You're usually not reading about workers' comp because you're curious. You're reading because a premium jumped, an agent asked for payroll detail you don't have organized, or an audit notice landed at the worst possible time.

That frustration is normal. Workers' compensation feels opaque because most owners only see the bill, not the mechanics behind it. In Florida, that's dangerous. If you guess at payroll, misclassify workers, or treat the annual premium like a fixed cost instead of a moving target, you can overpay, underbudget, or create a compliance problem that shows up later when cash is already tight.

A smart owner should understand how to calculate workers compensation well enough to ask better questions, catch expensive mistakes, and keep the business audit-ready all year.

Why Your Workers Comp Premium Can Feel Unpredictable

One month, the estimate looks manageable. Later, the renewal shows up and the number has changed. Then an audit request follows, and suddenly your office manager is pulling payroll reports from QuickBooks, job descriptions from old files, and contractor paperwork from three different folders.

That's the core reason workers' comp feels unpredictable. The problem usually isn't the formula. The problem is bad inputs, incomplete records, and a business owner who was never given a clean operating system for payroll and classification in the first place.

The bill changes because your business changes

If your company hires more field labor, adds a new service line, shifts admin staff into operations, or pays irregular overtime, your workers' comp cost can move with it. Construction companies in Jacksonville see this all the time. A crew mix change can alter premium exposure fast. Healthcare practices run into a similar issue when clinical and non-clinical roles get lumped together instead of separated correctly.

That's why workers' comp belongs in financial management, not just insurance administration. It affects margin, forecasting, and compliance.

Clean books don't just help you file taxes. They help you defend payroll classifications and avoid paying for mistakes that should have been caught upstream.

Most owners undercalculate the labor picture

Owners often focus on wages and stop there. That's too narrow. Workers' comp sits inside the broader cost of employing people. If you need a wider lens on labor economics, this UK employee cost calculator guide is a useful example of how employers should think about payroll-related costs as a system, not a single line item.

That mindset matters. If you only react when the workers' comp invoice arrives, you're late. You need to monitor payroll structure, role assignment, and documentation continuously.

Why this matters in Florida

Florida businesses don't get much room for sloppy compliance. If your records are weak, your audit gets harder. If your classifications are wrong, your premium can be wrong. If your payroll process is inconsistent, every downstream report gets less reliable.

Here's the blunt version. Workers' comp isn't just an insurance issue. It's a bookkeeping issue, a payroll issue, a tax reporting issue, and a cash flow issue. Owners who treat it as an annual nuisance usually pay more than they should and spend more time fixing preventable messes.

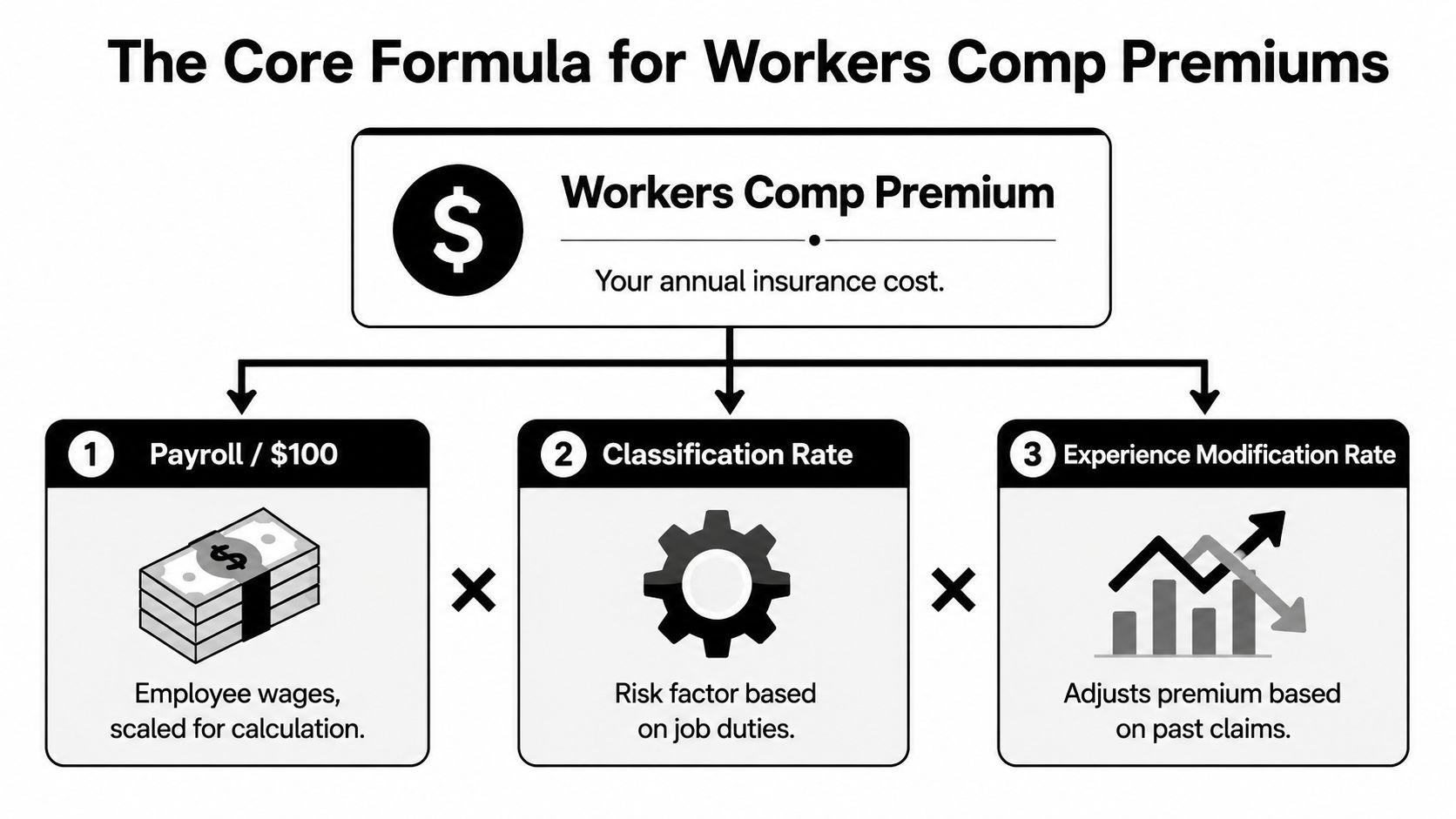

The Core Formula for Workers Comp Premiums

A Jacksonville contractor adds three field hires in June, revenue improves, and the year looks strong. Then the workers' comp audit lands and wipes out part of the margin. The formula did not change. The inputs did.

The basic premium calculation is simple: Classification Rate × Experience Modification Rate × (Payroll / $100) = Premium.

That equation matters because it shows exactly where Florida businesses overpay. They overstate or miscode payroll, assign employees to the wrong class code, or ignore how claims history affects pricing. If you want tighter cost control, start by understanding which part of the formula is driving the premium.

Payroll sets the base of the charge

Payroll is the starting point. Insurers take covered payroll, divide it by $100, and apply the rate tied to each job classification.

That sounds mechanical. It is not.

Workers' comp payroll is usually estimated at the start of the policy and reconciled later. If your business grows faster than expected, adds overtime-heavy crews, or shifts labor into higher-risk work, your final premium can climb fast. That is why clean reporting matters. If your payroll process is weak, fix it before renewal. A stronger payroll processing foundation gives you cleaner estimates, cleaner audits, and fewer expensive surprises.

Classification rates decide how expensive each dollar of payroll becomes

Here, many owners lose money.

A rate is assigned based on the work employees perform, not the title in your HR file. Two companies can run the same total payroll and still pay very different premiums because their labor mix is different. In Florida, that gap gets expensive fast in construction, healthcare, hospitality, and any business with mixed administrative and field duties.

If someone splits time between office work and physical operations, your records need to prove how that time is allocated. If they cannot, the insurer or auditor may default to the higher-rated exposure. That is not a technicality. It is a direct hit to margin.

Your experience modification rate reflects claims performance

The experience modification rate adjusts your premium based on prior loss history. A lower mod reduces cost. A higher mod increases it.

Owners should treat that number as a financial metric, not an insurance footnote. Claims frequency, claim severity, return-to-work discipline, and reporting habits all feed future pricing. Poor claims management raises insurance cost long after the original incident is closed.

Practical rule: If you cannot tie payroll, job duties, and claims history together in your records, you do not have a reliable workers' comp estimate.

For companies weighing direct coverage against outsourced employment arrangements, understanding PEO workers' comp costs can clarify how premium responsibility shifts under different models.

Use the formula as a control tool

The formula gives you three places to intervene:

- Payroll accuracy: Keep covered wages current and coded correctly.

- Classification discipline: Match each worker to the right job-based rate.

- Claims control: Reduce preventable losses and manage open claims tightly.

Business owners who treat workers' comp as a once-a-year insurance bill usually pay more than they should. Owners who use the formula to review payroll structure, job coding, and claims behavior make better forecasting decisions, stay cleaner on compliance, and protect profit.

Gathering Your Key Inputs Accurately

Most premium problems start before the policy is ever priced. They start when the wrong payroll data gets exported, when job duties aren't documented, or when a growing company lets informal staffing decisions spill into formal reporting.

Accurate inputs are the essential work. The formula is easy. The preparation is where businesses either protect margin or lose it.

Start with payroll records you can trust

Your payroll file has to be clean before anything else matters. If your reports are inconsistent, your premium calculation is built on noise. That means your payroll system, charting of wage categories, employee setup, and reporting cadence all have to line up.

If your payroll process needs work, review the basics of payroll processing and tighten that foundation first. Workers' comp depends on payroll integrity. There's no shortcut around that.

Job classification is where many businesses go off track

A worker's classification should reflect what that person does, not what their title says on an offer letter. That distinction matters in Florida industries where mixed duties are common.

Consider a healthcare office. An administrative assistant and a clinical worker may sit in the same building, report to the same manager, and appear on the same payroll run. That does not mean they belong in the same workers' comp classification. Construction companies have the same issue when office staff, estimators, site supervisors, and field labor get blurred together.

A useful outside reference for understanding how class code logic works in practice is this overview of California workers' compensation classification codes. It's from another state, but it illustrates the larger point well. Classifications follow work performed, not convenience.

What to gather before anyone prices or audits your policy

Don't wait for the carrier to ask. Pull the support in advance.

- Payroll detail by employee: Separate roles clearly, especially if your company has office, field, clinical, and management staff under one roof.

- Job descriptions: Keep them current. If duties changed during the year, document when and how.

- Organizational structure: Show who supervises whom and where labor is performed.

- Overtime records: Break out regular and premium pay accurately in your payroll system.

- Contractor documentation: If you use 1099 labor, keep agreements and support organized.

A clean system beats a heroic scramble

Too many owners rely on memory at audit time. That's a mistake. You need a repeatable process inside QuickBooks or your payroll platform that tags workers correctly, captures changes in responsibility, and preserves records in one place.

A good test is simple. If an auditor asked today why one employee was reported under one class and another under a different one, could your team answer in writing, with support, in minutes instead of days?

If the answer is no, your workers' comp issue isn't pricing. It's recordkeeping.

This is also where tax law changes and payroll rule updates matter. Even when a change doesn't directly rewrite workers' comp formulas, it can affect how payroll is coded, reported, or reviewed. Small businesses often miss that interaction because nobody owns the entire process from bookkeeping through payroll through compliance.

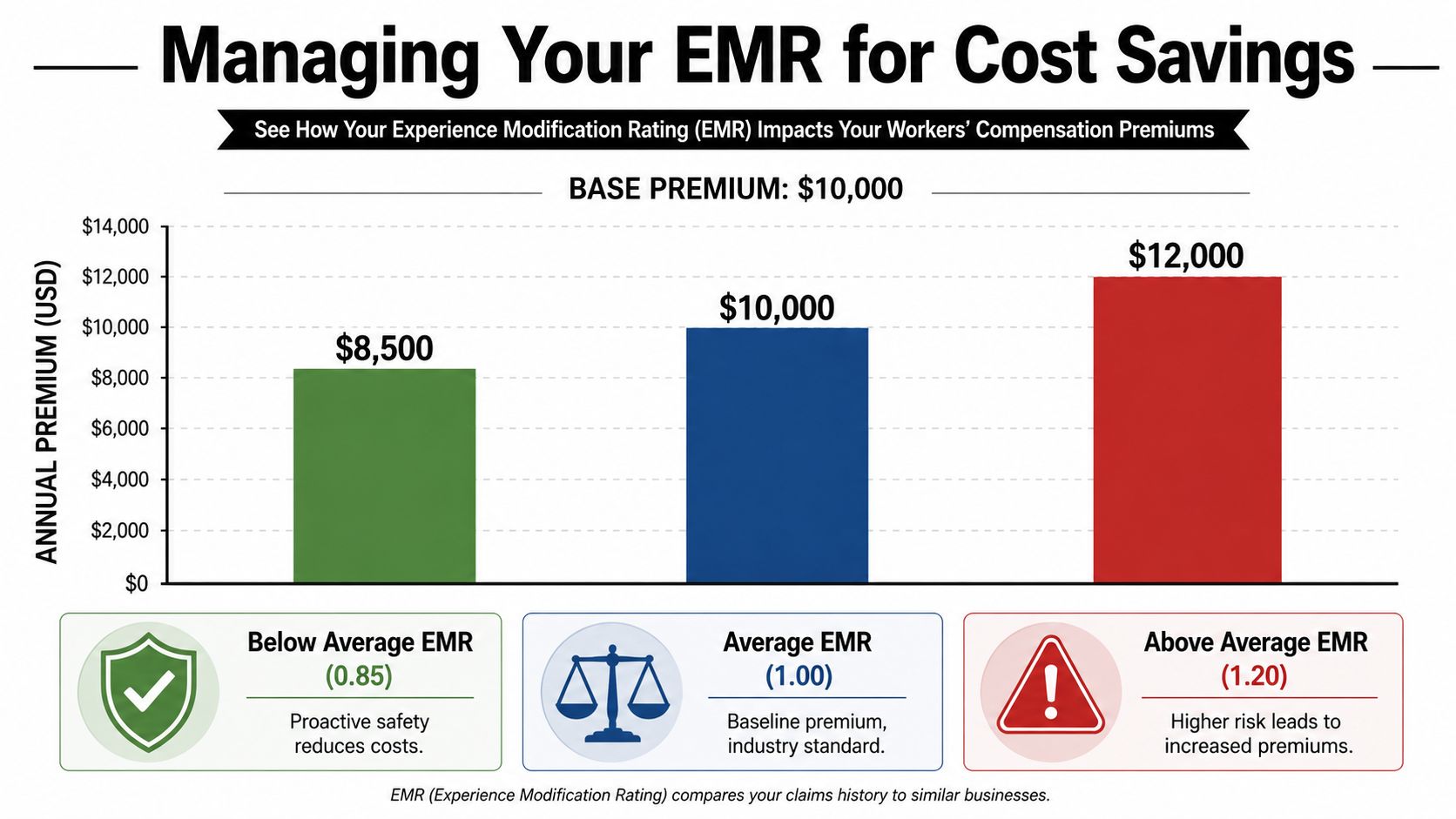

Controlling Costs with Your Experience Modification Rate

There's one part of workers' comp that reflects management quality more than most owners realize. It's your experience modification rate, often called the mod or EMR. This number isn't abstract. It's one of the clearest signals of whether your business controls injuries and handles claims intelligently.

A lot of owners treat workers' comp like weather. They assume the market sets the cost and they just live with it. That's lazy thinking. Your claims history influences your cost structure, and your operating discipline influences your claims history.

What your mod is really telling you

Your experience modification rate adjusts the premium above or below the base amount. A weaker claims record pushes cost up. A stronger one can reduce cost relative to that base. That's the financial consequence of workplace risk showing up in an insurance bill.

If your business keeps having the same injury pattern, that's not an insurance problem. It's an operations problem with an insurance price tag.

The owners who control this number do a few things consistently

They don't wait for renewal to think about claims. They build habits that reduce frequency and severity over time.

- They investigate incidents promptly: Fast fact gathering protects the claim file and helps management fix the actual cause.

- They maintain return-to-work options: Modified duty can reduce the business disruption that follows an injury.

- They train by role: Safety instruction should match what employees really do, not what a generic handbook says.

- They review claims with intent: Open claims should be monitored, not ignored until someone else sends an update.

Why this belongs in finance, not just HR

Too many companies dump workers' comp into HR or operations and never connect it back to margin. That's a mistake. Every avoidable claim can ripple through your insurance cost, staffing continuity, and administrative workload.

A disciplined finance leader looks at EMR as a controllable business variable. Not fully controllable, but absolutely influenceable. If your claims trend is getting worse, your premium problem started long before the renewal meeting.

Strong safety management isn't soft culture work. It's cost control.

The practical takeaway is simple. If you want lower workers' comp costs over time, don't negotiate harder at renewal before you fix what's driving the claims experience underneath it.

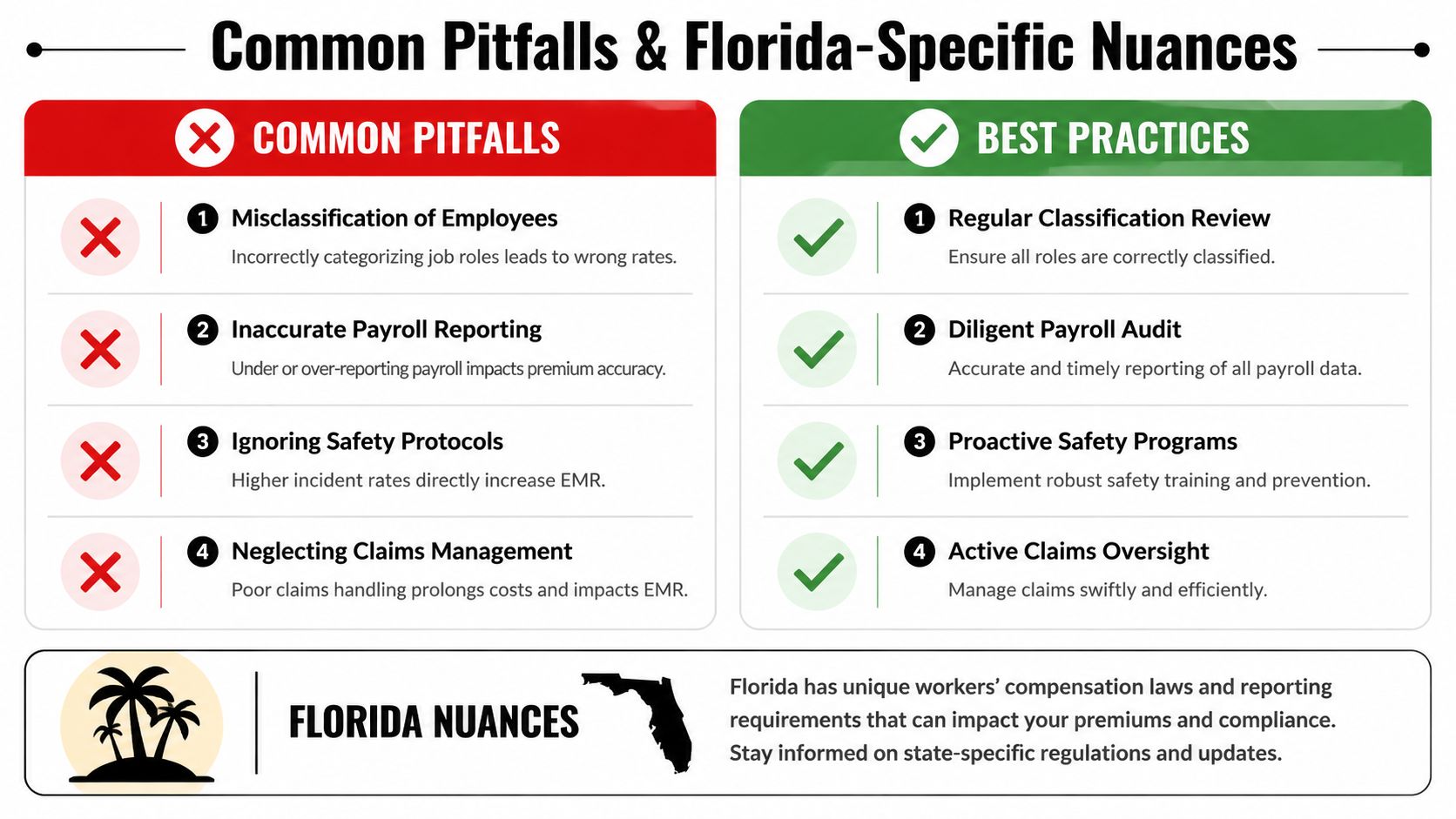

Common Pitfalls and Florida-Specific Nuances

Most online advice on how to calculate workers compensation is too simplistic to be useful. It tells you to multiply payroll by a rate and move on. That's exactly how small businesses drift into overpayment, underdocumentation, and audit trouble.

The expensive mistakes live in the details.

The overtime mistake that quietly inflates cost

One of the most overlooked issues is the distinction between gross wages and subject wages for workers' comp. Thomson Reuters explains that the Excluded Overtime Premium should be subtracted from Gross Wages before determining Subject Wages in its guidance on workers' compensation calculations. That matters because businesses that include all overtime premiums can inflate their workers' comp cost. The same source notes some estimates suggesting small businesses may overpay by up to 15% when they incorrectly include all overtime premiums.

This is exactly the kind of issue owners miss when payroll is processed mechanically instead of reviewed strategically. If your team can't identify the overtime premium portion distinctly in QuickBooks or your payroll reports, you may be paying comp on wages that shouldn't be in the subject wage base.

Florida businesses also get tripped up on worker status

Another recurring issue is treating someone like an independent contractor without having the documentation and facts to support that treatment. If your records are weak, this can become a workers' comp problem fast. Florida business owners should understand when an exemption applies and when it doesn't. If you need a starting point, review this explanation of what is workers comp exemption.

Don't assume a 1099 label solves anything. Classification decisions need support.

The pitfalls that create avoidable cost

Here's where I see owners lose control most often:

| Issue | Why it hurts |

|---|---|

| Misclassified employees | You apply the wrong rate to the wrong payroll base |

| Incomplete payroll coding | Overtime, bonuses, and role-based wages get reported inconsistently |

| Weak documentation | You can't defend the way workers were assigned or paid |

| Reactive compliance | You discover problems only when renewal or audit forces a review |

Tax law changes make payroll discipline more important

The author brief asked for tax law changes, and here's the right way to think about them. The specific change isn't the point unless it directly alters your payroll treatment. The bigger issue is that payroll compliance never stands still. Tax reporting rules, wage handling procedures, and state requirements shift. If your bookkeeping team doesn't reconcile those changes into the way payroll is processed, workers' comp reporting gets less reliable.

Bottom line: The businesses that overpay aren't always reckless. A lot of them are simply operating with outdated payroll assumptions.

Navigating Audits and Managing Costs Strategically

A Florida business owner gets a workers' comp audit notice, pulls payroll reports, and realizes job classifications changed midyear, overtime was handled inconsistently, and contractor files are missing support. That is how a routine audit turns into an expensive bill.

Your premium starts as an estimate. The final number gets settled after the policy period based on what you paid and how that payroll should have been classified. Owners who treat the audit like paperwork usually pay for it twice. First in added premium, then in staff time spent cleaning up records under pressure.

That pressure exposes weak accounting fast. Clean books protect cash.

Audit readiness is a year-round discipline

You prepare for a workers' comp audit by keeping payroll clean every pay period. That means consistent class coding, documented wage treatment, organized contractor support, and clear records for any ownership exemptions or role changes.

If your records are scattered, fix that before the audit notice arrives. This guide on how to prepare for an audit is a practical place to start. The payoff is straightforward. Better records reduce disputes, shorten the audit process, and make it easier to defend the numbers that drive your premium.

Claims accuracy starts with payroll accuracy

Workers' comp cost is not limited to the policy premium. Claims depend on wage records too, and sloppy payroll creates problems on that side of the system as well.

If earnings history is incomplete or coded inconsistently, you create room for disputes over benefit calculations, reserve levels, and claim handling. That matters in Florida because bad payroll records do more than frustrate an auditor. They can distort claim costs, affect your loss history, and put more pressure on future premiums.

Strong financial oversight saves real money

Workers' comp should be managed like a controllable cost, not a surprise expense that shows up at renewal. A good fractional CFO puts structure around payroll controls, certificate tracking, classification review, and audit preparation so problems get caught during the year instead of after the insurer totals everything up.

That matters for compliance, but it also matters for margin. Every preventable classification error, unsupported contractor payment, or messy payroll adjustment can increase your premium or weaken your position during an audit. Fixing those issues early is cheaper than defending them later.

If you want help building that system, Bookkeeping and Accounting of Florida Inc. gives Jacksonville and Northeast Florida businesses the accounting, payroll, audit support, tax guidance, and fractional CFO oversight needed to stay compliant and keep workers' comp from becoming an expensive surprise.