easy to spot when the numbers do not tie.

That Florida tax advantage matters, but not in the way many owners assume. It does not erase crypto tax rules. It gives you room to make smarter federal tax, cash flow, and entity decisions instead of wasting time on a state income tax return. That is a planning opportunity, not a free pass.

Here are the mistakes that trigger the most trouble.

Mistake one treating crypto revenue like it only matters at sale

If your business accepts crypto from a customer, the tax issue usually starts when you receive it, not months later when you sell it. The fair market value on the receipt date can create business income. Later, when you sell, convert, or spend that crypto, you may also have a gain or loss.

Miss the first entry and revenue is understated. Miss the second and basis is wrong. Either way, your books stop matching reality.

Mistake two assuming crypto-to-crypto swaps are invisible

Business owners say this all the time. “We never cashed out.”

That does not help. Swapping one coin for another can still create a taxable disposition. The account may feel like a trading app. The IRS treats it like property changing hands.

Mistake three keeping weak cost basis records

Bad basis records are how small errors turn into ugly audits.

If you cannot show when the asset was acquired, what the business paid, what fees were involved, and how it moved between wallets, you are guessing at gain or loss. Guessing is not a tax method. It is a donation to future penalties and accountant fees.

If your records need cleanup, do it before the return goes out. If you want a practical checklist, review this guide on how to prepare for an audit.

Clean books make an audit manageable. Dirty books make it expensive.

Mistake four mixing personal wallets with company activity

A business wallet should hold business activity. Simple.

Once an owner runs company receipts, personal trades, reimbursements, and random transfers through the same wallets, the audit trail turns into soup. That creates tax problems, bookkeeping problems, and control problems. It also makes lender reviews and financial statement work harder than they need to be.

Mistake five trusting software to make judgment calls

Crypto software is useful. It is not a controller, a CFO, or a CPA.

Import tools can pull transactions. They cannot tell whether a transfer was payroll, customer revenue, an owner contribution, treasury management, or a personal expense shoved into the wrong wallet. Software organizes data. A professional decides what the data means and how it belongs on the return.

What to do instead

Use a stricter process than you think you need.

- Separate business and personal wallets: no exceptions, no “just this once.”

- Record activity as it happens: year-end reconstruction is slow, expensive, and usually wrong.

- Keep support for value, basis, and business purpose: invoices, exchange records, wallet logs, and approvals matter more than screenshots alone.

- Review entity structure and cash flow strategy: Florida’s no-state-income-tax setup gives Jacksonville businesses flexibility, and that is exactly why crypto should be reviewed as a CFO issue, not just a tax prep task.

- Get a real review before filing: especially if you used multiple exchanges, self-custody wallets, staking, or DeFi.

DIY works for assembling patio furniture. It is a lousy plan for crypto compliance when the return belongs to a real business and the IRS gets to ask follow-up questions.

Why Your Business Needs a Fractional CFO for Crypto Strategy

A tax preparer looks backward. A fractional CFO looks forward.

That distinction matters when crypto enters a business. If your company holds digital assets, accepts them from customers, or uses them in treasury decisions, you don’t just have a tax task. You have a strategy issue.

Crypto creates business decisions not just tax entries

Should the business hold crypto at all? If so, how much? In which entity? With what internal controls? What happens to cash flow if the asset swings hard before payroll, rent, or vendor payments clear?

Those are CFO questions. They affect operations, not just tax forms.

What a fractional CFO actually does here

A good fractional CFO helps a Jacksonville business do four things well:

- Set policy: decide whether the company will accept, hold, convert, or restrict crypto use.

- Control risk: create approval workflows, wallet access rules, and documentation standards.

- Protect cash flow: prevent treasury decisions from colliding with payroll and operating needs.

- Align reporting: make sure tax records, books, and management reporting tell the same story.

That beats the common small-business approach, which is usually some version of “our office manager exported a file and we’ll figure it out later.”

Why this matters in Florida

Florida’s tax climate makes crypto more attractive to some business owners, but that same advantage can tempt companies into activity they aren’t prepared to manage well. The tax angle is only one piece. The operational side is where many businesses stumble.

A fractional CFO brings discipline. Not hype. Not social media chatter. Discipline.

If you’re evaluating whether this level of guidance makes sense, this overview of fractional CFO services is a useful starting point for understanding the role.

If crypto is large enough to affect your cash, risk, reporting, or owner decisions, it’s large enough to deserve CFO oversight.

The real business value

Most SMBs don’t need a full-time CFO. They do need someone who can connect tax, bookkeeping, forecasting, and internal controls.

That’s especially true in industries like healthcare, construction, retail, and nonprofits, where timing, compliance, and reporting discipline matter. Crypto doesn’t replace those basics. It punishes businesses that ignore them.

A seasoned advisor helps you avoid random decisions. That alone can save an owner from a year of bad accounting and worse stress.

How to Find the Best Crypto Tax CPA Near Me in Jacksonville

Search crypto tax near me and you’ll find plenty of generic national firms, ad-heavy directories, and vague promises about “maximizing your return.” That’s not enough for a Jacksonville business.

The local gap is real. Most search results don’t explain how Florida’s no-state-tax structure can create a 5-7% savings advantage over higher-tax states, or how a local CPA can connect that benefit to job costing and financial strategy for SMBs, according to Crypto Tax Girl’s analysis of the local content gap.

What to look for in a Jacksonville crypto tax CPA

Use a practical checklist.

- Local Florida knowledge: your CPA should understand that Florida’s tax advantage helps, but federal compliance still drives the reporting work.

- Business accounting strength: crypto for a business isn’t just a return issue. It lives in the books all year.

- Industry familiarity: healthcare, construction, retail, and nonprofits all have different reporting pressures.

- QuickBooks competence: if the books are messy, tax prep gets slower and more expensive.

- Strategic capability: you want someone who can advise on controls, timing, and planning, not just data entry.

- Audit readiness mindset: good firms prepare files as if someone may review them later.

Questions worth asking

When you interview a CPA, don’t ask only, “Do you do crypto taxes?”

Ask better questions.

- How do you reconcile exchange records to the books?

- How do you handle basis issues across wallets and platforms?

- How do you separate owner activity from business activity?

- Can you help with policy, internal controls, and ongoing financial guidance?

- Do you offer support beyond return prep, including bookkeeping and advisory?

If the answers sound fuzzy, keep looking.

What the right local partner should provide

A strong Jacksonville firm should be able to help with cleanup, monthly bookkeeping, tax prep, and higher-level guidance. That combination matters because crypto problems usually start in bookkeeping long before they show up on the tax return.

If you want a local option focused specifically on this area, review this page for a crypto tax accountant in Jacksonville.

The best CPA for crypto isn’t the one with the flashiest ad. It’s the one who can keep your books clean, your filing defensible, and your business calm when tax season gets noisy.

If your business has touched crypto in any way, now’s the time to get the books cleaned up and the reporting handled correctly. Bookkeeping and Accounting of Florida Inc. helps Jacksonville and Northeast Florida businesses stay compliant, organize messy records, and get the kind of bookkeeping, tax, and fractional CFO guidance that keeps small problems from turning into expensive ones.