You didn't go to medical school to stare at a Profit & Loss statement and wonder why the bank balance feels tighter than the schedule looks busy. Yet that's where many practice owners land. The waiting room is full, claims are going out, payroll keeps hitting, and somehow cash still feels unpredictable.

That disconnect is the whole story of medical practice financial management. Revenue on paper doesn't pay rent. Profit doesn't guarantee liquidity. A busy practice can still be financially fragile if collections lag, denials pile up, tax planning is sloppy, or no one is steering the numbers with discipline.

If you own a practice in 2026, you need more than bookkeeping. You need controls, forecasting, compliance awareness, and someone who can translate financial noise into decisions.

Why Your Medical Practice Needs a CFO Mindset

Monday starts with a full schedule. By Thursday, you are reviewing payroll, waiting on payer money that should have hit already, and wondering why a busy practice still feels cash-starved. Then your CPA asks for cleaner books, your office manager flags a vendor past due, and the numbers suddenly look less like administration and more like triage.

That is the moment practice owners need to stop acting like the financials are back-office clutter. Shrinking reimbursement and rising compliance pressure punish delay. If nobody is owning cash, margin, tax exposure, and reporting discipline, your practice is operating without a financial driver.

Clinical excellence doesn't fix weak finance

Great care does not protect a weak business model. A packed schedule can still hide slow collections, bloated overhead, poor contract performance, and sloppy reporting. By the time those problems show up in the bank account, they have usually been building for months.

A CFO mindset means you stop treating the books like a historical record and start using them as an operating system. You review results fast. You question swings in labor, supplies, and provider productivity. You compare collections to expectations. You make decisions before pressure turns into a cash problem.

Here is the hard truth. Many physician owners do not need more data. They need better interpretation and stronger accountability.

Practical rule: If you cannot explain your cash position, tax exposure, and biggest margin leak in plain English, you are not managing the practice. You are reacting to it.

What a CFO mindset looks like

A CFO mindset is not corporate theater. It is a set of habits and clear ownership.

- Watch cash every week. Bank balance alone is a false comfort. You need expected inflows, scheduled outflows, and a clear view of what is already spoken for.

- Separate volume from profit. More visits do not automatically mean better performance. Some service lines create work without creating margin.

- Find the leak. Every practice has one. It may be payer underpayments, overtime, poor scheduling templates, weak point-of-service collection, or aging A/R. Identify it and fix it.

- Assign the right people. Your biller should own clean claims. Your bookkeeper should keep records current. Your CPA should handle tax strategy and compliance. A fractional CFO should translate all of it into decisions.

- Review numbers on a cadence. Monthly is the minimum. Weekly review is better when cash is tight, growth is fast, or payer behavior is getting worse.

If you want a stronger practice, build the finance function the same way you build clinical operations. Put the right specialist in the right seat. A physician should not be chasing coding edits, cleaning up the general ledger, and guessing at quarterly taxes. That is how profitable practices get blindsided.

Owners who adopt this mindset run tighter, safer businesses. They know what their practice can afford, when to hire, when to cut, and when an apparent growth opportunity will drain cash. They also know when to bring in outside help, including a team that understands healthcare revenue cycle management services, bookkeeping, tax planning, and higher-level financial oversight.

That is not theory. It is survival. It is also how a practice grows without losing control.

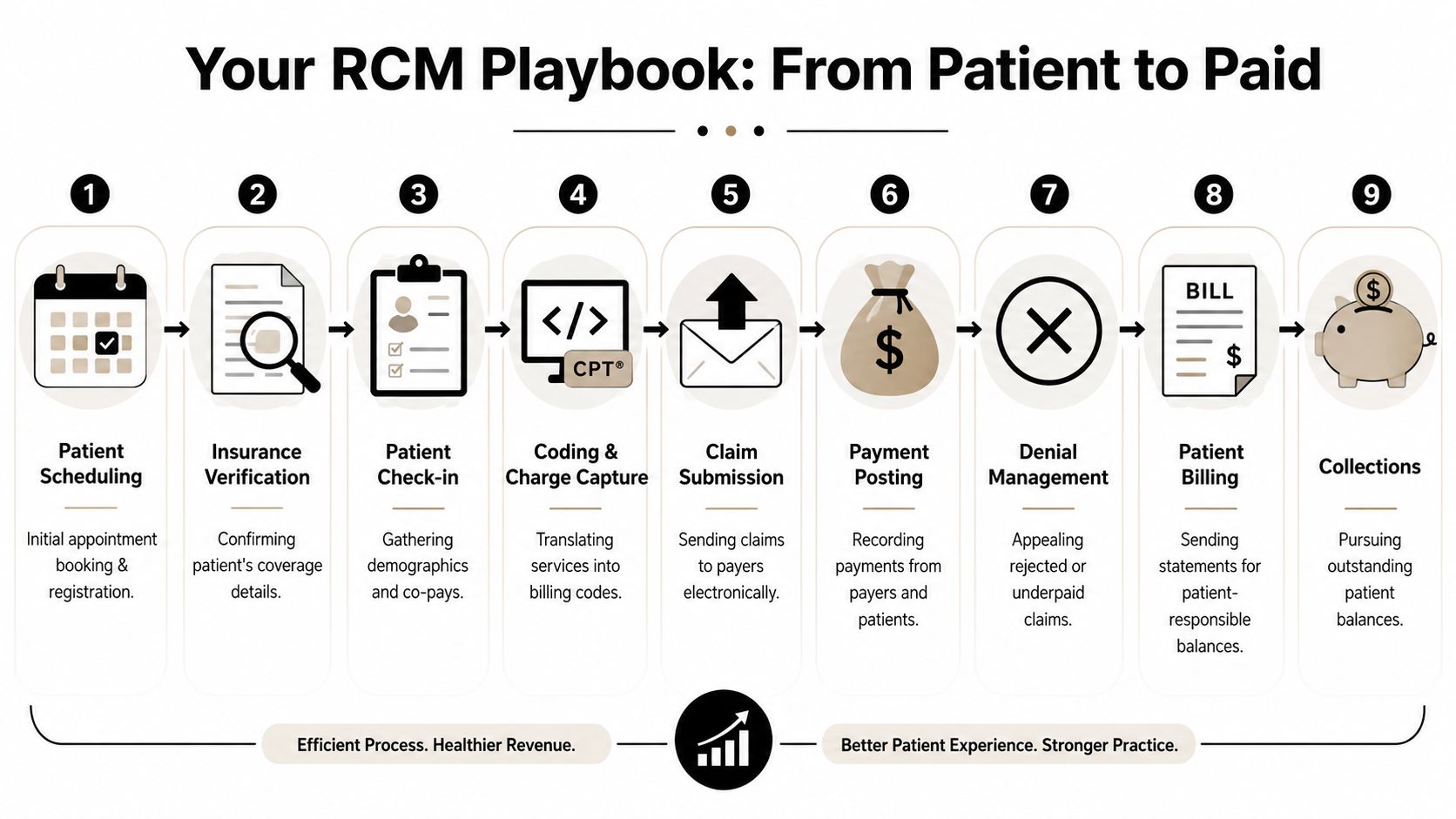

From Patient Visit to Paid Claim Your RCM Playbook

Revenue cycle management is a relay race. If one runner fumbles the handoff, the whole team loses time. In your practice, every handoff from scheduling to collections affects whether you get paid cleanly, quickly, or painfully.

The most important lesson is simple. Cash problems often start upstream.

The handoffs that matter most

Here's the no-nonsense version of your RCM playbook:

Scheduling

Get complete demographics on day one. Bad intake data poisons everything downstream.Eligibility verification

Don't wait until after the visit to learn the coverage problem. Industry guidance recommends automating eligibility verification because upstream automation reduces preventable denials, shortens claim cycle time, and lowers cost to collect (RCM workflow guidance from athenahealth).Check-in and point-of-service collection

Train staff to collect known balances and current patient responsibility before the patient leaves. Delayed patient collection usually becomes weak patient collection.Charge capture

Make sure every billable service gets captured. If the provider performed it and documented it, the charge should exist.Coding

Sloppy coding is like mailing a check to the wrong address. You did the work, but payment won't land where it should.Claim submission

Bill immediately after the visit. Speed matters because lag compounds.Payment posting

Post payments accurately and fast so the aging report reflects reality.Denial management

Work denials by root cause, not by random pile. If the same denial keeps repeating, the process is broken.Patient billing and collections

Make statements clear and timely. Confusing statements don't improve the patient experience. They stall payment.

For a deeper operational view, this guide to healthcare revenue cycle management is worth reviewing if you want to tighten each step.

A quick visual helps if you need to walk your team through the process:

Fix the front end before you attack the back end

Owners love to focus on old A/R because it feels urgent. Fine. But the bigger payoff usually comes from preventing bad claims from being created in the first place.

Use this checklist:

- Automate verification: Stop relying on manual lookups where software can handle the routine work.

- Assign prior-auth ownership: If everyone owns it, no one owns it.

- Require same-day billing workflow: Claims that sit usually age badly.

- Review denial reasons weekly: Weekly is management. Quarterly is archaeology.

- Collect at check-in or checkout: Don't turn the front desk into a courtesy desk.

A healthy revenue cycle isn't built in the billing office alone. It starts at the first patient phone call.

If your current process feels chaotic, don't buy a new dashboard first. Fix the handoffs. Bad process with better software is still bad process.

Stop Guessing Your Cash Flow and Start Forecasting It

Most practice owners confuse a budget with a forecast. That mistake causes panic.

A budget is a plan. A cash flow forecast is a prediction of what will hit and leave the bank. You need both, but if you're worried about making payroll, vendor payments, taxes, and debt obligations, the forecast is the tool that matters this week.

Build a simple rolling forecast

Don't overcomplicate this. Start with a rolling ninety-day view and update it every week.

Use three buckets:

- Expected cash in: Payer receipts, patient payments, any other operating inflows

- Committed cash out: Payroll, rent, software, loan payments, payroll taxes, insurance, key vendors

- Timing differences: Claims submitted now but paid later, disputed balances, delayed reimbursements

That's the heartbeat of practical medical practice financial management. You're not trying to predict the future perfectly. You're trying to avoid getting blindsided.

Healthcare financial guidance widely recommends keeping 3 to 6 months of fixed costs in cash reserves to absorb reimbursement delays, seasonal volume swings, and broader shocks (cash reserve guidance for medical practices). If you don't know how far your current cash carries fixed costs, you're operating without a cushion map.

What your forecast should tell you

A useful forecast answers questions like these:

| Question | Why it matters |

|---|---|

| Will cash cover payroll comfortably? | Payroll stress is usually the first visible symptom of weak forecasting |

| Are tax payments already accounted for? | Surprise tax bills are self-inflicted wounds |

| Are vendor payments timed realistically? | Late fees and strained supplier relationships damage operations |

| Is a major purchase safe right now? | Equipment bought at the wrong time can tighten working capital fast |

If you're evaluating short-term financing pressure, it helps to estimate merchant cash advance impact before accepting expensive capital that could choke future cash flow.

For owners who want a cleaner process, this walkthrough on how to forecast cash flow gives a practical framework.

Forecasting beats reacting

Here's how disciplined owners use a forecast:

- They spot the dip early: Then delay a discretionary purchase instead of scrambling later.

- They model payer lag: Not every claim pays on your preferred timeline.

- They prepare for tax obligations: Estimated payments and payroll tax deadlines shouldn't arrive as a surprise.

- They make hiring decisions with timing in mind: A good hire at the wrong cash moment can still create stress.

Owner's test: If your answer to “What will cash look like in sixty days?” is “It depends,” you need a real forecast, not a gut feeling.

A budget tells you what you hoped would happen. A forecast tells you whether the bank account agrees.

The Financial Dashboard Every Practice Owner Needs

It is Monday morning. Payroll clears in two days, a payer is running slow, and your billing manager says collections look "about normal." That answer is useless. You need a dashboard that shows where cash is getting stuck, who owns the fix, and how fast the problem is spreading.

A good dashboard is not a pile of reports. It is a control panel for survival and growth when reimbursements keep getting squeezed and administrative waste keeps rising. If your dashboard does not lead to weekly decisions, it is decoration.

The core indicators that deserve your attention

Keep the list short. Review it every week. Assign an owner to every number.

Days in A/R

This shows how long revenue sits in limbo after you earn it. If Days in A/R rises, cash is trapped. The usual culprits are slow claim submission, denials, weak follow-up, bad registration data, or coding breakdowns.

Net collection rate

This tells you how much of your allowed revenue you collect. A weak number means money is leaking after the visit. Write-offs, undertrained staff, and poor follow-up usually sit behind it.

Claim denial rate

Denials are not random weather. They are process failures with names attached to them. Eligibility checks, authorizations, coding, documentation, and payer edits all belong under active management.

First-pass resolution rate

Clean claims protect margin. Every claim that has to be touched again costs staff time, delays cash, and clogs the billing queue.

Point-of-service collections

Front-desk collection discipline matters more than owners want to admit. Dollars you fail to collect at the visit become harder and more expensive to collect later.

Current ratio and operating cash flow

You also need two balance-sheet and cash indicators on the dashboard. Current ratio shows whether short-term obligations are starting to crowd your flexibility. Operating cash flow shows whether the business is producing cash or just producing accounting profit. As noted earlier, weak liquidity deserves attention early, not after the bank balance gets tight.

Here is the practical read on the numbers:

| Metric | What it tells you | What a weak result usually signals |

|---|---|---|

| Current ratio | Ability to cover near-term obligations | Thin working capital or too much pressure from short-term liabilities |

| Days in A/R | Speed of collections | Billing lag, denials, weak follow-up |

| Operating cash flow | Real operating cash generation | Profit on paper with poor cash conversion |

| Denial rate | Claim quality and process control | Front-end or coding breakdowns |

Don't admire the dashboard. Use it.

Review this dashboard in a standing weekly meeting with the right people in the room. That means the owner, office manager, biller or RCM lead, bookkeeper, and CPA or fractional CFO if the practice has one. Financial management in a medical practice fails when nobody owns the number between report day and payroll day.

Act on changes fast.

- If Days in A/R worsens, audit claim lag by payer and provider, then fix the handoff between front desk, coding, and billing.

- If denial rate rises, stop blaming the payer and identify the exact denial categories, staff touchpoints, and physicians involved.

- If point-of-service collections slip, tighten scripts, train staff, and enforce payment policies at check-in and check-out.

- If operating cash flow weakens, compare cash receipts to payroll, rent, supplies, and debt service. Do not hide behind accrual profit.

- If current ratio tightens, delay discretionary spending and protect working capital before you talk about expansion.

Your dashboard should answer one question without delay. Where is money getting stuck right now, and who is fixing it this week? If you cannot answer that, you do not have financial control. You have a reporting habit.

Stay Compliant and Minimize Your Tax Burden

Most practice owners think “compliance” means HIPAA and maybe payroll taxes. That's far too narrow.

Your real compliance burden includes payer rules, prior authorization requirements, documentation standards, audit response, payroll reporting, contractor classification, sales and use tax issues where applicable, entity maintenance, year-end reporting, and federal and state tax filings. In healthcare, mistakes don't stay small for long.

Administrative friction is already hitting your bottom line

Physicians face a steady stream of prior authorization requirements, payer audits, and revenue-cycle burdens. The American Medical Association identifies this administrative friction as a primary driver of financial stress and recommends automation plus designated ownership for audit response to reduce leakage (AMA guidance on practice financial challenges).

That recommendation matters because many small practices still operate with vague responsibility. One person “kind of” handles payer notices. Another “usually” responds to audit requests. That's not a control system. That's a liability.

Compliance isn't paperwork for paperwork's sake. It's the difference between a manageable issue and a revenue leak that keeps repeating.

Tax law changes demand attention, not guesswork

Tax rules shift. Filing thresholds change. deduction treatment changes. Entity strategy that worked a few years ago may no longer be the best fit as your payroll, profit distribution, owner compensation, and equipment purchases evolve.

I'm not going to invent a list of 2026 tax changes that isn't verified here. The point is more practical than that. If you own a practice and you're waiting until year-end to ask tax questions, you're late. Tax planning belongs inside the year, not after it.

Here's what owners should be doing now:

- Review entity structure: Your current setup may not be the most efficient as the practice grows or ownership changes.

- Coordinate bookkeeping with tax strategy: Bad books create bad tax decisions.

- Track documentation for deductions: If you can't support it, don't count on it.

- Separate compliance ownership: Assign responsibility for payroll filings, 1099 review, W-2 processes, and payer-related documentation.

- Prepare for notices before they arrive: Clean records make audit response faster and cheaper.

DIY is often the most expensive option

Healthcare reimbursement complexity already eats management time. Add tax compliance on top, and the do-it-yourself approach becomes a gamble. You don't save money by missing filings, overlooking planning opportunities, or responding slowly to an audit letter because nobody knows where the supporting records live.

Owners should think about compliance the way they think about sterility in a procedure room. You don't improvise critical controls. You build them, document them, and review them routinely.

That's how you protect margin.

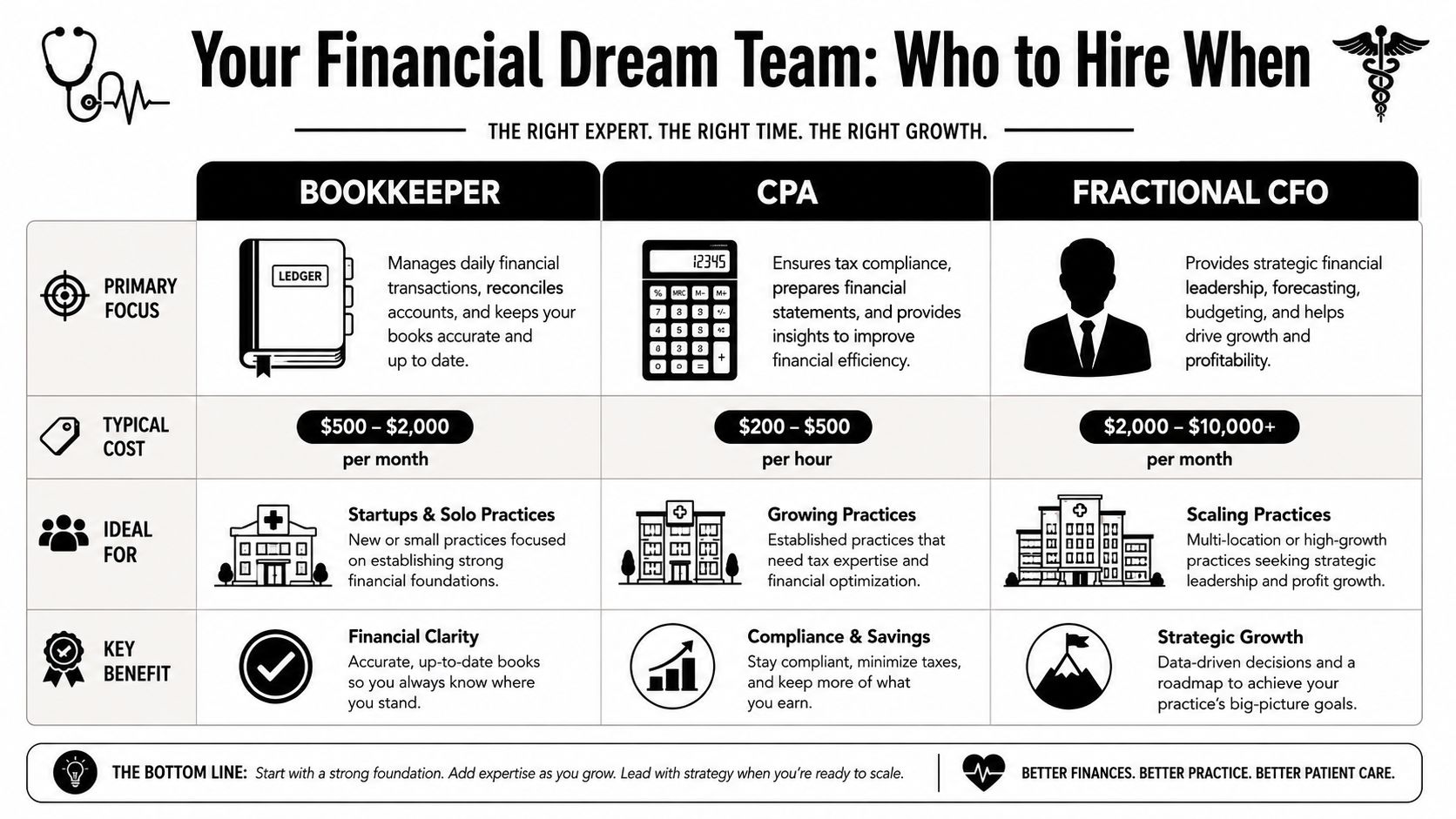

When to Hire a Bookkeeper CPA or Fractional CFO

Think of your financial team like your clinical team. You wouldn't ask one person to room the patient, diagnose the condition, perform the procedure, manage follow-up, and negotiate the payer contract. Yet many practices expect one overworked office manager to handle books, taxes, compliance, reporting, and strategy.

That setup breaks.

Physician finance literature stresses that many doctors enter practice with limited financial training and need a more structured framework for decisions such as outsourcing accounting or using a fractional CFO, especially as administrative complexity and reimbursement pressure rise (business basics guidance for physicians).

What each role actually does

Here's the clean distinction:

| Role | Best description | What they should own |

|---|---|---|

| Bookkeeper | The scorekeeper | Transaction entry, reconciliations, clean monthly books |

| CPA | The compliance and tax specialist | Tax planning, returns, financial statement accuracy, regulatory guidance |

| Fractional CFO | The strategist | Forecasting, scenario planning, cash management, decision support |

The medical-team analogy works well

Bookkeeper as your nurse taking vitals

A bookkeeper keeps the data clean and current. That means reconciled bank accounts, organized categories, timely close, and usable reports. If this role is weak, everything built on top of it gets distorted.

CPA as your specialist

Your CPA handles tax planning, filing accuracy, financial statement interpretation, and compliance insight. This role should catch risks that a general administrative team won't see.

Fractional CFO as the lead physician for the business

The fractional CFO looks ahead. This role helps answer questions like: Can we hire? Can we afford new equipment? Should we add a location? Are collections supporting growth? Is debt service putting pressure on future cash?

If you need a sharper sense of what that role includes, this overview of fractional CFO services lays it out clearly.

The right financial team doesn't just record what happened. It helps you decide what to do next.

My direct recommendation

Most small and mid-sized practices need all three functions. They may not need three full-time hires, but they need all three jobs covered.

Use this rule of thumb:

- If your books are late or messy, start with bookkeeping.

- If tax planning happens only at filing time, strengthen CPA involvement.

- If you're making hiring, expansion, debt, compensation, or purchase decisions without a forecast, you need CFO-level guidance.

Every practice needs a CFO mindset. Many practices also need a fractional CFO in reality, because strategy is too important to leave to guesswork and too specialized to dump on the front office.

Take Control of Your Practice's Financial Future

A healthy practice doesn't happen because patient volume is strong or because last quarter looked fine. It happens because the owner builds financial discipline into the operation. That means tighter revenue cycle controls, a real cash forecast, a dashboard that drives action, and a compliance process that doesn't rely on memory.

That's what modern medical practice financial management looks like. It's active. It's structured. And it protects your independence.

The practices that stay strong do three things well

They don't romanticize growth. They measure it.

They don't confuse profit with cash.

And they don't assume someone in the office is “handling finance” just because reports exist.

If you want a broader personal and business perspective alongside practice strategy, this resource on financial planning for medical professionals is a useful complement.

The real goal

You should be able to focus on medicine without wondering whether the business side is eroding underneath you. That won't happen through optimism. It happens when the numbers are clean, the controls are clear, and someone is responsible for turning data into decisions.

Own the business with the same discipline you bring to patient care. Review the numbers monthly. Forecast cash weekly. Tighten the billing workflow. Treat compliance like risk management, because that's what it is. And stop waiting for year-end to discover what the practice should've been doing all along.

Bookkeeping and Accounting of Florida Inc. helps medical practices turn messy books, cash flow uncertainty, and compliance stress into clear financial control. If you need accurate reporting, healthcare-specific accounting, tax guidance, or fractional CFO support, work with a team that knows how to keep your practice compliant, informed, and ready for smarter decisions. Schedule a consultation with Bookkeeping and Accounting of Florida Inc..