If you’re a business owner, you’ve probably stared at a profit and loss (P&L) statement that showed a healthy profit, then looked at your bank account and wondered where all the money went. It’s a classic, terrifying moment.

That’s because profit isn’t cash. And that single, simple fact is why the statement of cash flows is the most important financial report for your survival.

Your Business’s Financial Heartbeat Explained

Your income statement can lie to you. It shows sales on paper, even when your customers are taking their sweet time to pay invoices. This little bit of accounting magic can make you look profitable right before you go bankrupt from a lack of cash.

The statement of cash flows cuts through the noise. It doesn't care about "accrued revenue" or other accounting terms—it just tells a story about the hard cash moving in and out of your bank account. To really get a grip on this, you need to start by mastering the cash conversion cycle, which shows you how fast your business turns its operations into actual money.

Why This Statement Is So Critical

Most small business owners are experts at what they do, not at navigating the ever-changing maze of financial compliance. That’s where this statement becomes your best friend. It helps you:

- Make smart decisions. Know exactly how much cash you have to make payroll, buy inventory, or invest in that new equipment. No more guessing.

- Dodge a cash crisis. Spot negative trends before they turn into a full-blown disaster. Remember, profitable businesses fail from a lack of cash all the time.

- Stay compliant. Reporting your financial position accurately is non-negotiable for taxes. With constant tax law changes, this report is essential for getting it right and avoiding costly penalties. Most small businesses do not know what all is required to stay compliant, which is a major risk.

Most business owners are experts in their trade, not in complex financial reporting or shifting tax codes. They need a guide to translate the numbers into an actionable plan and ensure every 'i' is dotted and 't' is crossed for compliance.

This is exactly why you need a fractional CFO. At Bookkeeping and Accounting of Florida Inc., we don't just hand you reports. We act as your guide, helping you stay compliant and use your financial data to build a business that actually lasts. We navigate the complexities so you can have the financial clarity to thrive.

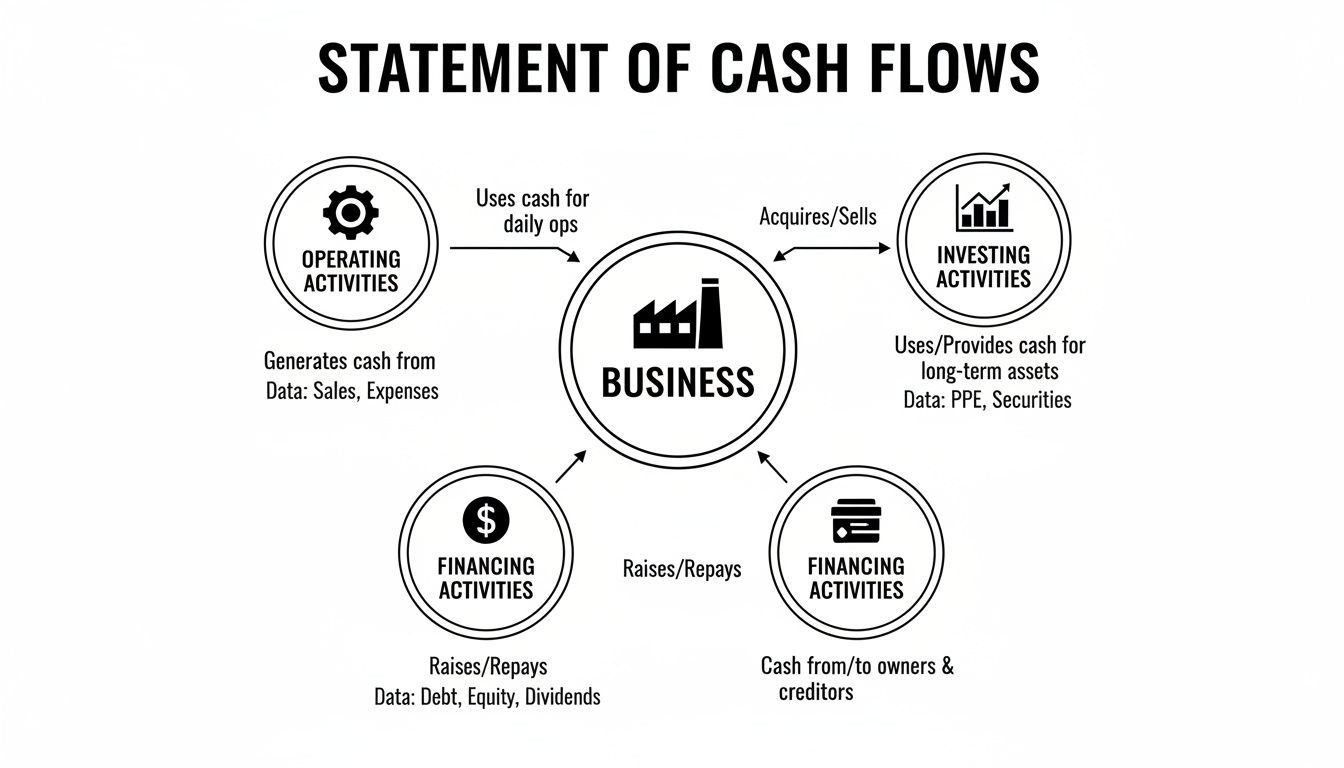

The Three Core Stories Your Cash Flow Tells

Think of your statement of cash flows as a three-act play about your business's money. It's not just some accounting document the Financial Accounting Standards Board (FASB) makes you create; it’s the real story of how you make money, spend money, and find money.

Getting a handle on these three acts is the first step to truly understanding your company’s financial pulse.

This visual gives you a quick map of how the money moves through your business—from earning it to growing with it.

You can see how the engine (Operating) is separate from reinvestment (Investing) and outside capital (Financing). Let's break down what each one really means.

Cash From Operating Activities: Your Business Engine

This is the big one. It’s the cash your business generates just by doing what it does every day. Forget "net income" for a second—this is the actual cash that hits your bank account from your core operations.

For a doctor's office, this is cash from patient payments, not just the invoices you sent out. A healthy, positive operating cash flow means your business can stand on its own two feet.

You can float a business on loans and investor money for a while. But if it can't eventually generate cash from its own operations, it's living on borrowed time. This number is the truth-teller.

This is where our business accounting and fractional CFO services earn their keep. We make sure you’re looking at real cash, not just paper profits, so you can make decisions based on reality.

Cash From Investing Activities: Your Growth Story

This section is all about where you’re placing your bets for the future. It tracks cash spent on or received from long-term assets—think buying property, new equipment, or even investing in other companies.

If your construction firm buys a new excavator, that’s a cash outflow for investing. Yes, it drains cash now, but it's a bet on future jobs. On the flip side, selling that old, dusty piece of machinery creates a cash inflow.

Don’t panic if you see a negative number here. For a growing company, that’s usually a great sign. It means you’re reinvesting your profits back into the business to get bigger and better. We help businesses make these big capital decisions, ensuring they don’t spend themselves into a corner. You can find more strategies on how to improve cash flow in a business in our complete guide.

Cash From Financing Activities: Your Funding Strategy

So, where does the money come from when it’s not from your customers? That’s what financing activities tell you. This section shows how you raise and repay outside capital.

This includes cash from:

- Taking out a new bank loan

- Investors buying equity in your company

- Paying back loans

- Paying dividends to shareholders

For a startup, a big cash inflow here probably means you just closed a funding round. For a nonprofit, it could be the arrival of a major grant. But you have to read between the lines. A large inflow could mean a healthy investment, or it could mean you're piling on debt just to keep the lights on.

To help you quickly identify where your cash is coming from and going to, we've put together a simple breakdown of these three activities.

Cash Flow Activities at a Glance

| Activity Type | What It Tells You | Example Inflows | Example Outflows |

|---|---|---|---|

| Operating | Is the core business profitable and self-sustaining? | Cash from sales of goods or services, customer payments | Payments to suppliers, employee salaries, rent, taxes |

| Investing | How is the business investing in its future growth? | Selling property, plant, or equipment; selling investments | Buying new equipment, purchasing real estate, acquiring another business |

| Financing | How is the business funding itself with outside capital? | Taking on a new loan, issuing stock to investors | Repaying loan principal, paying dividends to owners, buying back stock |

This table makes it easier to categorize transactions and see the story your numbers are telling at a glance.

Putting it all together is where the magic happens. Look at a giant like Apple. In one year, its $53.66 billion in operating cash easily funded its -$33.77 billion in investing activities (like R&D and new facilities) and -$16.379 billion in financing (like paying back investors).

That’s a healthy cycle. Your operating cash flow is the engine that should fund your growth. In most small and medium-sized businesses, it accounts for 60-70% of all expansion.

Most business owners don't have time to become experts in financial reporting. They just want to know what the numbers mean. That’s what our business accounting services do. We turn the complex into the clear, so you can focus on running your business.

Direct vs. Indirect: The Two Roads to Cash Flow Truth

When accountants put together your statement of cash flows, they have two ways to do it: the Direct Method and the Indirect Method. They both end up at the same number for cash from operations, but the journey they take to get there is completely different.

Let's get one thing straight: you’ll almost never see the Direct Method. Think of it like a detailed diary of every dollar that came in from customers and every dollar that went out to suppliers or for payroll. It’s simple to read but a total nightmare to create.

That's why over 98% of companies use the Indirect Method. This is the one you need to understand.

The Indirect Method: What Your Accountant Is Actually Doing

Instead of tracking every single transaction, the Indirect Method is a bit of a detective story. It starts with your net income (the "profit" from your P&L statement) and then works backward to find out where the actual cash went.

Your net income is a great starting point, but it's not cash. It’s an accounting figure that includes all sorts of things that never touched your bank account.

The Indirect Method adjusts for two main things:

- Non-cash expenses: The most common one is depreciation. You didn't actually write a check for "depreciation," so this amount gets added back to your net income.

- Changes in working capital: This is where the real story is. It looks at the shifts in what you owe (accounts payable) and what people owe you (accounts receivable). If your receivables went up, it means you made sales but haven't been paid yet. That's not cash in the bank, so it gets subtracted.

Why You Should Care About These Adjustments

You don't need to become an expert at preparing these statements. But you absolutely need to understand what they're telling you. These adjustments turn a boring accounting report into a powerful diagnostic tool.

The Financial Accounting Standards Board (FASB) made this statement mandatory back in 1988, and for good reason. Before that, it was tough to get a clear picture of a company’s actual cash position. You can see how the cash flow statement has evolved and why it's so critical for modern business analysis.

The Indirect Method answers the classic question: "If my P&L says we made a $50,000 profit, why did my bank balance only go up by $10,000?"

This is exactly where our business accounting services come in. Most business owners are too busy to track the constantly shifting compliance and tax law changes that affect these reports. A fractional CFO from our team handles the complex reconciliations in QuickBooks, making sure your books are accurate and compliant so you can focus on what the numbers are telling you.

How to Spot Critical Cash Flow Red Flags

Reading your statement of cash flows is like being a financial detective. Forget the surface-level profits for a moment; this document holds the real clues to your company’s health, digging into the hard truth of your bank account.

Getting this wrong is a huge deal. A staggering 82% of small business failures trace back to poor cash management. It’s the silent killer of otherwise healthy-looking businesses.

Let’s walk through a classic scenario. Your income statement is glowing with a healthy net income, but your cash from operations is deep in the red. This is a five-alarm fire. It screams that you have a problem with accounts receivable—you’re making sales, but your customers aren’t paying you.

This is the blind spot that trips up so many entrepreneurs. They see profit on paper and assume everything’s fine, only to get ambushed by a cash crisis when payroll is due.

To help you become a better financial detective, I've put together a quick-reference table of the most common red flags. Think of it as a field guide to spotting trouble before it takes you down.

Common Cash Flow Red Flags and What They Mean

| Red Flag (Symptom) | What It Could Mean | Action to Consider |

|---|---|---|

| Negative Operating Cash Flow (but Profitable) | Your customers aren't paying you fast enough (high accounts receivable), or you have too much cash tied up in unsold inventory. | Tighten credit terms, aggressively pursue collections, and optimize your inventory management. |

| Consistently Positive Financing Cash Flow | You're constantly borrowing money or selling equity just to cover day-to-day operating expenses. You're living on borrowed time. | Address the root cause of your poor operating cash flow. This is not a long-term solution. |

| Negative Investing Cash Flow (Sustained & High) | You're spending heavily on new assets like equipment or property. This can be good (growth) or bad (overspending). | Cross-reference with your strategic plan. Is this investment generating a return, or is it just draining cash? |

| Profits and Operating Cash Flow Are Drifting Apart | Your "paper profits" are growing, but the actual cash hitting your bank account isn't keeping pace. A classic sign of trouble ahead. | Review revenue recognition policies and check if your receivables or inventory are ballooning. |

| Selling Off Assets to Generate Cash | You're seeing positive cash from investing by selling off equipment or property. It might be a one-time cash boost, but it could mean you're liquidating to survive. | Determine if this is a strategic move to get rid of old assets or a desperate measure to pay the bills. |

Keep this table handy when you review your financials. Recognizing the symptom is the first step; taking the right action is what keeps your business healthy and growing.

Over-Reliance on Financing

Now, take a hard look at your financing activities. Is that section consistently positive, quarter after quarter? While taking out a loan for a strategic growth project is smart, needing a constant drip of new debt or investor cash just to keep the lights on is a massive red flag.

A business that consistently borrows money to pay its bills isn't growing; it's surviving. This dependency on external capital is unsustainable and masks underlying operational issues.

This is a trap. Too many businesses use financing as a bandage for weak operating cash flow instead of fixing the actual wound. A good fractional CFO is trained to spot this dangerous cycle and steer you back toward a business that funds itself. This is what truly understanding statement of cash flows at a strategic level is all about.

Inaccurate Books and Red Flags You Can't See

Spotting these signals is only possible if your bookkeeping is accurate. With ever-changing tax law changes, even small errors in applying new rules for deductions or expenses can have a big impact. A simple mistake in how you categorize a transaction can warp your financial picture, leading you to make terrible decisions based on flawed data.

Most business owners don’t have the time to become experts in compliance. But an error here and there adds up, creating red flags you can’t even see.

That’s why having an expert in your corner isn't a luxury—it's a necessity. At Bookkeeping and Accounting of Florida Inc., our business accounting team helps clients in construction, healthcare, and retail navigate this complexity. We turn raw financial data into a clear, forward-looking action plan so you're not just compliant, but strategically sound.

Ready to get ahead of the curve? Check out our guide on how to forecast cash flow.

Why a Fractional CFO Is Your Key to Growth

So you’ve learned how to read your financial statements. That’s step one. But turning those numbers into a real growth strategy is a whole different ballgame. It’s what separates the businesses that thrive from the ones that just tread water.

Let’s be honest. You’re an expert at what you do—not necessarily at the tangled web of accounting, tax law changes, and financial forecasting. That’s exactly where a fractional CFO from Bookkeeping and Accounting of Florida Inc. steps in.

Here's the secret: all companies need a fractional CFO and someone to guide their business, but most small businesses can’t swallow the six-figure salary of a full-time executive. Our business accounting services give you that same senior-level financial brainpower—forecasting, budget analysis, strategic advice—without the full-time cost. Our job is to be the expert in your corner, decoding the numbers so you can focus on running your business.

Navigating Complexity and Ensuring Compliance

For a lot of small businesses, the financial world feels like a minefield of deadlines and rules they don't even know exist. This is especially true with the never-ending stream of tax law changes that can blow up everything from your expense reports to your final tax bill.

Frankly, most owners need us to help them stay compliant because they don't know what all is required. We manage these headaches, making sure you never miss a deadline or make a mistake that costs you big time. It's about giving you the peace of mind that your financials are clean and your business is on solid legal ground.

This is even more critical in specialized Florida industries:

- Healthcare: We make sure your practice manages its revenue cycle without leaks and stays compliant with all the industry-specific reporting rules. Using smart strategies like outsourced revenue cycle management can also slash denial rates and speed up collections, fixing major cash flow problems before they start.

- Non-profits: We help you navigate the tricky world of restricted grants, prepare for audits, and maintain the squeaky-clean financial records needed to keep your tax-exempt status.

- Construction: Our deep experience in job costing and project-based accounting means you get a crystal-clear picture of your profit on every single job.

A fractional CFO doesn't just stare at last month's numbers; they use them to draw a map for your future. They translate the story your cash flow statement is telling into a concrete plan for growth.

From Data to Decisions: The Fractional CFO Difference

The real magic of a fractional CFO is turning raw data into smart decisions. Sure, understanding statement of cash flows is a great skill to have, but you need an expert to connect those numbers to what you should do next Monday morning.

We don't just email you reports and disappear. We sit down with you and explain what it all means for your company's future. If your operating cash flow looks weak, we don't just point it out—we help you build a plan to tighten up collections, move inventory faster, and strengthen your financial foundation.

This kind of guidance is indispensable. We become part of your leadership team, adding the financial discipline every growing business needs. By partnering with Bookkeeping and Accounting of Florida Inc., you get an expert who's as committed to your success as you are.

If you want to see how this high-level partnership can change your business, you can learn more about our fractional CFO services and how we help businesses get to the next level. We're an indispensable partner for any growing Florida business.

Your Top Cash Flow Questions, Answered

After digging into the numbers, a few key questions always pop up. These aren't just accounting details; they're business survival questions. Let's get straight to what you really want to know.

My Business Is Profitable, So Why Am I Always Broke?

This is the big one. We hear it all the time, and it’s exactly why the cash flow statement is so critical. Your profit and loss (P&L) statement runs on accrual accounting. It shows you income when you earn it, not when the cash actually lands in your bank account.

So you closed a fantastic $20,000 deal in March. Your P&L looks amazing. But if the client has 60-day terms, you won't see a dime until May. Meanwhile, you’ve got rent, payroll, and vendor bills due in April that need to be paid with actual cash.

The statement of cash flows bridges the gap between paper profits and cold, hard cash. If your profits are high but your operating cash flow is in the red, that’s a massive red flag. It usually means you’ve got a collections problem or your money is all tied up in inventory.

How Often Should I Look at This Thing?

For the average business, a thorough monthly review of your big three financial statements (P&L, balance sheet, and cash flow) is the absolute minimum. This gives you enough time to catch bad habits before they bankrupt you.

But if your business has razor-thin margins or is highly seasonal—think Florida construction firms or holiday retail shops—a weekly cash flow check-in is non-negotiable. It’s your real-time pulse on whether you can make payroll next Friday.

Can't I Just Run the Report in QuickBooks?

You can, but there’s a huge catch. QuickBooks can spit out a statement of cash flows in seconds, but that report is only as good as the bookkeeping behind it. It's the classic "garbage in, garbage out" scenario.

If your transactions are miscategorized, your chart of accounts is a mess, or you haven’t factored in recent tax law changes to depreciation, that report is dangerously wrong. You might think you have cash you don't, or miss a warning sign buried in bad data.

Relying on an automated report without a professional set of eyes is like letting a robot fly your plane. It might work, until it doesn't.

As Certified QuickBooks ProAdvisors, we don't just push a button. We build a clean, compliant set of books first with our business accounting services, so the reports you depend on are actually telling you the truth.

What's the Difference Between Cash Flow and EBITDA?

People love to throw around EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) as a stand-in for cash flow. Don't do it. It's a wildly misleading shortcut.

EBITDA’s biggest flaw is that it completely ignores changes in working capital. It doesn't see the cash that's stuck in unpaid customer invoices (accounts receivable) or the money you spent on inventory just sitting on the shelf. A company can have a stellar EBITDA and still be bleeding cash because its working capital management is a disaster.

Cash Flow from Operations is the real-deal metric for your company's financial health. It accounts for those messy, real-world cash movements. A fractional CFO will look at both, but they'll always trust the cash flow statement to tell the true story.

Don't let financial uncertainty hold your business back. Most small businesses lack the expertise to navigate complex compliance and financial strategy, but that’s where we come in. At Bookkeeping and Accounting of Florida Inc., we provide the expert guidance and meticulous business accounting every company needs to stay compliant and build a financially resilient future. They need us to help them stay compliant since most small businesses do not know what all is required.

Schedule your consultation today and gain the peace of mind that comes from knowing your numbers are right.